Houlihan Lokey (HLI): Reassessing Valuation as Sponsor-Led Deal Recovery Expectations Build

Morgan Stanley is leaning into a 2026 rebound in sponsor led deals, and Houlihan Lokey (HLI) sits squarely in that slipstream as investors reassess the earnings power of fee driven advisory franchises.

See our latest analysis for Houlihan Lokey.

At around $179.87, Houlihan Lokey’s share price has cooled off from its recent highs. A weak 3 month share price return contrasts sharply with a powerful 3 year total shareholder return that signals longer term momentum is still very much intact.

If this advisory rebound has your attention, it could be a good moment to see what else is gaining traction and explore fast growing stocks with high insider ownership.

With advisory volumes still subdued and Houlihan Lokey trading below analyst targets despite robust multi year returns, investors now face a key question: is this a genuine entry point, or is the market already baking in the 2026 rebound?

Most Popular Narrative: 14.7% Undervalued

Against a last close of $179.87, the most widely followed narrative points to a fair value near $210.86, framing upside through earnings power and multiple resilience.

Increasing global corporate complexity and cross-border transactions are driving ongoing demand for independent advisory expertise, as evidenced by resilient revenues and continued international hiring and expansion initiatives. These factors are expected to support sustained top-line revenue growth.

Curious how mid teens growth, fatter margins, and a premium earnings multiple can still add up to upside from here? Unpack the full narrative to see which long range assumptions really carry this valuation.

Result: Fair Value of $210.86 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, softer global M&A volumes or sustained compensation pressure could quickly compress margins and test the assumptions behind Houlihan Lokey’s premium multiple and growth trajectory.

Find out about the key risks to this Houlihan Lokey narrative.

Another Lens on Value

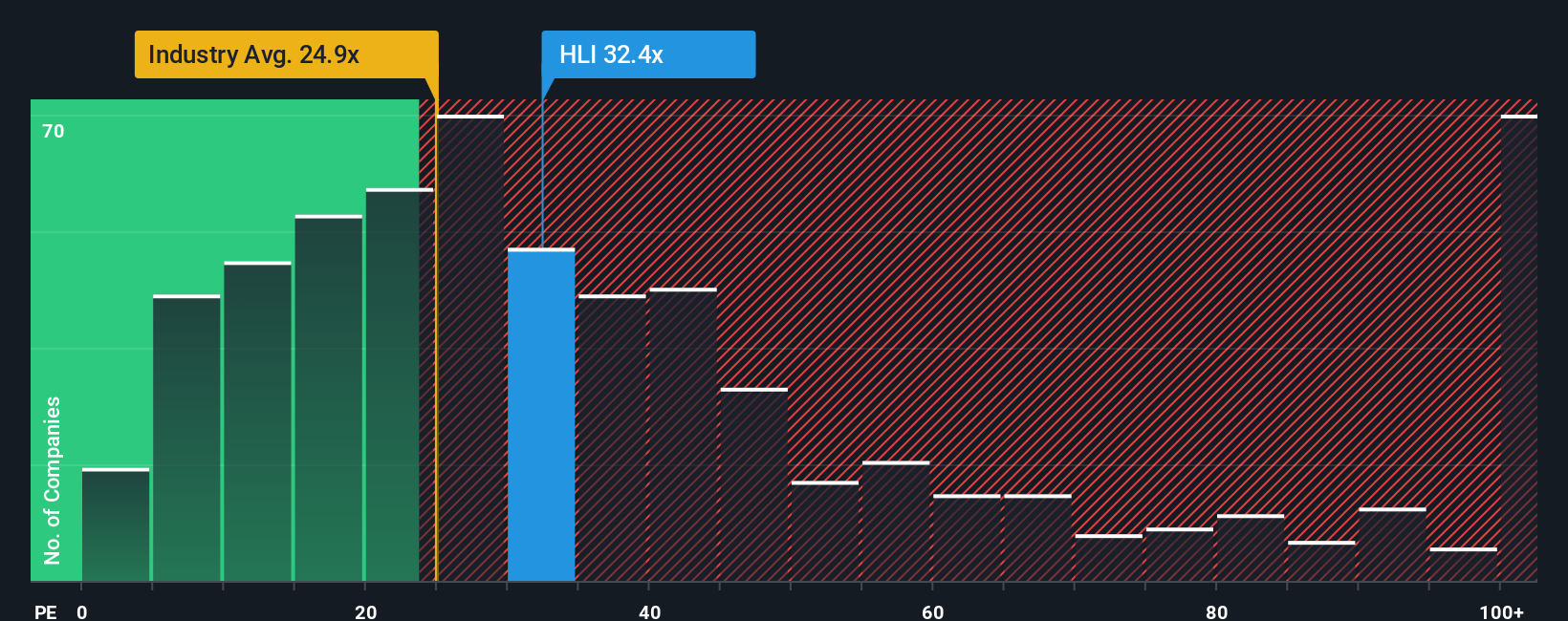

Our fair ratio work paints a tougher picture. HLI trades on a 29.5x earnings multiple versus a 15.8x fair ratio, above both the US Capital Markets industry at 25.8x and peers at 19.2x. If growth stumbles, this rich setup could unwind faster than the narrative implies.

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Houlihan Lokey Narrative

If you see the story differently or want to dive into the numbers yourself, you can build a personalized narrative in just a few minutes using Do it your way.

A good starting point is our analysis highlighting 2 key rewards investors are optimistic about regarding Houlihan Lokey.

Looking for more investment ideas?

Maintain your edge by looking beyond Houlihan Lokey. Some of the most effective moves can come from fresh ideas that others overlook in today’s shifting market.

- Explore potential mispricing by scanning these 904 undervalued stocks based on cash flows, where quality businesses may trade at meaningful discounts to their intrinsic cash flow characteristics.

- Focus on structural innovation by targeting these 25 AI penny stocks, which may be positioned to benefit as artificial intelligence influences productivity, automation, and long term earnings dynamics.

- Seek to strengthen your income stream by filtering for these 12 dividend stocks with yields > 3%, which can help support a compounding approach through regular cash payouts.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com