- PREMIUM

- LIVE QUOTES

- INSTITUTIONS

Index Options

Index Options State Street

State Street CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street JournalEvergy (EVRG): Assessing Valuation After a Recent Share Price Pullback and Strong Multi‑Year Returns

Evergy (EVRG) has quietly pulled back about 5% over the past month even though the stock is still up roughly 23% over the past year, which sets up an interesting valuation check.

See our latest analysis for Evergy.

With the share price now around $73.37, that recent 30 day share price pullback sits against a much stronger year to date gain and a solid multi year total shareholder return profile. This suggests momentum has cooled a bit, but the longer term story is still intact.

If Evergy’s steadier utilities profile has you thinking about where growth might be stronger, this could be a good moment to explore fast growing stocks with high insider ownership.

So with a solid multi year track record, healthy recent earnings growth and a share price still below Wall Street targets, is Evergy quietly offering upside here, or is the market already pricing in the next leg of growth?

Most Popular Narrative Narrative: 13% Undervalued

With Evergy last closing at $73.37 against a most popular narrative fair value near $84.32, the story leans toward upside while hinging on specific long term assumptions.

Robust economic development pipeline (15+ GW), with advanced stages of customer agreements and significant financial commitments from large users, indicates continued customer and volume growth, which will expand rate base and drive above average rate base and EPS growth over time.

Want to see how those growth commitments turn into a double digit earnings path and a premium future multiple for a regulated utility? The narrative explains how modest revenue acceleration, margin lift, and a lower forward valuation multiple can still be combined to reach that higher fair value.

Result: Fair Value of $84.32 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, that upside case still hinges on Evergy executing its capital plan smoothly and large customers ramping as expected, without regulatory pushback capping returns.

Find out about the key risks to this Evergy narrative.

Another Angle On Value

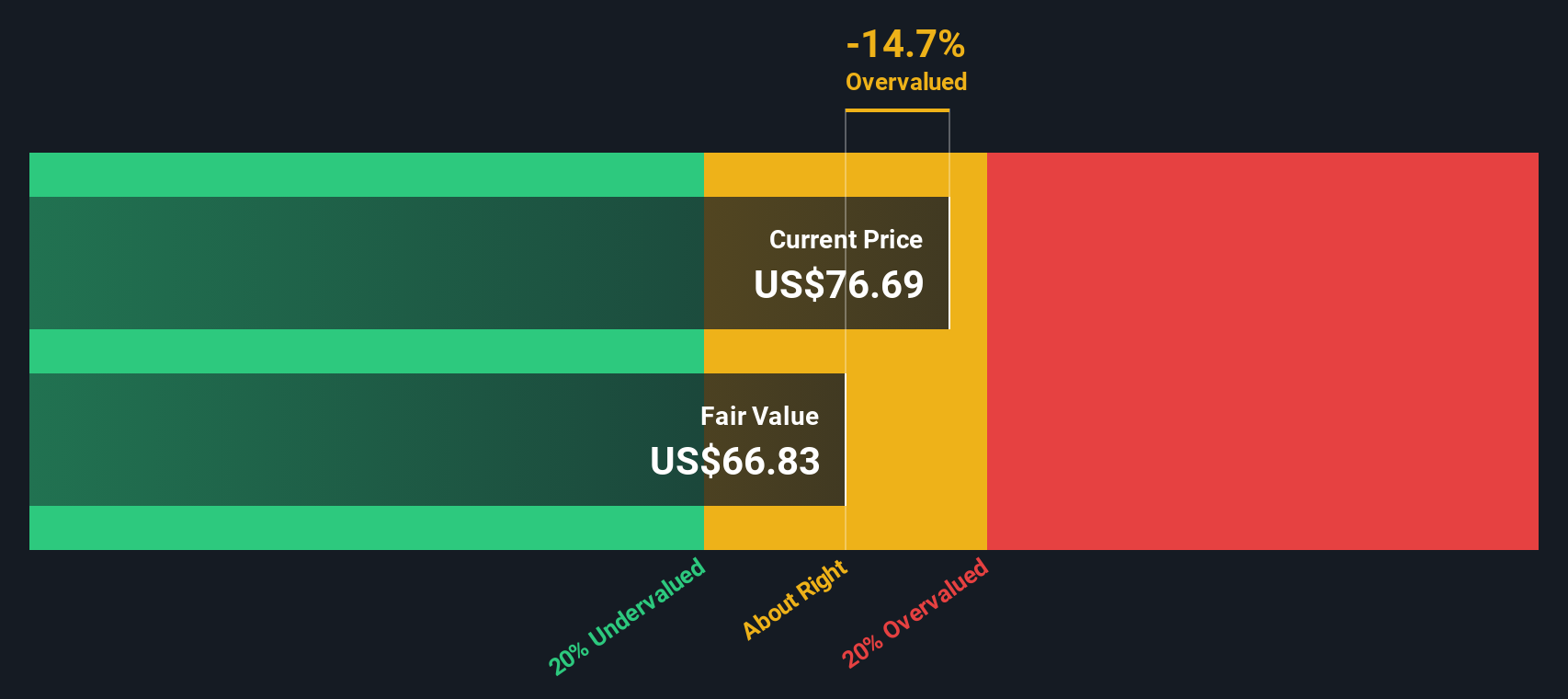

Our SWS DCF model is less generous than the upbeat narrative, pointing to a fair value near $63.89 versus today’s $73.37 price. This implies Evergy looks overvalued on cash flows and leaves less margin for regulatory or project surprises.

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Evergy for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 905 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Evergy Narrative

If you see the story differently or want to dig into the numbers yourself, you can quickly build a personalized view in just minutes: Do it your way.

A great starting point for your Evergy research is our analysis highlighting 1 key reward and 2 important warning signs that could impact your investment decision.

Ready for more investment ideas?

If Evergy sparked your interest, do not stop here. Use the Simply Wall Street Screener now to uncover fresh, data driven opportunities before everyone else.

- Capitalize on mispriced opportunities by targeting these 905 undervalued stocks based on cash flows that the market has not fully appreciated yet.

- Ride powerful income trends by focusing on these 12 dividend stocks with yields > 3% that can help strengthen your long term cash flow.

- Position yourself ahead of digital finance shifts by zeroing in on these 80 cryptocurrency and blockchain stocks shaping the future of blockchain and decentralized technologies.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com