Trane Technologies (TT): Assessing Valuation After a Strong Multi-Year Run and Recent Share Price Consolidation

Trane Technologies (TT) has been treading water lately, with the stock roughly flat over the past year after a strong multi year run, even as revenue and net income continue to grow steadily.

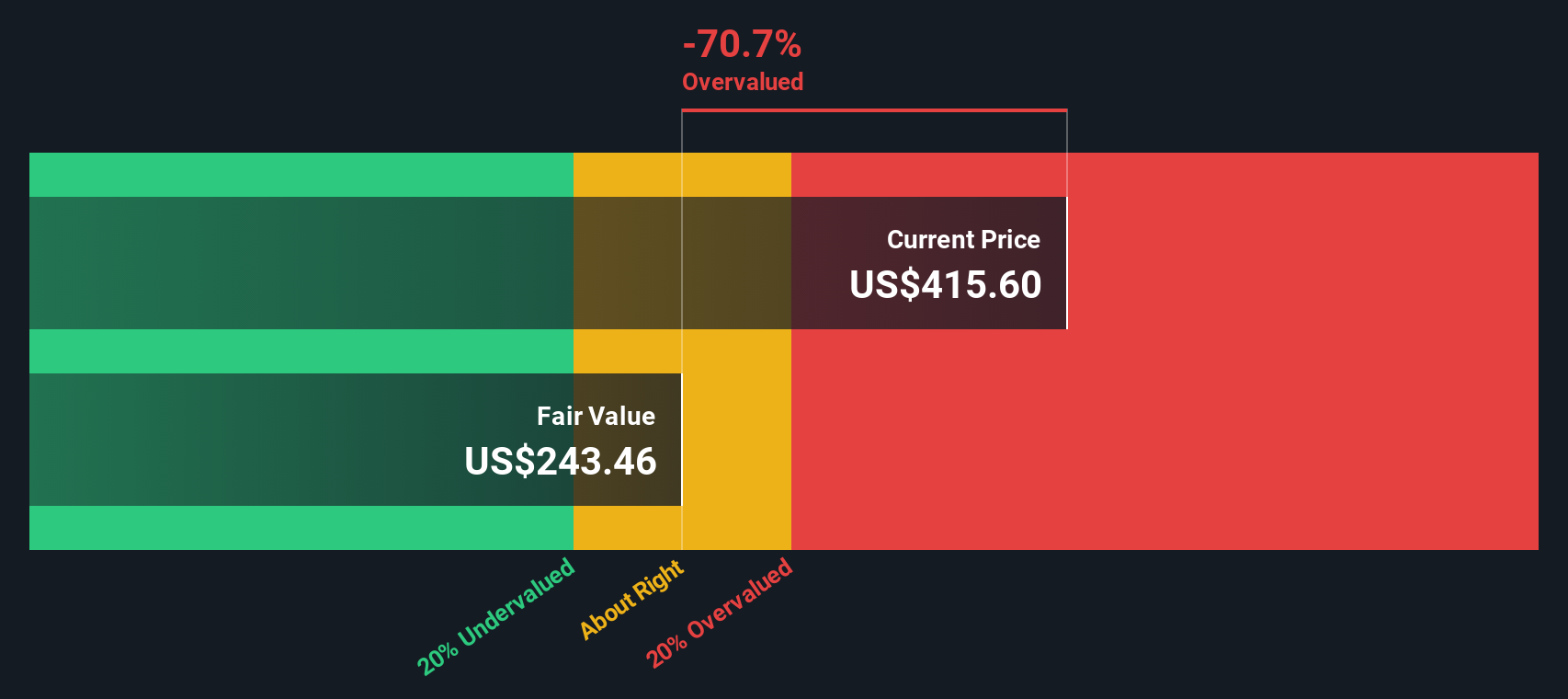

See our latest analysis for Trane Technologies.

At around a 7 percent year to date share price return and a powerful five year total shareholder return of just over 200 percent, Trane’s recent consolidation near 399.14 looks more like a pause after a long rally than a trend break. Investors are reassessing growth and pricing power after years of strong execution.

If Trane’s steady performance has you thinking about where else momentum and quality might be lining up, this is a good moment to explore fast growing stocks with high insider ownership.

With earnings still growing faster than sales and the stock trading roughly 21 percent below the average analyst target, is Trane quietly undervalued here, or has the market already priced in its next leg of growth?

Most Popular Narrative Narrative: 17.2% Undervalued

The most followed narrative sees Trane’s fair value near 482 dollars, well above the 399 dollar last close, framing an upside case driven by durable growth and margins.

The strategic emphasis on innovation and a direct sales force enables Trane Technologies to consistently outgrow its end markets. This approach supports long term revenue expansion and potential margin improvement due to enhanced market positioning and customer engagement.

Want to see why steady revenue gains, rising profitability, and a richer future earnings multiple all converge on that higher value? The narrative’s projections may surprise you.

Result: Fair Value of $482.02 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, a prolonged slump in transport markets or weaker demand from data centers and healthcare could quickly challenge those upbeat growth and margin assumptions.

Find out about the key risks to this Trane Technologies narrative.

Another Lens on Value

Analysts see upside to fair value, but our SWS DCF model is more cautious, placing Trane’s worth closer to 307.91 dollars a share, below today’s 399.14. If cash flows do not ramp as expected, is the stock already pricing in too much of tomorrow’s growth?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Trane Technologies for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 904 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Trane Technologies Narrative

If you see the story differently, or simply prefer to test the numbers yourself, you can build a complete view in minutes: Do it your way.

A great starting point for your Trane Technologies research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Ready for your next investing move?

Before you move on, lock in your edge by using the Simply Wall St Screener to pinpoint stocks that match your strategy instead of leaving opportunities on the table.

- Capitalize on turnaround potential with these 3602 penny stocks with strong financials that already back their promise with solid financial foundations.

- Ride the next wave of innovation by targeting these 26 AI penny stocks positioned at the heart of the AI transformation.

- Lock in higher income prospects through these 12 dividend stocks with yields > 3% that can strengthen your portfolio’s cash flow.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com