Evaluating Hinge Health (HNGE)’s Valuation After a Recent Rebound in Share Price Momentum

Hinge Health (HNGE) has been quietly on the move, with shares up over 12% in the past month and more than 32% year to date, even though the past 3 months have remained choppy.

See our latest analysis for Hinge Health.

That mix of a 7 day share price return near 8 percent and a 30 day share price return above 12 percent, despite a weaker 90 day patch, suggests momentum in Hinge Health is quietly rebuilding as investors reassess its growth story and risk profile around the 49.69 dollar mark.

If Hinge Health has caught your eye, this might also be a good moment to explore other innovative healthcare stocks that could be riding similar structural trends in digital care and medical services.

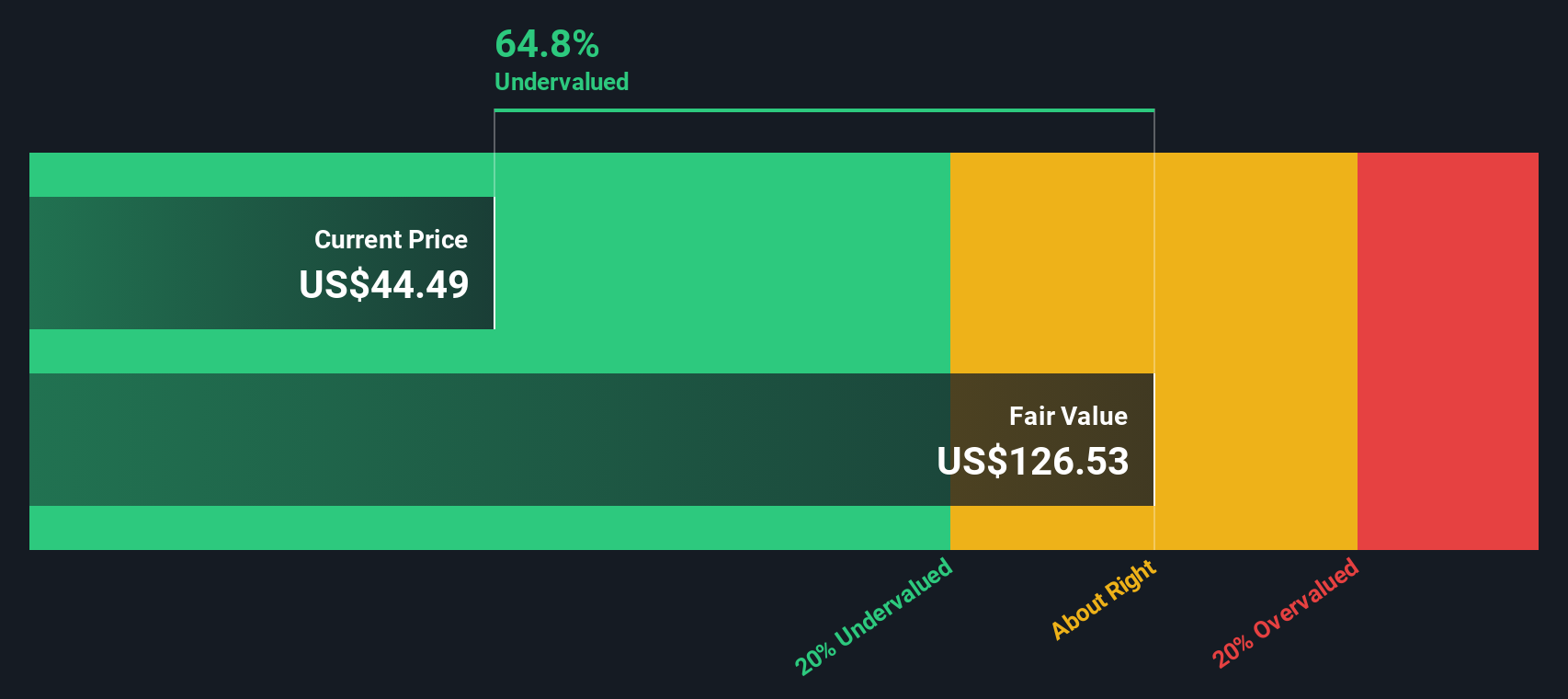

Yet with shares still trading at a steep discount to analyst targets and intrinsic value estimates, investors face a key question: Is Hinge Health quietly undervalued, or is the market already pricing in its future growth?

Price-to-Sales of 7.3x: Is it justified?

On a price-to-sales basis, Hinge Health looks relatively richly priced at its recent 49.69 dollar close, even though some metrics still flag it as good value.

The price-to-sales ratio compares the company’s market value to its revenue, a common yardstick for high growth, loss making healthcare and digital health businesses where profits are still some way off.

For Hinge Health, the headline 7.3 times sales multiple screens attractively against close peers, where the typical company trades around 9.7 times. This implies the market is not fully bidding up its revenue base despite strong historic and forecast growth.

Set against the broader US Healthcare sector however, where the average price-to-sales sits near 1.3 times, Hinge Health commands a hefty premium. Even versus an estimated fair price-to-sales level of 6.4 times, the shares look stretched, suggesting room for the multiple to drift lower if execution or growth disappoint.

Explore the SWS fair ratio for Hinge Health

Result: Price-to-Sales of 7.3x (OVERVALUED)

However, investors still face meaningful risks, including ongoing heavy losses and any slowdown in musculoskeletal program adoption among large self insured employers.

Find out about the key risks to this Hinge Health narrative.

Another View: DCF Points to Deep Value

While the 7.3 times sales multiple looks demanding, our DCF model presents a different perspective. It suggests fair value near 122.72 dollars, which is around 59.5 percent above today’s 49.69 dollar price. If that cash flow outlook proves accurate, this volatility may represent a long term entry point.

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Hinge Health for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 908 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Hinge Health Narrative

If you see the numbers differently or simply prefer to draw your own conclusions, you can build a tailored view in just a few minutes: Do it your way.

A great starting point for your Hinge Health research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

Ready for more high conviction opportunities?

Do not stop at a single compelling story. Use the Simply Wall Street Screener to uncover fresh, data backed ideas before the crowd moves on.

- Capture early stage potential by reviewing these 3602 penny stocks with strong financials that pair tiny market caps with surprisingly resilient fundamentals.

- Position yourself for the next wave of automation by focusing on these 26 AI penny stocks shaping software, infrastructure, and intelligent platforms.

- Lock in quality at sensible prices with these 908 undervalued stocks based on cash flows that our models flag as trading below their cash flow potential.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com