What Evolution Mining (ASX:EVN)'s Bigger Lithium Bet Means For Its Gold-Focused Shareholders

- In late November 2025, Surge Battery Metals Inc., through its U.S. subsidiary, finalized all documents for a joint venture with an Evolution Mining Limited subsidiary to advance the Nevada North Lithium Project, and by mid-December Evolution had funded an initial CA$3,000,000, lifting its stake in Nevada North Lithium LLC to 25.85%.

- This move expands Evolution’s exposure beyond its core gold operations into lithium exploration, linking the group more directly to electric vehicle and battery supply chains.

- We’ll now explore how Evolution’s higher-funded lithium joint venture stake could influence its gold-focused investment narrative and long-term portfolio balance.

We've found 12 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

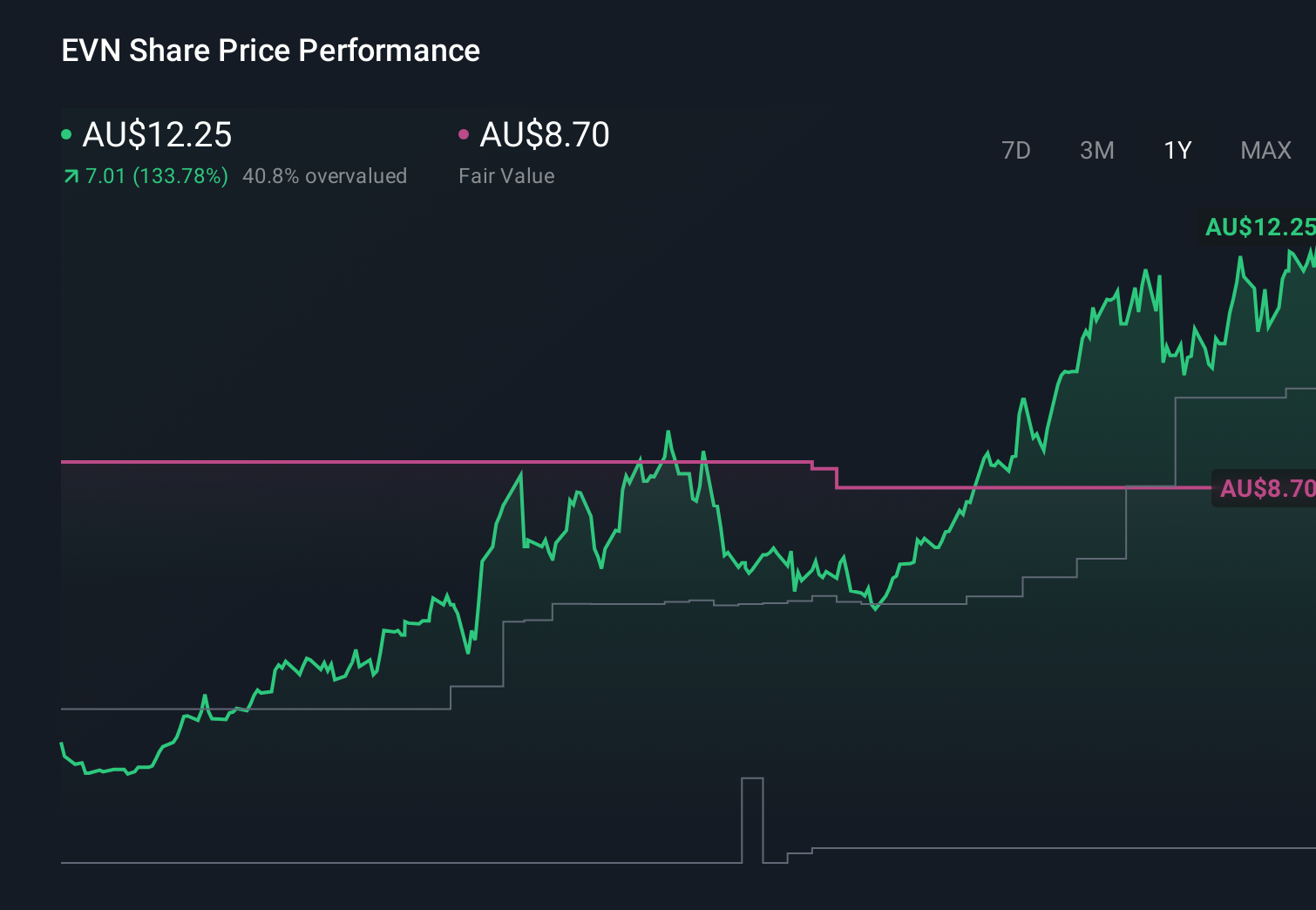

Evolution Mining Investment Narrative Recap

To own Evolution Mining, you need to be comfortable with a gold producer that is already priced at a premium on earnings and has delivered strong recent returns, while still relying heavily on gold prices and disciplined cost control. The Nevada North lithium joint venture modestly broadens its exposure to battery materials, but given Evolution’s scale and gold focus, this initial CA$3,000,000 step does not materially change the near term catalyst of operational delivery at its core assets or the key risk of rising costs and regulatory burdens.

The recent commissioning of the expanded Mungari mill, completed ahead of schedule and under its A$228,000,000 budget, is more central to Evolution’s current catalyst set than the lithium JV. It directly ties into expectations for sustained margins and production, against a backdrop where investors are already paying up on a 26.9x P/E and future earnings growth is forecast to trail the broader Australian market, making execution on core gold projects a crucial piece of the story investors should understand before they decide to...

Read the full narrative on Evolution Mining (it's free!)

Evolution Mining's narrative projects A$4.9 billion revenue and A$1.1 billion earnings by 2028. This requires 4.1% yearly revenue growth and an earnings increase of about A$200 million from A$926.2 million today.

Uncover how Evolution Mining's forecasts yield a A$10.22 fair value, a 17% downside to its current price.

Exploring Other Perspectives

Six fair value estimates from the Simply Wall St Community range from A$6.13 to A$10.23, reflecting very different views on Evolution’s upside. Against that, the company’s high margins and cost position still depend on managing rising regulatory and ESG costs, which could influence how those valuations play out over time, so you may want to compare several of these perspectives before forming your own view.

Explore 6 other fair value estimates on Evolution Mining - why the stock might be worth 50% less than the current price!

Build Your Own Evolution Mining Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Evolution Mining research is our analysis highlighting 2 key rewards that could impact your investment decision.

- Our free Evolution Mining research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Evolution Mining's overall financial health at a glance.

Curious About Other Options?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- These 10 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

- Rare earth metals are the new gold rush. Find out which 37 stocks are leading the charge.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com