Canadian Solar (NasdaqGS:CSIQ) Valuation After New U.S. Reshoring Push and Manufacturing Expansion

Canadian Solar (NasdaqGS:CSIQ) just shook up its U.S. strategy, unveiling a reshoring push that puts key manufacturing and American joint ventures directly under the parent company. The move aims to tighten control and align with domestic policy tailwinds.

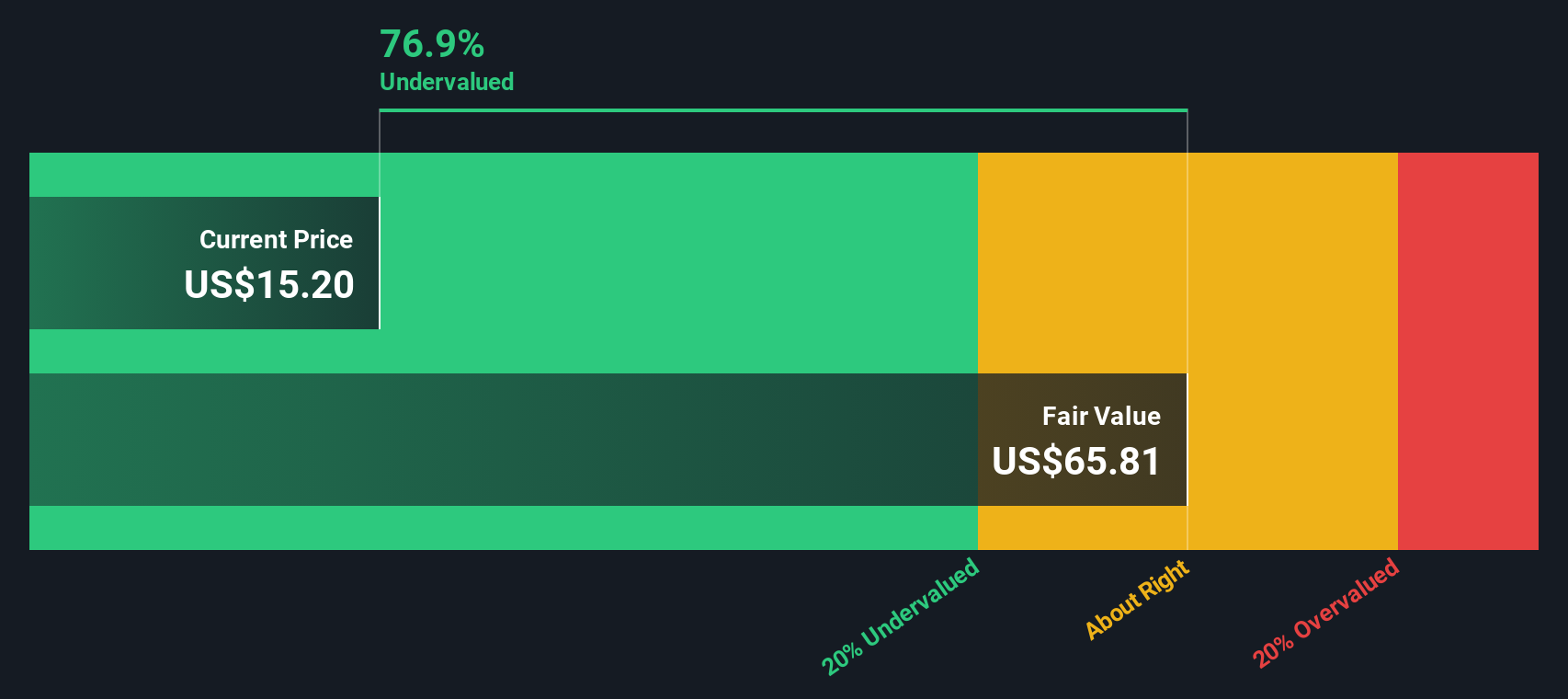

See our latest analysis for Canadian Solar.

The reshoring announcement comes after a volatile period, with a 90 day share price return of 125.88 percent and a year to date share price return of 102.24 percent signaling powerful but still fragile momentum. This contrasts with a three year total shareholder return of negative 30.82 percent and a five year total shareholder return of negative 42.16 percent.

If this kind of policy backed growth story interests you, it is worth exploring other solar and clean tech names via high growth tech and AI stocks to see what else fits your thesis.

With the stock trading above its consensus price target yet still at a steep discount to intrinsic value estimates, are investors staring at a rare mispricing in solar manufacturing, or is the market already baking in the reshoring upside?

Most Popular Narrative: 4.4% Overvalued

With Canadian Solar last closing at $24.35 against a narrative fair value of about $23.33, the valuation gap is narrow but telling for long term expectations.

Recent updates from Wall Street highlight a sharply improved near term narrative for Canadian Solar, but also underscore that execution and policy risks remain central to the valuation debate.

Want to see what is driving this upbeat long term view despite tighter margins and policy noise? The narrative quietly leans on surprisingly strong growth and richer future earnings power. Curious which precise revenue and profit assumptions tip the model toward a higher earnings multiple on tomorrow's cash flows? Read on to uncover the numbers behind that conviction.

Result: Fair Value of $23.33 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, execution could still stumble, especially if U.S. policy shifts or trade penalties tighten margins and undermine the economics of its reshoring build out.

Find out about the key risks to this Canadian Solar narrative.

Another Lens on Value

Step away from analyst targets and Canadian Solar looks very different. Our DCF model pegs fair value near $57.94 per share, around 58 percent above today’s price. If cash flows really compound as forecast, is the market badly misreading this cycle sensitive story?

Look into how the SWS DCF model arrives at its fair value.

Build Your Own Canadian Solar Narrative

If you see the story differently or simply want to stress test the assumptions yourself, you can build a custom view in minutes: Do it your way.

A great starting point for your Canadian Solar research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

Ready for more high conviction ideas?

Before you move on, lock in your next potential win by using the Simply Wall Street Screener to surface stocks that match your exact strategy and risk appetite.

- Capture powerful turnaround potential by scanning these 905 undervalued stocks based on cash flows that the market has not fully priced yet.

- Ride the next wave of digital disruption by targeting these 26 AI penny stocks shaping automation, data intelligence, and productivity breakthroughs.

- Strengthen your income stream by focusing on these 12 dividend stocks with yields > 3% that can support more reliable long term returns.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com