- PREMIUM

- LIVE QUOTES

- INSTITUTIONS

Index Options

Index Options State Street

State Street CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street JournalCanaan (NasdaqGM:CAN): Reassessing Valuation After a Volatile Year and Recent Share Price Rebound

Canaan (CAN) has been on a rough ride this year, but its recent rebound over the past 3 months is catching traders attention, especially given the sharp drawdown investors sat through earlier.

See our latest analysis for Canaan.

That rebound sits against a tough backdrop, with the 90 day share price return of 32.85% only partly offsetting a year to date share price decline of 57.81% and a 1 year total shareholder return of 68.67%. As a result, momentum is tentatively rebuilding from a deep drawdown.

If Canaan’s volatility has you thinking more broadly about opportunities in the sector, it is worth exploring high growth tech and AI stocks as a way to spot other potential movers in the space.

With shares still trading below analyst targets despite a sharp rebound and ongoing revenue growth, the key question now is whether Canaan remains a beaten down value play or if markets already reflect its future recovery.

Most Popular Narrative Narrative: 67.6% Undervalued

With Canaan last closing at $0.94 against a narrative fair value near $2.89, the story centers on whether aggressive growth assumptions can bridge that gap.

Persistent investment in next-generation ASIC chip development (e.g., imminent A-16 launch), along with broadening cooling options, enables product differentiation and pricing power amid hardware refresh cycles. This, in turn, should drive improved gross and net margins as mining efficiency demands rise.

Curious how rapid top line expansion, a sharp margin turnaround, and a richer future earnings multiple all combine to justify that upside? Unpack the full narrative.

Result: Fair Value of $2.89 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, this upside hinges on Bitcoin cycle dynamics and intensifying mining hardware competition, either of which could quickly erode Canaan’s projected growth path.

Find out about the key risks to this Canaan narrative.

Another Angle on Valuation

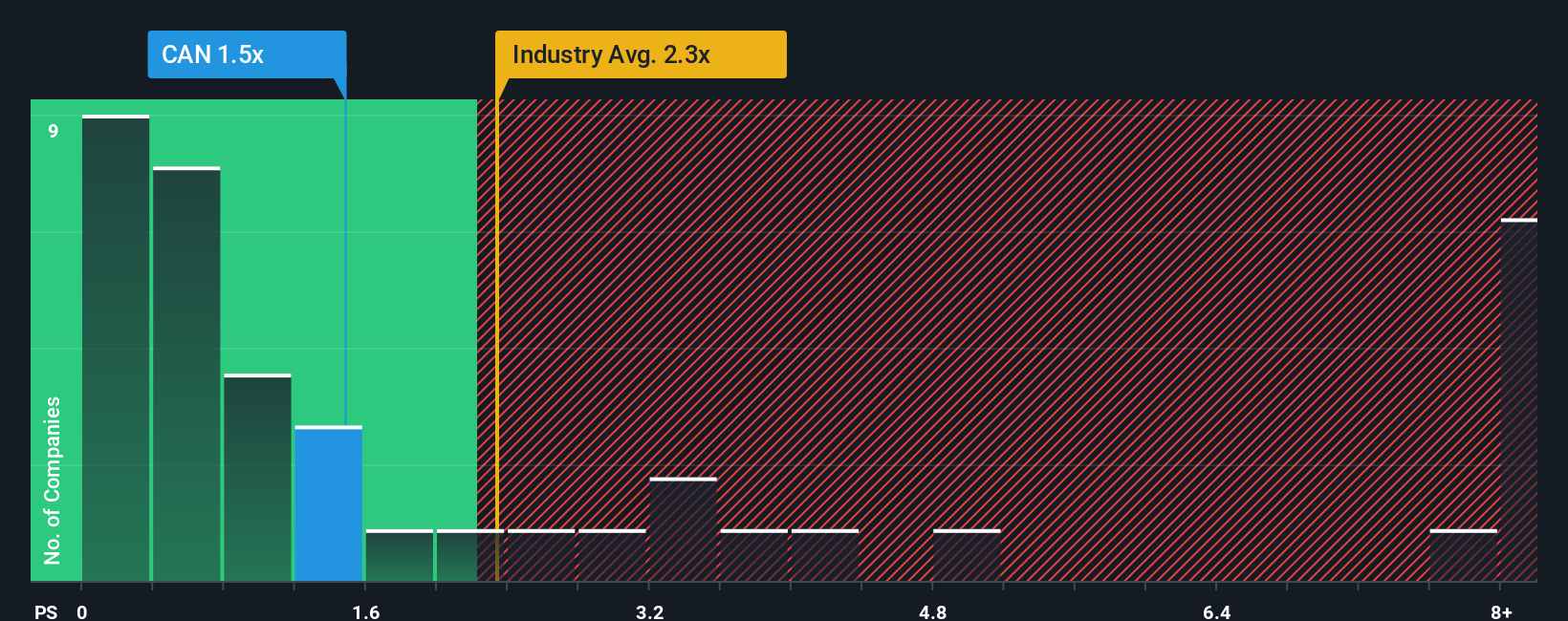

While the narrative fair value suggests big upside, today’s price-to-sales ratio of 1.5x paints a tighter picture. It is only slightly cheaper than the US tech industry at 1.6x but much richer than peers at 0.7x and its 1.2x fair ratio, hinting at limited margin for error if growth stumbles.

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Canaan Narrative

If you want to dig into the numbers yourself rather than rely on this view, you can quickly craft a personalised perspective in minutes with Do it your way.

A great starting point for your Canaan research is our analysis highlighting 1 key reward and 2 important warning signs that could impact your investment decision.

Ready for more high conviction ideas?

Do not stop with one stock; use the Simply Wall St Screener now to uncover focused opportunities other investors will only notice once the momentum is obvious.

- Capture early-stage growth potential by scanning these 3588 penny stocks with strong financials that already show strong balance sheets and fundamentals.

- Capitalize on the AI wave by targeting these 27 AI penny stocks positioned at the heart of machine learning and automation trends.

- Lock in quality at compelling prices with these 903 undervalued stocks based on cash flows that appear mispriced based on their future cash flows.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com