- PREMIUM

- LIVE QUOTES

- INSTITUTION

Index Options

Index Options State Street

State Street CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street JournalEven With A 26% Surge, Cautious Investors Are Not Rewarding Nippon Chemi-Con Corporation's (TSE:6997) Performance Completely

Nippon Chemi-Con Corporation (TSE:6997) shareholders would be excited to see that the share price has had a great month, posting a 26% gain and recovering from prior weakness. Looking back a bit further, it's encouraging to see the stock is up 38% in the last year.

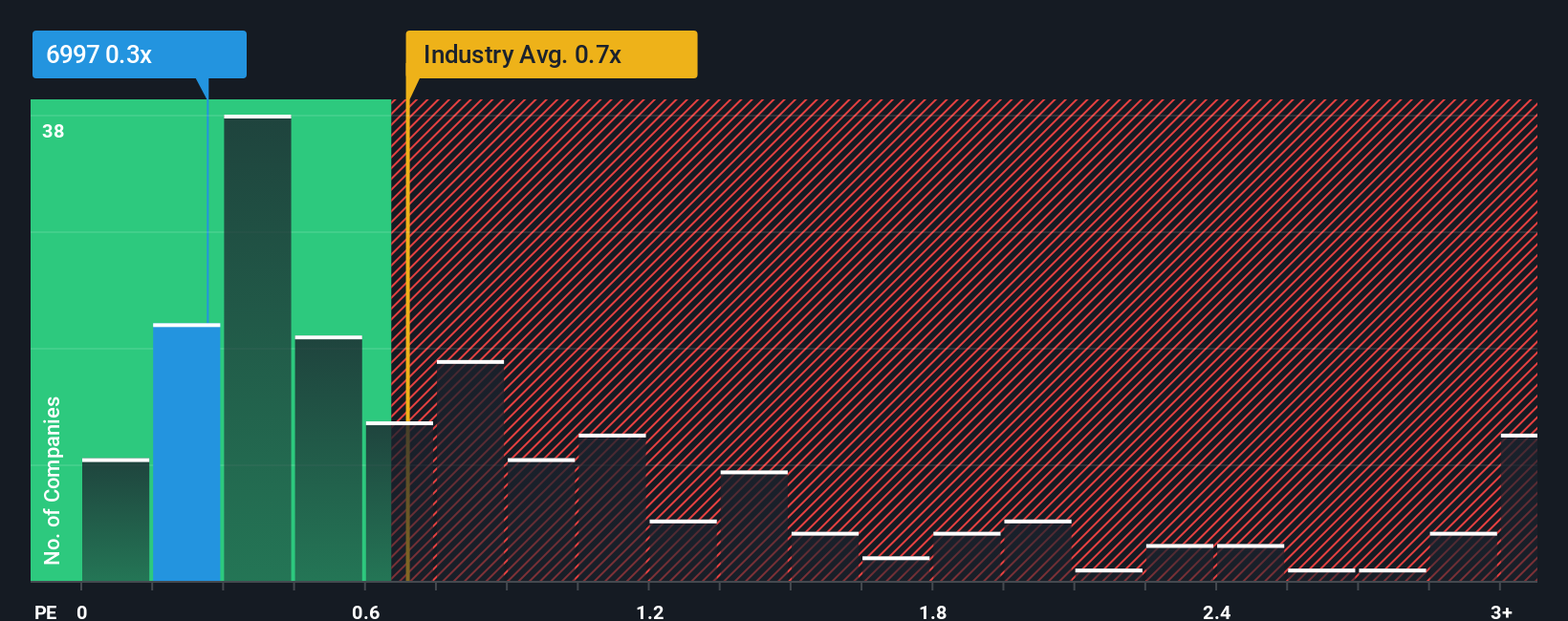

In spite of the firm bounce in price, you could still be forgiven for feeling indifferent about Nippon Chemi-Con's P/S ratio of 0.3x, since the median price-to-sales (or "P/S") ratio for the Electronic industry in Japan is also close to 0.7x. While this might not raise any eyebrows, if the P/S ratio is not justified investors could be missing out on a potential opportunity or ignoring looming disappointment.

See our latest analysis for Nippon Chemi-Con

How Nippon Chemi-Con Has Been Performing

Nippon Chemi-Con could be doing better as its revenue has been going backwards lately while most other companies have been seeing positive revenue growth. It might be that many expect the dour revenue performance to strengthen positively, which has kept the P/S from falling. You'd really hope so, otherwise you're paying a relatively elevated price for a company with this sort of growth profile.

Keen to find out how analysts think Nippon Chemi-Con's future stacks up against the industry? In that case, our free report is a great place to start.How Is Nippon Chemi-Con's Revenue Growth Trending?

There's an inherent assumption that a company should be matching the industry for P/S ratios like Nippon Chemi-Con's to be considered reasonable.

Retrospectively, the last year delivered a frustrating 2.5% decrease to the company's top line. The last three years don't look nice either as the company has shrunk revenue by 16% in aggregate. So unfortunately, we have to acknowledge that the company has not done a great job of growing revenue over that time.

Shifting to the future, estimates from the four analysts covering the company suggest revenue should grow by 10% over the next year. Meanwhile, the rest of the industry is forecast to only expand by 6.6%, which is noticeably less attractive.

With this in consideration, we find it intriguing that Nippon Chemi-Con's P/S is closely matching its industry peers. It may be that most investors aren't convinced the company can achieve future growth expectations.

What Does Nippon Chemi-Con's P/S Mean For Investors?

Its shares have lifted substantially and now Nippon Chemi-Con's P/S is back within range of the industry median. Typically, we'd caution against reading too much into price-to-sales ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

Despite enticing revenue growth figures that outpace the industry, Nippon Chemi-Con's P/S isn't quite what we'd expect. When we see a strong revenue outlook, with growth outpacing the industry, we can only assume potential uncertainty around these figures are what might be placing slight pressure on the P/S ratio. At least the risk of a price drop looks to be subdued, but investors seem to think future revenue could see some volatility.

Before you settle on your opinion, we've discovered 4 warning signs for Nippon Chemi-Con (2 don't sit too well with us!) that you should be aware of.

If strong companies turning a profit tickle your fancy, then you'll want to check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.