- PREMIUM

- LIVE QUOTES

- INSTITUTION

Index Options

Index Options State Street

State Street CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street JournalTop ASX Dividend Stocks To Consider In December 2025

As the Australian market navigates a cautious landscape, with telecoms leading amidst broader sector declines and rate pause expectations from the RBA, investors are keenly observing how these dynamics might influence dividend stocks. In such an environment, selecting robust dividend stocks involves looking for companies with strong fundamentals and consistent payout histories to potentially weather economic fluctuations.

Top 10 Dividend Stocks In Australia

| Name | Dividend Yield | Dividend Rating |

| Treasury Wine Estates (ASX:TWE) | 6.97% | ★★★★★☆ |

| Super Retail Group (ASX:SUL) | 5.90% | ★★★★★☆ |

| Sugar Terminals (NSX:SUG) | 7.86% | ★★★★★☆ |

| Steadfast Group (ASX:SDF) | 3.88% | ★★★★★☆ |

| Smartgroup (ASX:SIQ) | 5.62% | ★★★★★☆ |

| MFF Capital Investments (ASX:MFF) | 3.75% | ★★★★★☆ |

| Lindsay Australia (ASX:LAU) | 5.80% | ★★★★★☆ |

| Kina Securities (ASX:KSL) | 7.43% | ★★★★★☆ |

| Fiducian Group (ASX:FID) | 4.28% | ★★★★★☆ |

| Accent Group (ASX:AX1) | 7.37% | ★★★★★☆ |

Click here to see the full list of 32 stocks from our Top ASX Dividend Stocks screener.

Let's take a closer look at a couple of our picks from the screened companies.

Super Retail Group (ASX:SUL)

Simply Wall St Dividend Rating: ★★★★★☆

Overview: Super Retail Group Limited operates as a retailer of auto, sports, and outdoor leisure products in Australia and New Zealand, with a market cap of A$3.67 billion.

Operations: Super Retail Group Limited generates revenue from its segments including Rebel at A$1.36 billion, Macpac at A$231.40 million, Super Cheap Auto (SCA) at A$1.53 billion, and Boating, Camping and Fishing (BCF) at A$950.70 million.

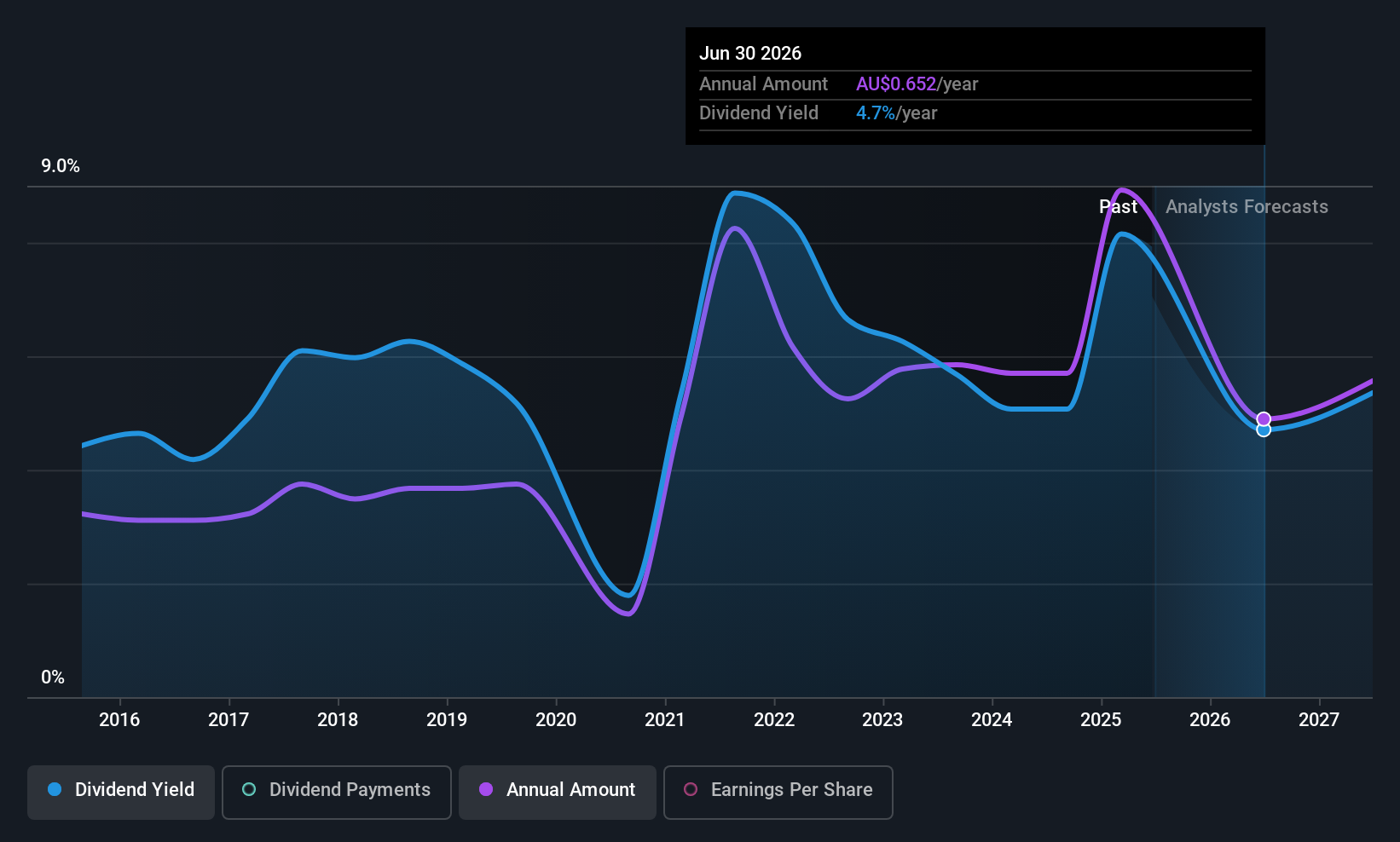

Dividend Yield: 5.9%

Super Retail Group's dividend yield is in the top 25% of the Australian market, supported by a manageable payout ratio of 67.2% from earnings and 52.7% from cash flows, suggesting sustainability. However, its dividend history has been volatile over the past decade. Recent leadership changes, including Paul Bradshaw's appointment as CEO, may impact strategic direction but have not yet affected dividend policies directly. The stock trades at a significant discount to its estimated fair value, presenting potential value opportunities for investors focused on dividends amidst industry peers.

- Dive into the specifics of Super Retail Group here with our thorough dividend report.

- The analysis detailed in our Super Retail Group valuation report hints at an deflated share price compared to its estimated value.

Southern Cross Electrical Engineering (ASX:SXE)

Simply Wall St Dividend Rating: ★★★★☆☆

Overview: Southern Cross Electrical Engineering Limited, with a market cap of A$625.04 million, offers electrical, instrumentation, communications, security, fire, and maintenance services and products across Australia.

Operations: Southern Cross Electrical Engineering Limited generates revenue primarily from the provision of electrical services, amounting to A$801.45 million.

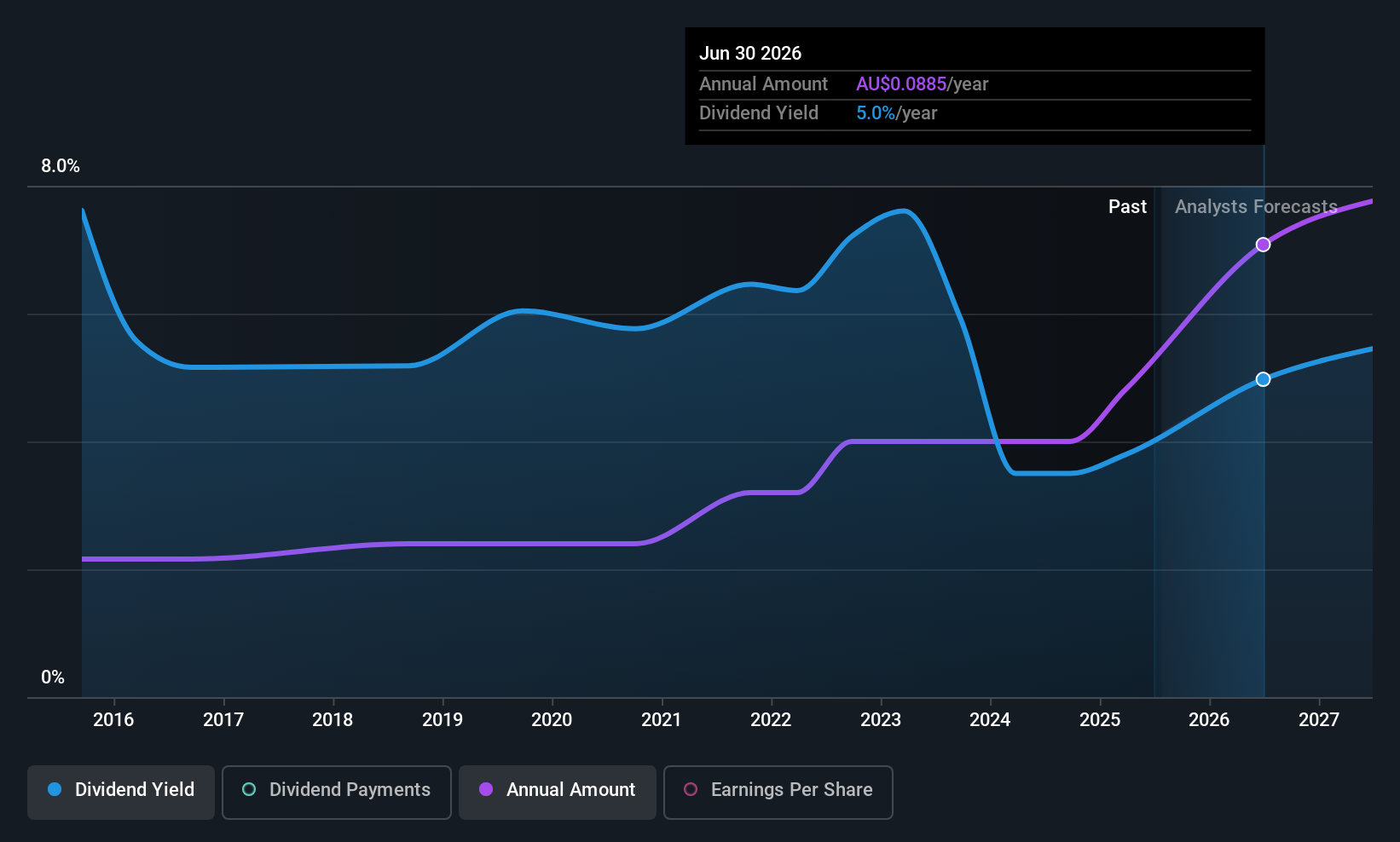

Dividend Yield: 3.2%

Southern Cross Electrical Engineering's dividend yield is below the top 25% of Australian payers, with a manageable payout ratio of 62.5% from earnings and 33.4% from cash flows, indicating sustainability. Despite a decade-long increase in dividends, payments have been volatile and unreliable. The stock trades at an 18.5% discount to its estimated fair value, offering potential value for investors prioritizing dividend coverage over high yields amidst recent insider selling activities.

- Click here to discover the nuances of Southern Cross Electrical Engineering with our detailed analytical dividend report.

- Our expertly prepared valuation report Southern Cross Electrical Engineering implies its share price may be too high.

Waterco (ASX:WAT)

Simply Wall St Dividend Rating: ★★★★☆☆

Overview: Waterco Limited manufactures, wholesales, and exports equipment and accessories for swimming pools, spa pools, spa baths, rural pumps, irrigation, and water treatment sectors across Australia, New Zealand, Asia, North America, and Europe with a market cap of A$174.41 million.

Operations: Waterco Limited's revenue segment from Building Products amounts to A$254.93 million.

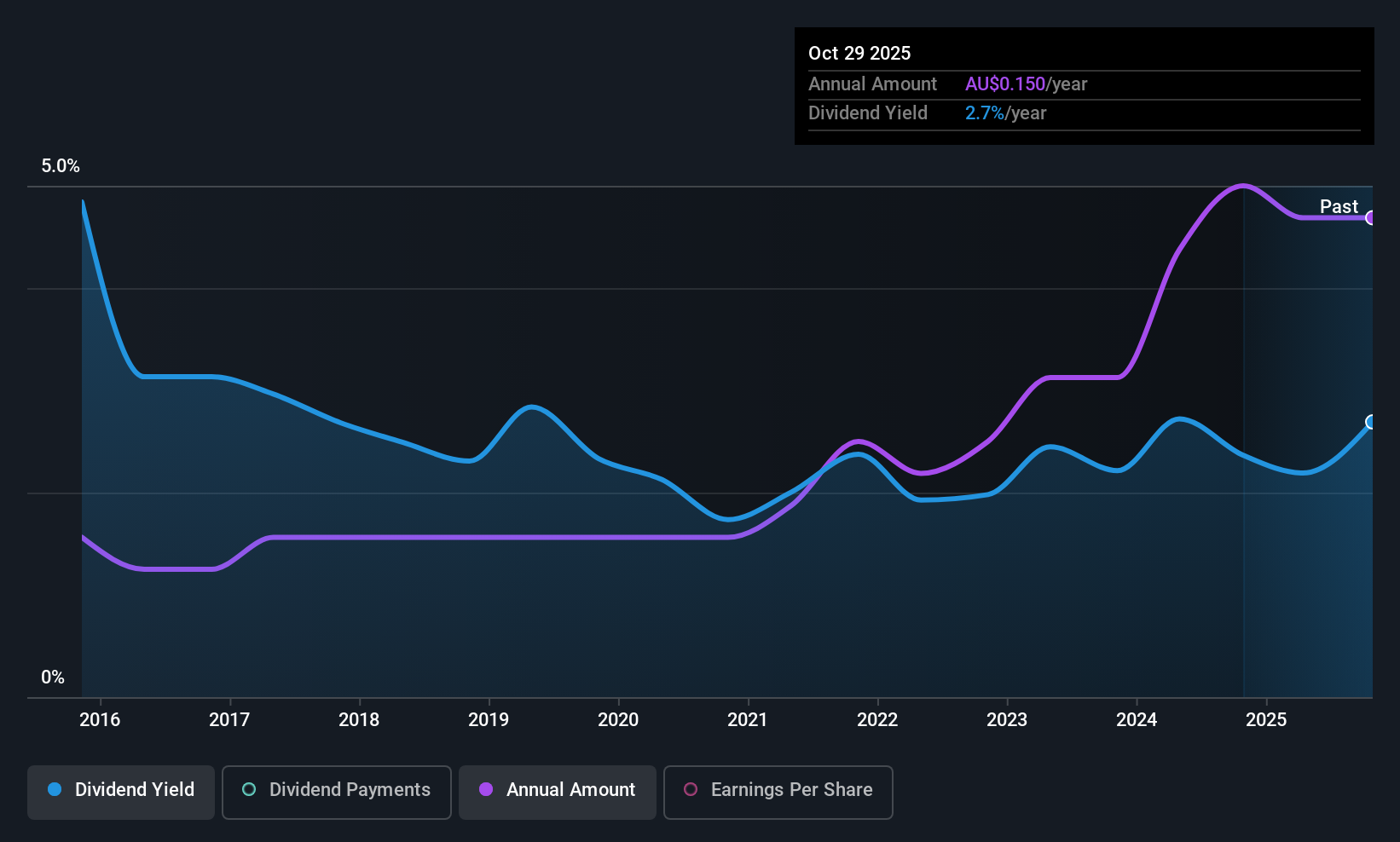

Dividend Yield: 3%

Waterco's dividend yield of 3.02% is below the top 25% of Australian payers, but its payout ratio of 55.1% from earnings and a cash payout ratio of 29.1% suggest sustainability. Dividends have grown over the past decade yet remain volatile and unreliable, with significant annual fluctuations. Currently trading at a 38.1% discount to estimated fair value, Waterco may attract investors focused on dividend coverage rather than high yields ahead of its Q1 2026 results announcement today.

- Delve into the full analysis dividend report here for a deeper understanding of Waterco.

- According our valuation report, there's an indication that Waterco's share price might be on the cheaper side.

Turning Ideas Into Actions

- Access the full spectrum of 32 Top ASX Dividend Stocks by clicking on this link.

- Are these companies part of your investment strategy? Use Simply Wall St to consolidate your holdings into a portfolio and gain insights with our comprehensive analysis tools.

- Maximize your investment potential with Simply Wall St, the comprehensive app that offers global market insights for free.

Want To Explore Some Alternatives?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com