- PREMIUM

- LIVE QUOTES

- INSTITUTION

Index Options

Index Options State Street

State Street CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street JournalHow Worthington’s Q2 FY26 Update And Automation Drive At Worthington Enterprises (WOR) Has Changed Its Investment Story

- In December 2025, Worthington Enterprises held its fiscal second quarter 2026 earnings call, following the release of results after the market closed on December 16, with a live webcast and year-long replay for investors.

- Alongside this update, investors focused on Worthington’s portfolio reshaping, modernization and automation efforts, and integration of acquisitions like Ragasco, which are intended to improve efficiency and margins over time.

- We’ll now examine how Worthington’s facility modernization and automation push may influence its broader investment narrative and future performance assumptions.

Uncover the next big thing with financially sound penny stocks that balance risk and reward.

Worthington Enterprises Investment Narrative Recap

To own Worthington Enterprises, you need to believe its modernization, automation and portfolio reshaping can translate into durable margin improvement despite uneven earnings and macro sensitivity. The upcoming fiscal Q2 2026 results call is a short term catalyst for clarity on these efficiency projects, while integration risk around acquisitions and ongoing M&A remains a key near term concern. This latest earnings date announcement itself does not fundamentally change those risks or catalysts.

The most relevant update here is Worthington’s continuing investment in facility modernization and automation, which the company and analysts link to potential net margin gains over time. Investors watching the Q2 2026 call may focus less on one quarter’s numbers and more on evidence that these projects and the integration of assets like Ragasco are tracking in line with expectations for efficiency and earnings growth.

Yet, even as modernization efforts progress, the risk that recent acquisitions and expansion initiatives may strain resources is something investors should be aware of...

Read the full narrative on Worthington Enterprises (it's free!)

Worthington Enterprises' narrative projects $1.4 billion revenue and $213.4 million earnings by 2028. This requires 7.6% yearly revenue growth and about a $117.3 million earnings increase from $96.1 million today.

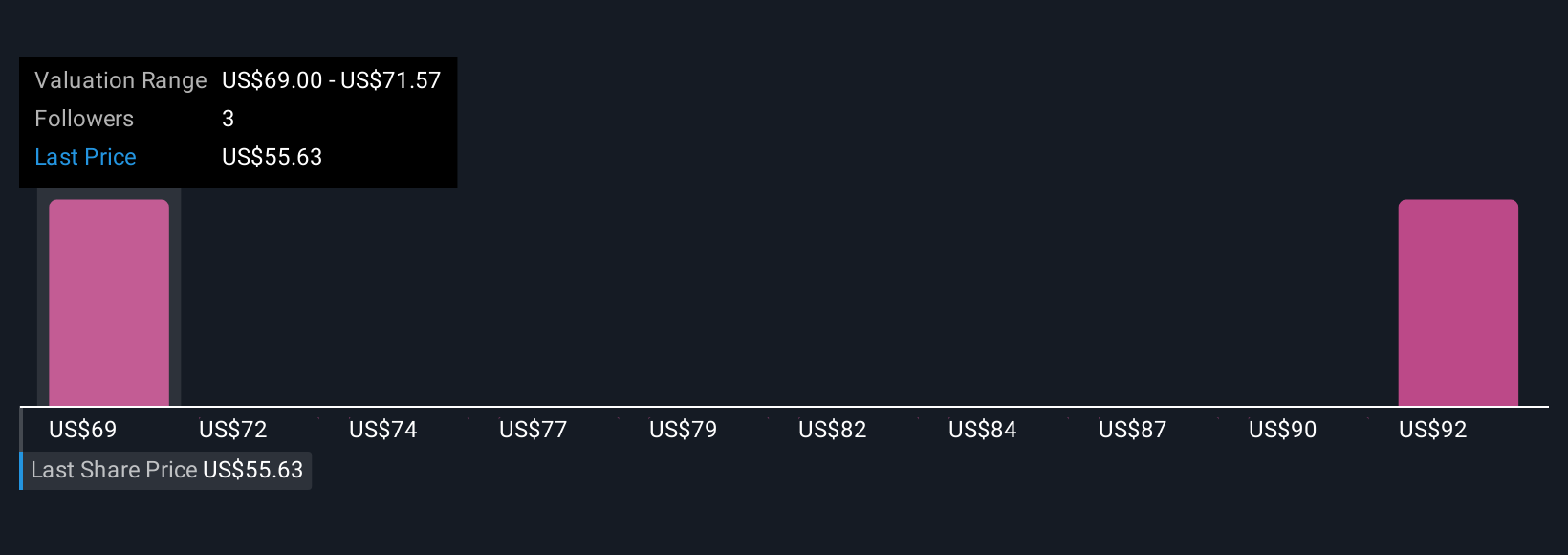

Uncover how Worthington Enterprises' forecasts yield a $69.00 fair value, a 25% upside to its current price.

Exploring Other Perspectives

Simply Wall St Community members currently see fair value clustered between about US$69 and US$92, illustrating how differently two individual investors can view the same stock. Against that backdrop, Worthington’s push into facility modernization and automation could influence how you weigh potential margin improvement against the execution and integration risks ahead.

Explore 2 other fair value estimates on Worthington Enterprises - why the stock might be worth as much as 67% more than the current price!

Build Your Own Worthington Enterprises Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Worthington Enterprises research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Worthington Enterprises research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Worthington Enterprises' overall financial health at a glance.

Want Some Alternatives?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- Outshine the giants: these 27 early-stage AI stocks could fund your retirement.

- Find companies with promising cash flow potential yet trading below their fair value.

- AI is about to change healthcare. These 30 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com