Reassessing Inspur Digital Enterprise Technology (SEHK:596)’s Valuation After Its Follow-On Equity Offering

Inspur Digital Enterprise Technology (SEHK:596) just wrapped up a follow on equity offering worth about HK$494 million, issuing over 67 million new ordinary shares at roughly HK$7.30 each.

See our latest analysis for Inspur Digital Enterprise Technology.

The follow on offering lands after a choppy stretch, with a roughly 9.7% 1 month share price return decline and a sharper 27.2% 3 month slide. This sits against a 5 year total shareholder return of over 300%, suggesting longer term momentum and growth expectations may remain intact even as near term sentiment cools.

If this capital raise has you rethinking your tech exposure, it could be a good moment to scout other high growth opportunities through high growth tech and AI stocks.

With the share price nearly halved from recent highs but still boasting robust growth and a sizeable discount to analyst targets, is Inspur Digital Enterprise Technology now undervalued, or is the market already pricing in its next leg of expansion?

Price to Earnings of 16x, Is it justified?

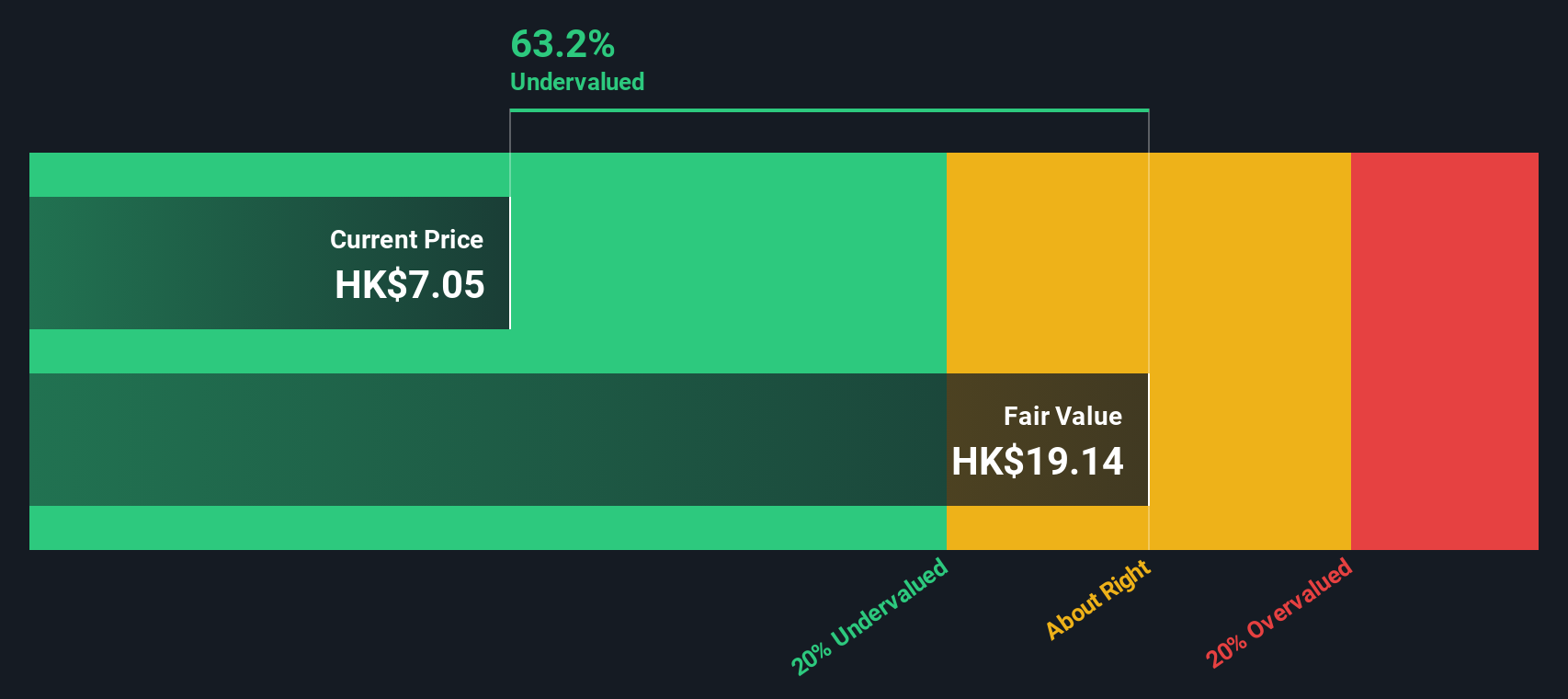

On a last close of HK$7.05, Inspur Digital Enterprise Technology trades on a price to earnings ratio of around 16 times, which screens as materially undervalued against both peers and its own fundamentals.

The price to earnings multiple compares the company’s market value with its current earnings. This is a core yardstick for software and cloud businesses where profitability is increasingly in focus. For Inspur Digital Enterprise Technology, this single figure captures how much investors are willing to pay for each unit of earnings in a sector that typically commands premium valuations.

Here, the market appears cautious. The stock trades at a 16 times price to earnings ratio, well below the estimated fair price to earnings of 26.3 times implied by our regression based fair ratio work. If sentiment or fundamentals continue to support current earnings growth trends, there is ample room for the valuation multiple to move closer to that fair level.

Relative comparisons sharpen the picture. The company’s 16 times price to earnings ratio stands at a steep discount to the Asian software industry average of about 26.2 times and to a peer group average of roughly 51.5 times, suggesting investors are paying far less for each dollar of earnings than they do elsewhere in the sector.

Explore the SWS fair ratio for Inspur Digital Enterprise Technology

Result: Price to Earnings of 16x (UNDERVALUED)

However, slowing revenue growth or a reversal in net income trends could quickly challenge the low valuation thesis and drag the multiple even lower.

Find out about the key risks to this Inspur Digital Enterprise Technology narrative.

Another View: Our DCF Lens

While the earnings multiple points to value, our DCF model is even more optimistic, suggesting fair value around HK$19.15, far above the current HK$7.05. If both are right, is the market simply behind the curve, or are expectations running too hot?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Inspur Digital Enterprise Technology for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 904 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Inspur Digital Enterprise Technology Narrative

If you see the story differently or want to dig into the numbers yourself, you can build a tailored view in minutes: Do it your way.

A great starting point for your Inspur Digital Enterprise Technology research is our analysis highlighting 5 key rewards and 1 important warning sign that could impact your investment decision.

Ready for your next investing move?

Before the market’s next big swing, lock in fresh ideas with targeted stock lists built from real data so you are not reacting after the opportunity passes.

- Capture potential turnaround winners by scanning these 3577 penny stocks with strong financials that pair low share prices with surprisingly resilient financials.

- Position ahead of structural growth by focusing on these 30 healthcare AI stocks transforming how medicine, diagnostics, and patient care are delivered.

- Strengthen your income strategy by targeting these 15 dividend stocks with yields > 3% that can keep your portfolio working even when markets cool.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com