- PREMIUM

- LIVE QUOTES

- INSTITUTION

Index Options

Index Options State Street

State Street CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street JournalPeloton (PTON) Valuation Check as New CEO Pushes AI Cross Training Revamp and Profit-Focused Turnaround

Peloton Interactive (PTON) is back in the spotlight after CEO Peter Stern laid out the company’s overhaul and new AI driven Cross Training Series, giving investors fresh context ahead of his appearance at Morgan Stanley’s Global Consumer and Retail Conference.

See our latest analysis for Peloton Interactive.

Despite the buzz around Peloton’s overhaul and AI driven launch, the stock’s recent momentum is still weak, with a 30 day share price return of minus 16.19 percent and a 1 year total shareholder return of minus 35.8 percent. This suggests sentiment remains cautious even as the turnaround narrative builds.

If you like Peloton’s tech angle but want more resilient momentum, this could be a good moment to explore high growth tech and AI stocks for other ideas in the space.

With shares still down nearly 95 percent from their peak yet trading at a steep discount to analyst targets, the key question now is whether Peloton is an undervalued turnaround story or if the market is already pricing in its next leg of growth.

Most Popular Narrative Narrative: 38.4% Undervalued

With Peloton Interactive’s fair value estimate of $10.43 sitting well above the last close at $6.42, the most followed narrative leans decisively optimistic on upside potential and future profitability.

The analysts have a consensus price target of $9.841 for Peloton Interactive based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $20.0, and the most bearish reporting a price target of just $5.0.

Want to see what turns today’s losses into future profits? This narrative leans on stronger margins, rising earnings, and a bold valuation multiple. Curious which assumptions really do the heavy lifting? Read on to uncover the projections behind that fair value call.

Result: Fair Value of $10.43 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, persistent subscription declines and rising competition could derail margin expansion and force analysts to reassess both growth assumptions and today’s seemingly attractive valuation.

Find out about the key risks to this Peloton Interactive narrative.

Another Lens on Valuation

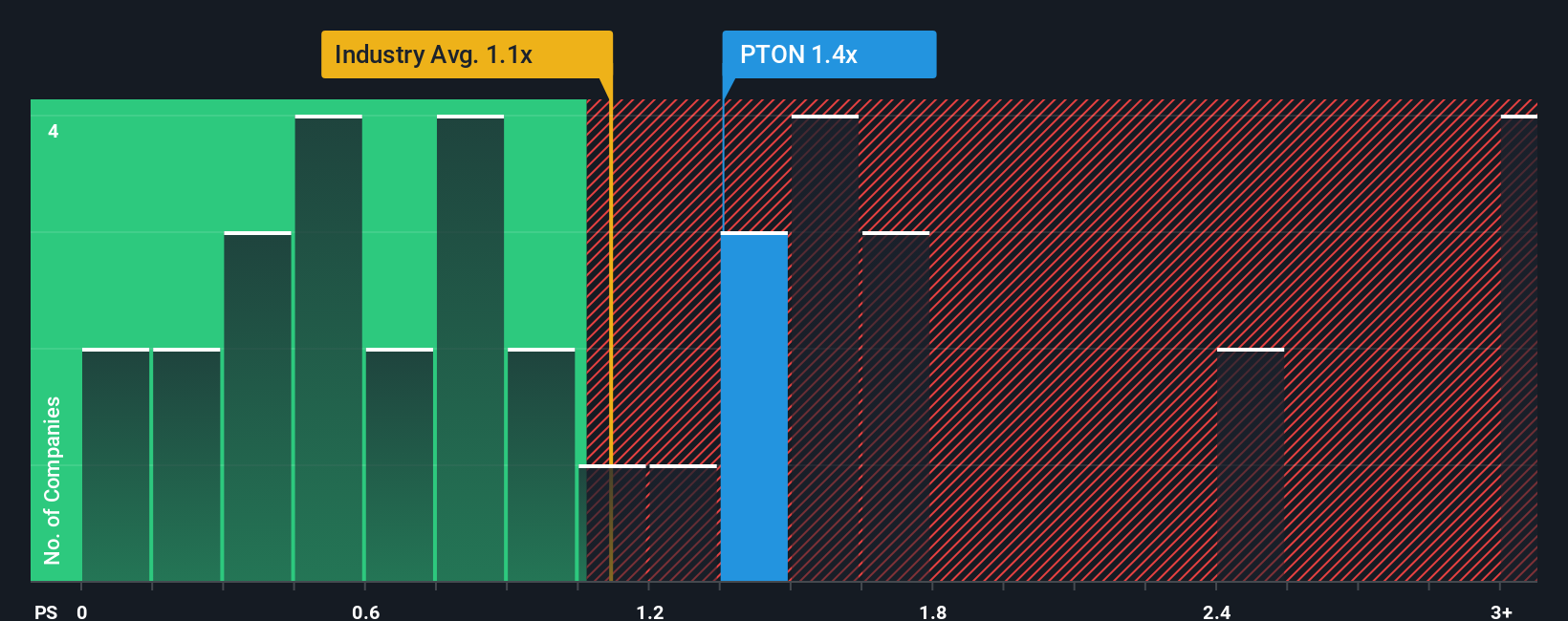

Step away from fair value models and Peloton starts to look pricey. On a price to sales of 1.1 times, it trades above both the US Leisure sector and close peers at 0.9 times, and even above its own fair ratio of 1 times. Is the market overpaying for a fragile turnaround?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Peloton Interactive Narrative

If you are not fully convinced by this takeaway and would rather dig into the numbers yourself, you can build a custom view in minutes, Do it your way.

A great starting point for your Peloton Interactive research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Before you move on, lock in a few more opportunities by using the Simply Wall St Screener to pinpoint stocks that match your strategy, not the crowd’s.

- Capture potential multi baggers early by scanning these 3578 penny stocks with strong financials packed with companies that already show stronger balance sheets and fundamentals than typical small caps.

- Capitalize on the AI wave by reviewing these 26 AI penny stocks, where innovation, data advantages, and scalable platforms could fuel the next leg of market leadership.

- Strengthen the core of your portfolio by focusing on value first using these 905 undervalued stocks based on cash flows that highlight stocks priced below their cash flow potential.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com