- PREMIUM

- LIVE QUOTES

- INSTITUTION

Index Options

Index Options State Street

State Street CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street JournalIs Micron Technology’s 171.6% 2025 Rally Still Supported by Its Fundamentals?

- Wondering if Micron Technology is still a smart buy after its huge run, or if you are late to the party? This breakdown will help you decide whether the current price really makes sense.

- The stock has rocketed higher, with shares up 171.6% year to date and 135.5% over the last year, even after a relatively flat last month and week with moves of around 0.3% and -0.1% respectively.

- Those gains have been driven by growing optimism around AI infrastructure demand, with Micron seen as a key supplier of high bandwidth memory and advanced DRAM that power data centers and next generation GPUs.

- Right now Micron earns a valuation score of 3/6. We will unpack what that means across different valuation approaches, before finishing with a more holistic way to judge whether the stock is truly priced for its future.

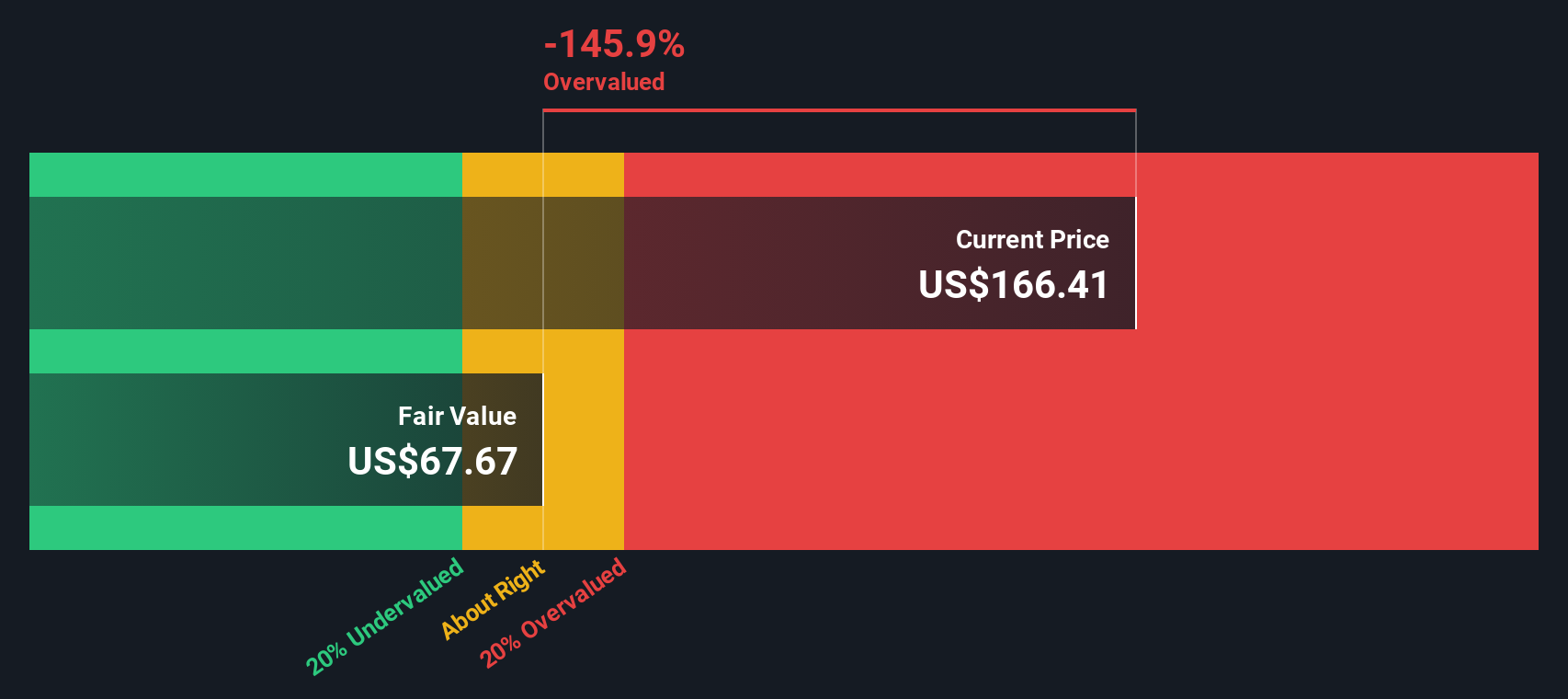

Approach 1: Micron Technology Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow model estimates what a company is worth today by projecting its future cash flows and then discounting them back to the present using a required rate of return.

For Micron Technology, the model starts with last twelve months Free Cash Flow of about $2.2 billion and uses analyst forecasts and longer term extrapolations to map out future cash generation. Analyst based estimates drive the nearer years, while Simply Wall St extends the projections further out, expecting Free Cash Flow to rise to around $10.6 billion by 2030.

These cash flows are discounted using a 2 Stage Free Cash Flow to Equity framework to arrive at an intrinsic value of roughly $101.06 per share. Compared with the current market price, this implies the stock is about 134.7% above the DCF based fair value, which indicates that investors are paying a substantial premium for future growth.

Result: OVERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Micron Technology may be overvalued by 134.7%. Discover 906 undervalued stocks or create your own screener to find better value opportunities.

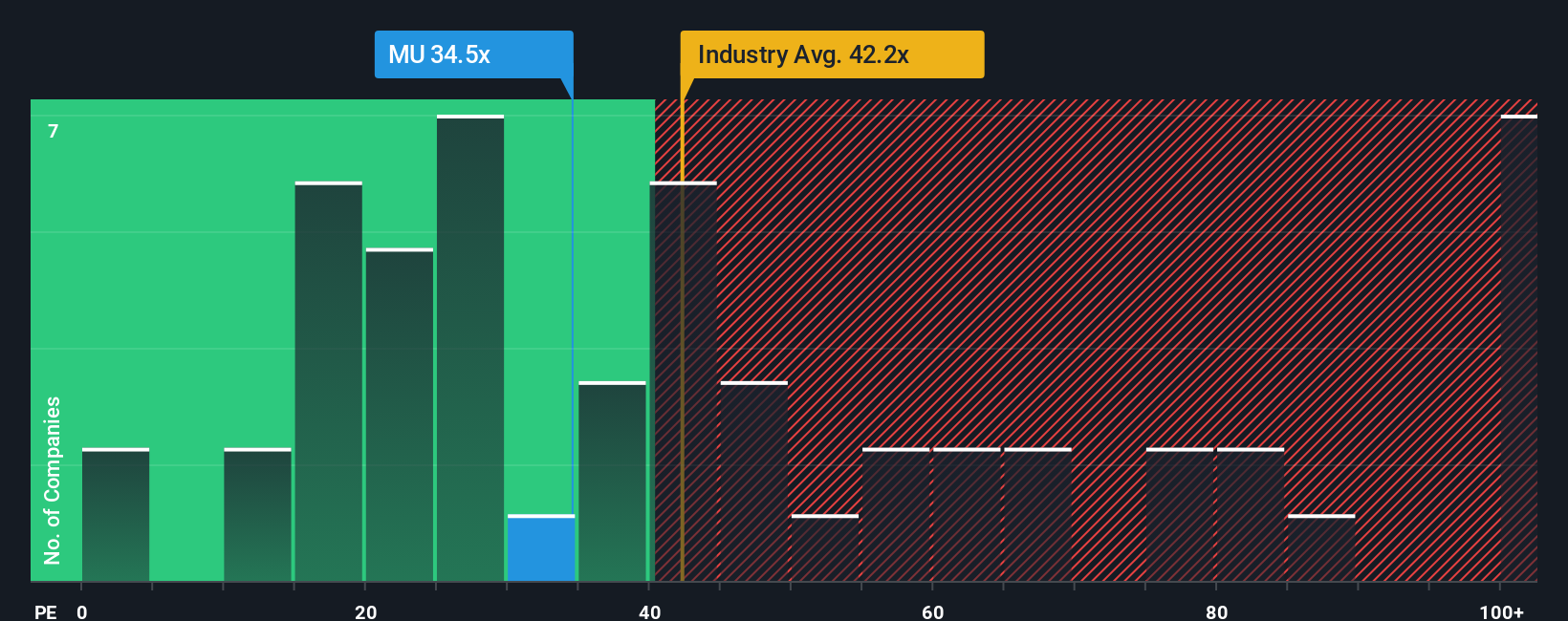

Approach 2: Micron Technology Price vs Earnings

For profitable companies like Micron, the price to earnings, or PE, ratio is a useful yardstick because it directly links what investors pay today to the profits the business is generating. A higher PE can be justified when investors expect stronger, more reliable earnings growth, while companies with slower growth or higher risk typically deserve a lower, more conservative multiple.

Micron currently trades at about 31.2x earnings, which sits below the broader semiconductor industry average of roughly 38.0x and well under a peer group average of around 90.2x. At first glance, that discount might suggest the stock is attractively priced, but raw comparisons like these do not fully capture Micron’s specific growth outlook, cyclicality, profitability, and risk profile.

That is where Simply Wall St’s Fair Ratio comes in. This proprietary metric estimates what Micron’s PE should be, given factors such as its earnings growth, industry, profit margins, market cap, and risk. For Micron, the Fair Ratio is 46.1x, meaning the shares trade materially below what this framework would imply is reasonable. Taken together, this indicates that, on a PE basis, Micron appears to be trading at a discount relative to this metric.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1442 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Micron Technology Narrative

Earlier we mentioned that there is an even better way to understand valuation. Let us introduce you to Narratives, which are simple, story driven forecasts where you spell out how you think Micron’s revenue, earnings, and margins will evolve. You then link that story to a financial model that calculates Fair Value, and compare it with today’s price to decide whether to buy, hold, or sell, all inside an easy to use tool on Simply Wall St’s Community page. The tool automatically refreshes when new news or earnings arrive. For Micron, one investor might build a bullish Narrative that assumes HBM demand stays red hot and justifies a Fair Value above $200 per share. Another might plug in more conservative growth, margin pressure, and a larger discount rate to arrive closer to $95. The platform lets you see, stress test, and refine these perspectives in real time so your decisions follow a clear, quantified story rather than just reacting to the share price.

Do you think there's more to the story for Micron Technology? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com