- PREMIUM

- LIVE QUOTES

- INSTITUTION

Index Options

Index Options State Street

State Street CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street JournalShareholders May Be Wary Of Increasing Wilton Resources Inc.'s (CVE:WIL) CEO Compensation Package

Key Insights

- Wilton Resources to hold its Annual General Meeting on 12th of December

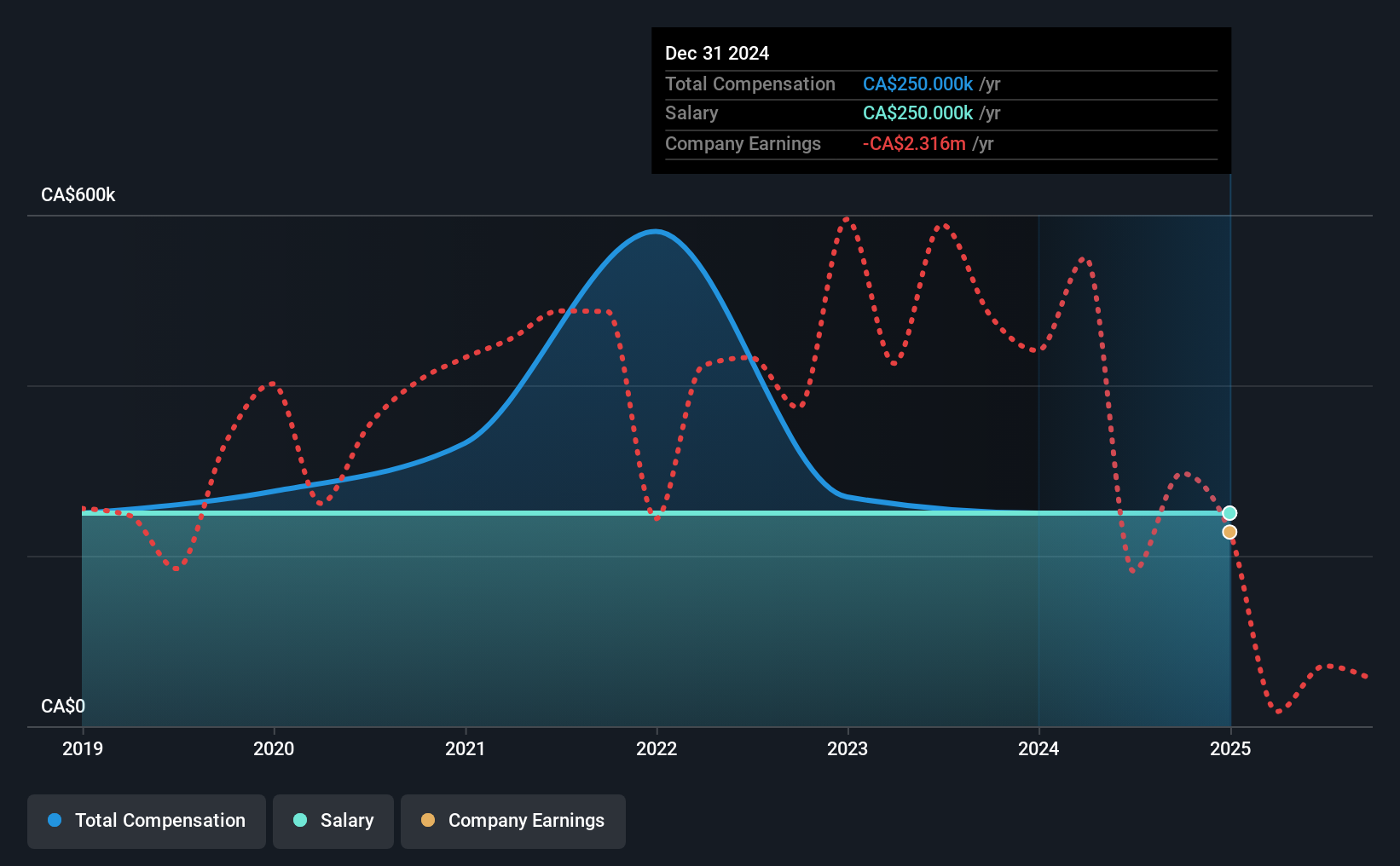

- Total pay for CEO Richard Anderson includes CA$250.0k salary

- The total compensation is similar to the average for the industry

- Wilton Resources' three-year loss to shareholders was 75% while its EPS was down 20% over the past three years

Wilton Resources Inc. (CVE:WIL) has not performed well recently and CEO Richard Anderson will probably need to up their game. Shareholders will be interested in what the board will have to say about turning performance around at the next AGM on 12th of December. They will also get a chance to influence managerial decision-making through voting on resolutions such as executive remuneration, which may impact firm value in the future. The data we present below explains why we think CEO compensation is not consistent with recent performance.

See our latest analysis for Wilton Resources

How Does Total Compensation For Richard Anderson Compare With Other Companies In The Industry?

According to our data, Wilton Resources Inc. has a market capitalization of CA$21m, and paid its CEO total annual compensation worth CA$250k over the year to December 2024. This was the same as last year. Notably, the salary of CA$250k is the entirety of the CEO compensation.

On comparing similar-sized companies in the Canadian Oil and Gas industry with market capitalizations below CA$277m, we found that the median total CEO compensation was CA$290k. This suggests that Wilton Resources remunerates its CEO largely in line with the industry average. Furthermore, Richard Anderson directly owns CA$240k worth of shares in the company.

| Component | 2024 | 2023 | Proportion (2024) |

| Salary | CA$250k | CA$250k | 100% |

| Other | - | - | - |

| Total Compensation | CA$250k | CA$250k | 100% |

Speaking on an industry level, nearly 38% of total compensation represents salary, while the remainder of 62% is other remuneration. Speaking on a company level, Wilton Resources prefers to tread along a traditional path, disbursing all compensation through a salary. If total compensation veers towards salary, it suggests that the variable portion - which is generally tied to performance, is lower.

Wilton Resources Inc.'s Growth

Over the last three years, Wilton Resources Inc. has shrunk its earnings per share by 20% per year. In the last year, its revenue is down 3.7%.

Few shareholders would be pleased to read that EPS have declined. And the fact that revenue is down year on year arguably paints an ugly picture. These factors suggest that the business performance wouldn't really justify a high pay packet for the CEO. We don't have analyst forecasts, but you could get a better understanding of its growth by checking out this more detailed historical graph of earnings, revenue and cash flow.

Has Wilton Resources Inc. Been A Good Investment?

With a total shareholder return of -75% over three years, Wilton Resources Inc. shareholders would by and large be disappointed. So shareholders would probably want the company to be less generous with CEO compensation.

To Conclude...

Wilton Resources pays CEO compensation exclusively through a salary, with non-salary compensation completely ignored. Not only have shareholders not seen a favorable return on their investment, but the business hasn't performed well either. Few shareholders would be willing to award the CEO with a pay raise. At the upcoming AGM, they can question the management's plans and strategies to turn performance around and reassess their investment thesis in regards to the company.

CEO compensation is an important area to keep your eyes on, but we've also need to pay attention to other attributes of the company. We did our research and identified 3 warning signs (and 2 which can't be ignored) in Wilton Resources we think you should know about.

Important note: Wilton Resources is an exciting stock, but we understand investors may be looking for an unencumbered balance sheet and blockbuster returns. You might find something better in this list of interesting companies with high ROE and low debt.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.