- PREMIUM

- LIVE QUOTES

- INSTITUTION

Index Options

Index Options State Street

State Street CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street JournalSmurfit Westrock’s US$1.3 Billion Refinancing And Share Count Update Might Change The Case For Investing In Smurfit Westrock (SW)

- In early December 2025, Smurfit Westrock Plc reported that it had issued 522,189,716 Ordinary Shares with no treasury holdings, and separately completed US$1.30 billion of new notes through subsidiaries to refinance existing senior debt.

- This combination of a clarified share count and a sizable refinancing package gives investors fresh insight into both ownership structure and balance sheet flexibility.

- Next, we’ll examine how this US$1.30 billion refinancing effort may influence Smurfit Westrock’s investment narrative around margins and earnings growth.

AI is about to change healthcare. These 30 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

Smurfit Westrock Investment Narrative Recap

To own Smurfit Westrock, you need to believe the combined group can turn a low margin, capital intensive packaging platform into a higher return, cash generative business through synergies, asset rationalization, and more profitable contracts. The clarified share count and US$1.30 billion refinancing do not materially change that near term, but they do tighten the focus on the key catalyst of margin expansion and the ongoing risk that structurally weak volumes and pricing could stall earnings progress.

Among the recent updates, the US$1.30 billion in new notes stands out as most relevant here, because it directly affects how much financial headroom Smurfit Westrock has to fund integration, efficiency projects, and capacity resets that underpin the margin and earnings improvement story. At the same time, refinancing does not remove underlying pressures from overcapacity, cost inflation in Europe, or the need to exit loss making contracts in North America to unlock better profitability.

Yet behind the refinancing headlines, a less visible risk investors should be aware of is the industry overcapacity that could...

Read the full narrative on Smurfit Westrock (it's free!)

Smurfit Westrock's narrative projects $33.9 billion revenue and $2.2 billion earnings by 2028. This requires 3.2% yearly revenue growth and about a $1.8 billion earnings increase from $352.0 million today.

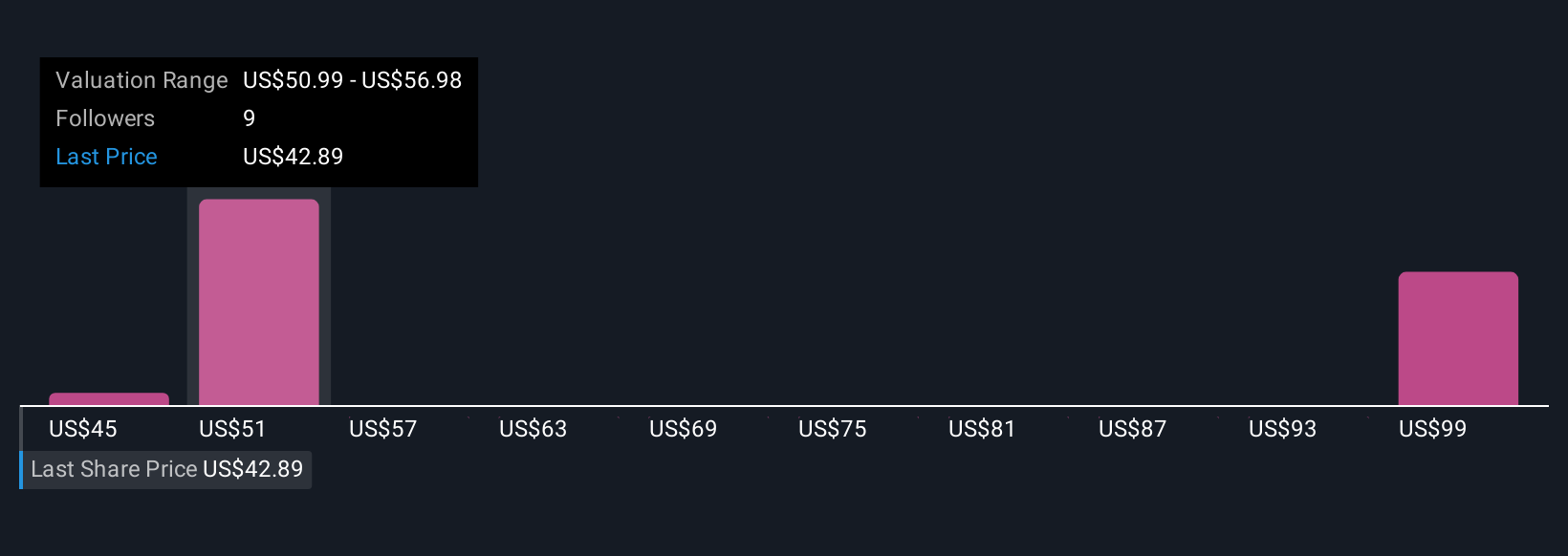

Uncover how Smurfit Westrock's forecasts yield a $53.73 fair value, a 49% upside to its current price.

Exploring Other Perspectives

Four fair value estimates from the Simply Wall St Community span roughly US$45 to about US$84 per share, showing how widely views on upside can differ. Set against this, the key earnings catalyst still hinges on whether Smurfit Westrock can lift margins in the face of volume and pricing risks, which could have a major bearing on how those community expectations ultimately play out.

Explore 4 other fair value estimates on Smurfit Westrock - why the stock might be worth just $45.00!

Build Your Own Smurfit Westrock Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Smurfit Westrock research is our analysis highlighting 4 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Smurfit Westrock research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Smurfit Westrock's overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

- We've found 15 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

- Trump has pledged to "unleash" American oil and gas and these 22 US stocks have developments that are poised to benefit.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com