- PREMIUM

- LIVE QUOTES

- INSTITUTION

Index Options

Index Options State Street

State Street CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street JournalWe Think Pharma Equity Group (CPH:PEG) Has A Fair Chunk Of Debt

Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. As with many other companies Pharma Equity Group A/S (CPH:PEG) makes use of debt. But is this debt a concern to shareholders?

Why Does Debt Bring Risk?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first step when considering a company's debt levels is to consider its cash and debt together.

How Much Debt Does Pharma Equity Group Carry?

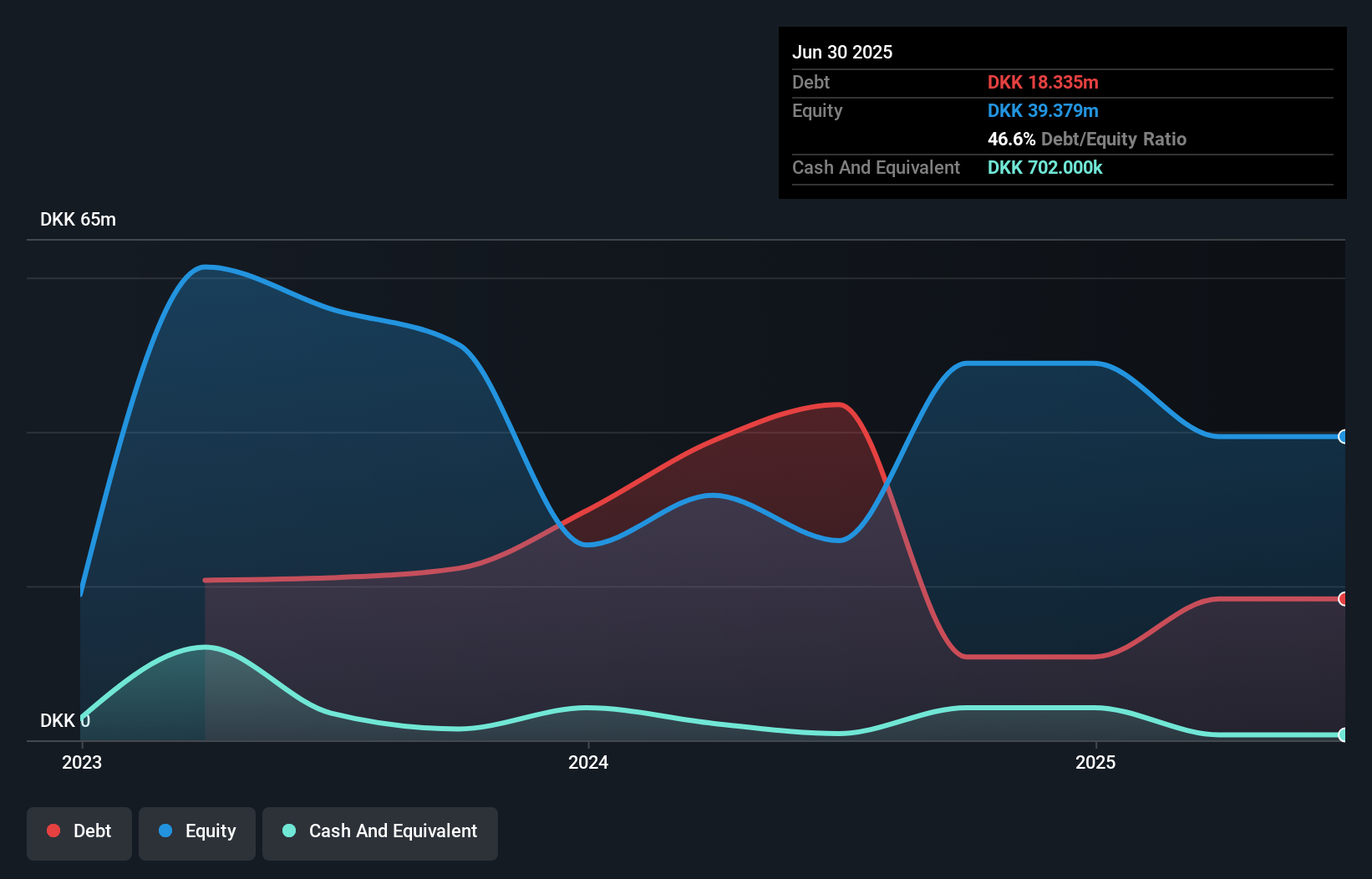

As you can see below, Pharma Equity Group had kr.18.3m of debt at June 2025, down from kr.43.5m a year prior. However, it also had kr.702.0k in cash, and so its net debt is kr.17.6m.

How Healthy Is Pharma Equity Group's Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Pharma Equity Group had liabilities of kr.7.69m due within 12 months and liabilities of kr.15.2m due beyond that. Offsetting these obligations, it had cash of kr.702.0k as well as receivables valued at kr.60.0m due within 12 months. So it can boast kr.37.8m more liquid assets than total liabilities.

This excess liquidity suggests that Pharma Equity Group is taking a careful approach to debt. Due to its strong net asset position, it is not likely to face issues with its lenders. The balance sheet is clearly the area to focus on when you are analysing debt. But it is Pharma Equity Group's earnings that will influence how the balance sheet holds up in the future. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

See our latest analysis for Pharma Equity Group

Given it has no significant operating revenue at the moment, shareholders will be hoping Pharma Equity Group can make progress and gain better traction for the business, before it runs low on cash.

Caveat Emptor

Importantly, Pharma Equity Group had an earnings before interest and tax (EBIT) loss over the last year. Its EBIT loss was a whopping kr.18m. On a more positive note, the company does have liquid assets, so it has a bit of time to improve its operations before the debt becomes an acute problem. But we'd want to see some positive free cashflow before spending much time on trying to understand the stock. This one is a bit too risky for our liking. There's no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet. Be aware that Pharma Equity Group is showing 4 warning signs in our investment analysis , and 2 of those make us uncomfortable...

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.