- PREMIUM

- LIVE QUOTES

- INSTITUTION

Index Options

Index Options State Street

State Street CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street JournalDoes BAC’s New 1%–4% Crypto Allocation Shift Change the Bull Case for Bank of America (BAC)?

- In recent days, Bank of America has shifted its wealth management stance by allowing advisers to recommend a 1%–4% portfolio allocation to digital assets and beginning research coverage of several spot bitcoin ETFs, reversing its previous prohibition on crypto advice.

- This policy change positions the bank more directly in the growing market for regulated crypto exposure, aligning its wealth platform with evolving client demand and competitors’ digital asset offerings.

- With this new crypto allocation guidance now in place, we’ll examine how expanding bitcoin ETF coverage could influence Bank of America’s investment narrative.

These 13 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

Bank of America Investment Narrative Recap

To own Bank of America, you need to believe it can keep turning its scale, digital investments, and diversified banking into steady earnings and capital returns. The new 1% to 4% crypto allocation guidance adds a new talking point, but the main near term catalyst still looks like how effectively the bank balances loan growth and asset repricing against funding costs. The biggest current risk remains pressure on net interest income if deposit competition and rate shifts compress margins.

In my view, the most relevant recent development alongside the crypto move is Bank of America’s continued share repurchases under its US$40 billion authorization, which directly tie into the earnings per share growth catalyst. As the bank layers digital asset access and AI driven initiatives onto an already active capital return program, the key question is how sustainably it can support buybacks and dividends if funding costs rise or credit conditions soften.

Yet behind the crypto headlines, investors should still pay close attention to the risk that higher deposit costs could...

Read the full narrative on Bank of America (it's free!)

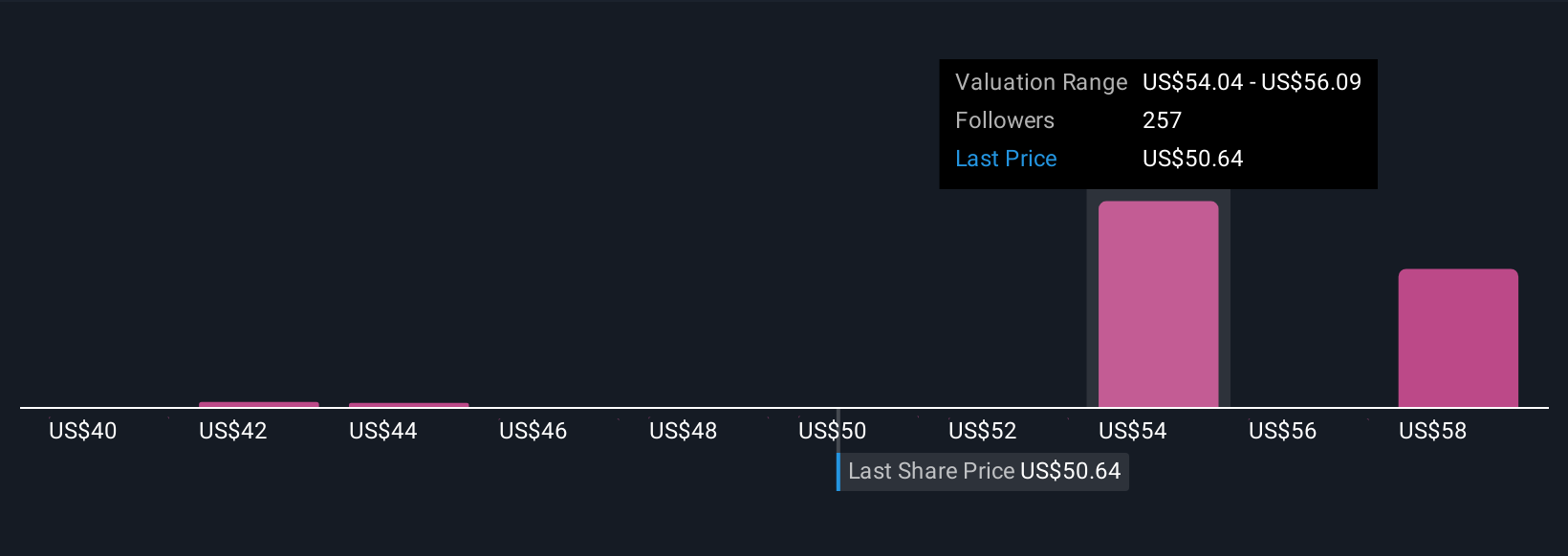

Bank of America's narrative projects $122.0 billion revenue and $32.9 billion earnings by 2028. This requires 7.4% yearly revenue growth and a $6.3 billion earnings increase from $26.6 billion today.

Uncover how Bank of America's forecasts yield a $58.90 fair value, a 9% upside to its current price.

Exploring Other Perspectives

Fourteen fair value estimates from the Simply Wall St Community span roughly US$43 to US$59 per share, showing how far apart individual views can be. Against this backdrop, the risk that rising competition for deposits could pressure Bank of America’s net interest income gives you one more reason to compare several perspectives before forming your own view.

Explore 14 other fair value estimates on Bank of America - why the stock might be worth as much as 9% more than the current price!

Build Your Own Bank of America Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Bank of America research is our analysis highlighting 4 key rewards that could impact your investment decision.

- Our free Bank of America research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Bank of America's overall financial health at a glance.

Curious About Other Options?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- Find companies with promising cash flow potential yet trading below their fair value.

- Trump's oil boom is here - pipelines are primed to profit. Discover the 22 US stocks riding the wave.

- We've found 15 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com