- PREMIUM

- LIVE QUOTES

- INSTITUTION

Index Options

Index Options State Street

State Street CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street JournalIs Tripadvisor A Hidden Opportunity After Years of Share Price Declines?

- Wondering if Tripadvisor at around $15 a share is a hidden deal or a value trap? Let us unpack what the market is really pricing in and whether the risk reward still stacks up for long term investors.

- The stock is up about 3% over the last week but roughly flat over the past month, and it has only gained around 2% year to date and 6.9% over the last year after steep declines of 17.1% over 3 years and 46.1% over 5 years. That mix of modest recent gains and deep longer term drawdowns often signals changing sentiment, but not yet a full comeback.

- Recently, Tripadvisor has stayed in focus as investors weigh its position in online travel alongside shifting consumer demand and competitive pressure from larger platforms. Strategic moves and ongoing debates about the future of its core review and experiences ecosystem are shaping how the market is reassessing its long term prospects.

- On our valuation checks, Tripadvisor scores just 2 out of 6. This suggests the market may still be cautious about its fundamentals. Next, we will walk through different valuation approaches to see what they imply for fair value today. We will then finish with a more holistic way to judge whether the stock really fits your strategy.

Tripadvisor scores just 2/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: Tripadvisor Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow model estimates what a company is worth by projecting its future cash flows and then discounting them back to today, to reflect risk and the time value of money.

For Tripadvisor, the latest twelve month Free Cash Flow is about $270.5 Million. Analysts and extrapolations used in the 2 Stage Free Cash Flow to Equity model see cash flows rising gradually over time, with projected Free Cash Flow of around $341.1 Million in 2035. Simply Wall St uses detailed analyst estimates for the early years and then extends that trend further out to build a ten year view.

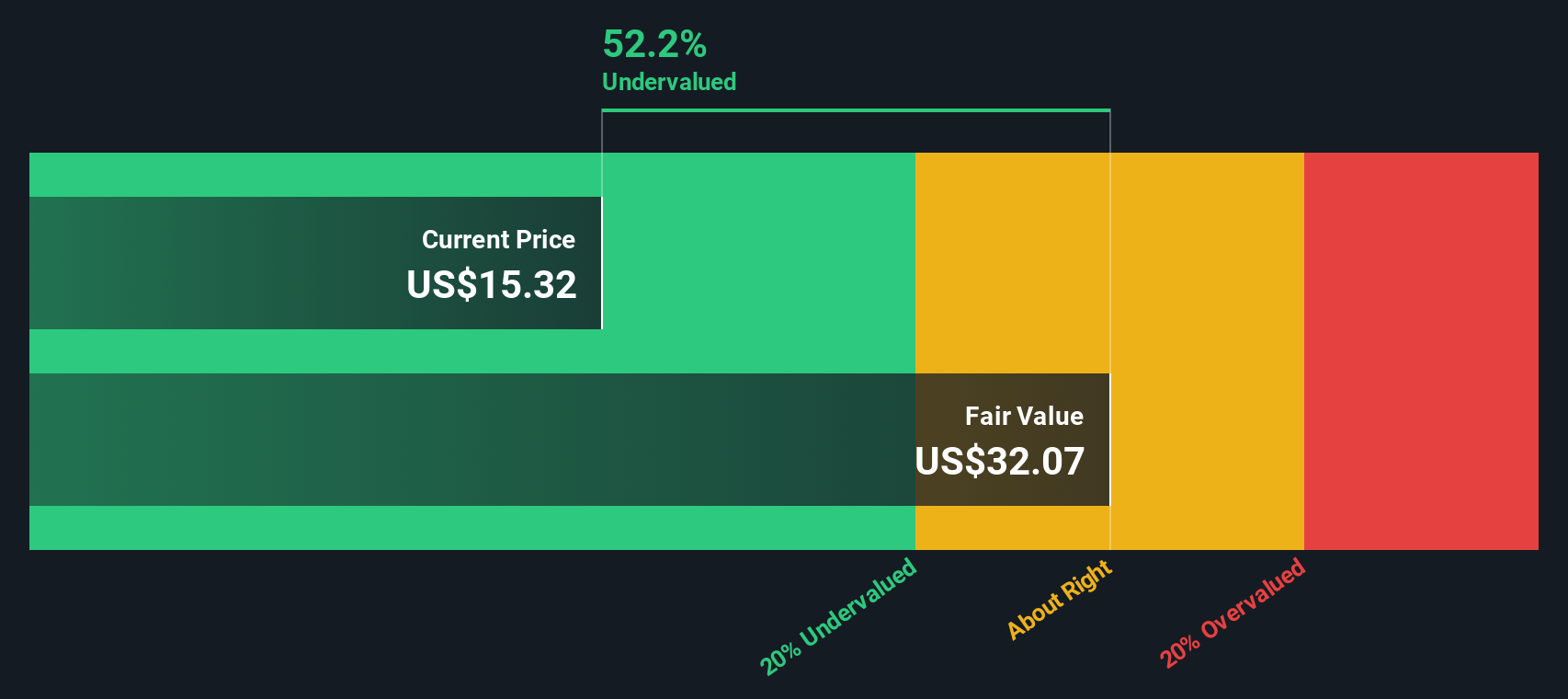

When all those future $ cash flows are discounted back, the intrinsic value comes out at roughly $31.92 per share. With the stock trading near $15, the DCF implies Tripadvisor is about 52.0% undervalued on this measure, indicating a sizable margin of safety if the cash flow path proves accurate.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Tripadvisor is undervalued by 52.0%. Track this in your watchlist or portfolio, or discover 906 more undervalued stocks based on cash flows.

Approach 2: Tripadvisor Price vs Earnings

For a profitable business like Tripadvisor, the Price to Earnings, or PE, ratio is a useful way to see how much investors are paying for each dollar of current earnings. It captures not only what the company is earning today, but also how the market feels about its future, since higher growth and lower perceived risk usually justify a higher PE multiple.

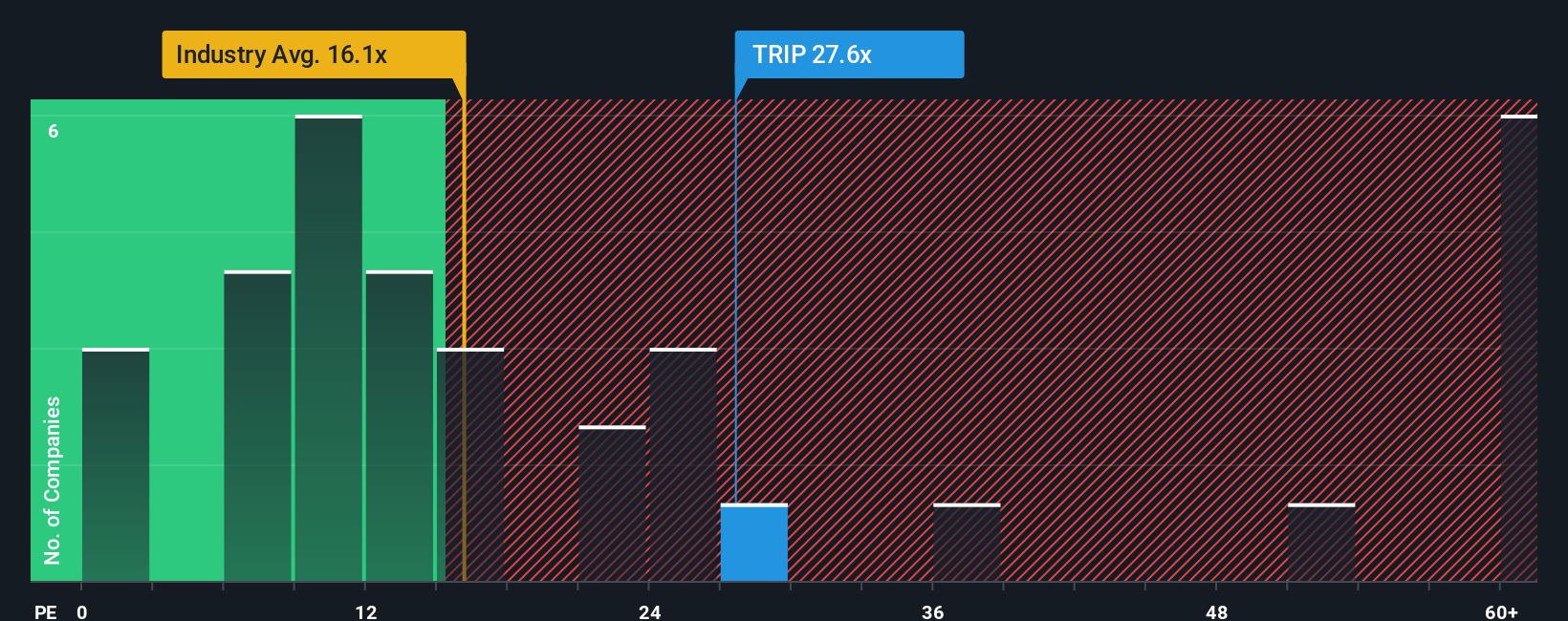

Tripadvisor currently trades on a PE of about 22.7x, which is richer than both the Interactive Media and Services industry average of roughly 17.2x and its broader peer group at around 19.3x. On the surface, that premium suggests the market is expecting better growth or lower risk than the typical peer.

Simply Wall St also calculates a Fair Ratio of 20.7x, an in house estimate of what Tripadvisor’s PE should be after factoring in its earnings growth outlook, profitability, industry, market cap and specific risks. Because it blends these fundamentals rather than relying only on simple comparisons, the Fair Ratio gives a more tailored benchmark than just lining the stock up against peers or the sector. With the actual PE at 22.7x versus a Fair Ratio of 20.7x, Tripadvisor screens as modestly overvalued on this metric.

Result: OVERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1442 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Tripadvisor Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives. Narratives let you connect your view of Tripadvisor’s story, such as how fast its experiences marketplace grows or how much AI improves margins, to a concrete forecast for future revenue, earnings and profitability, and then to a Fair Value you can easily compare with today’s share price.

On Simply Wall St’s Community page, Narratives are an accessible tool used by millions of investors to turn their assumptions about key drivers, like Tripadvisor’s organic traffic trends or competitive pressures, into dynamic models that automatically update when new information, such as earnings reports or major news, is released.

This makes it much simpler to decide how to approach the stock, because you can see at a glance whether your Narrative’s Fair Value is above or below the current market price, and adjust your stance as the facts change rather than relying on static ratios alone.

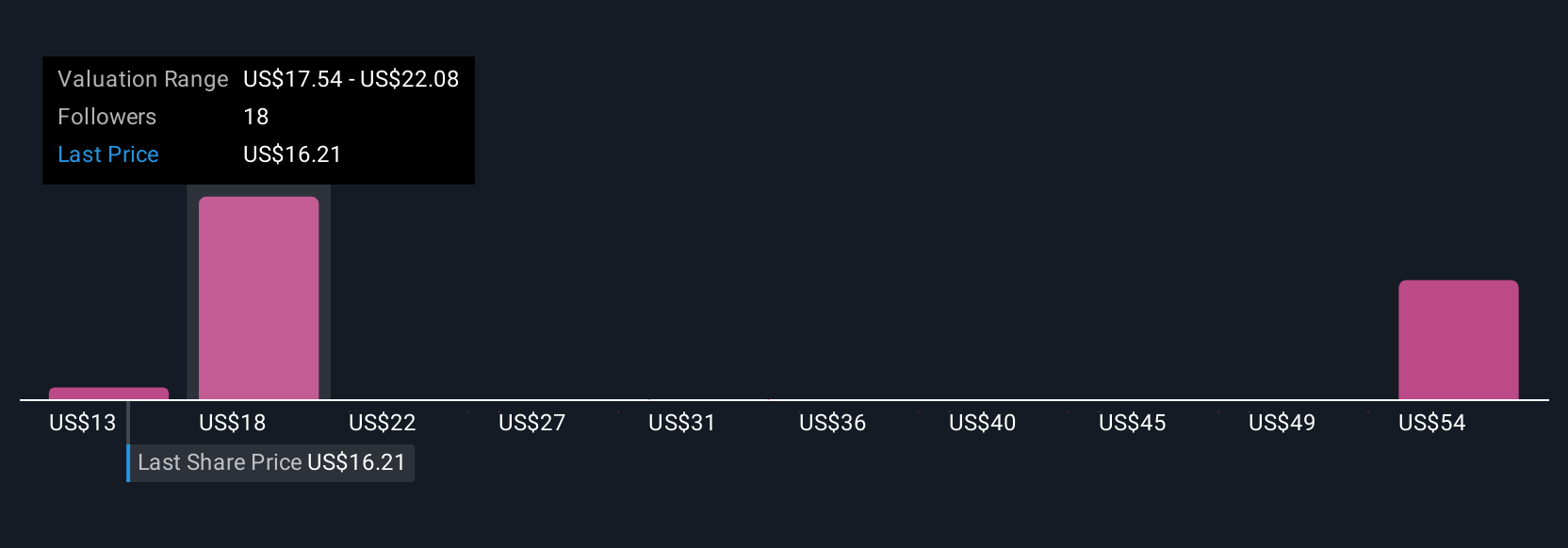

For example, one investor’s Narrative for Tripadvisor might justify a Fair Value near the high end of recent targets around $25 if they expect resilient growth and margin expansion, while a more cautious Narrative could land closer to $13.50 if they see competitive and traffic headwinds persisting.

Do you think there's more to the story for Tripadvisor? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com