- PREMIUM

- LIVE QUOTES

- INSTITUTION

Index Options

Index Options State Street

State Street CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

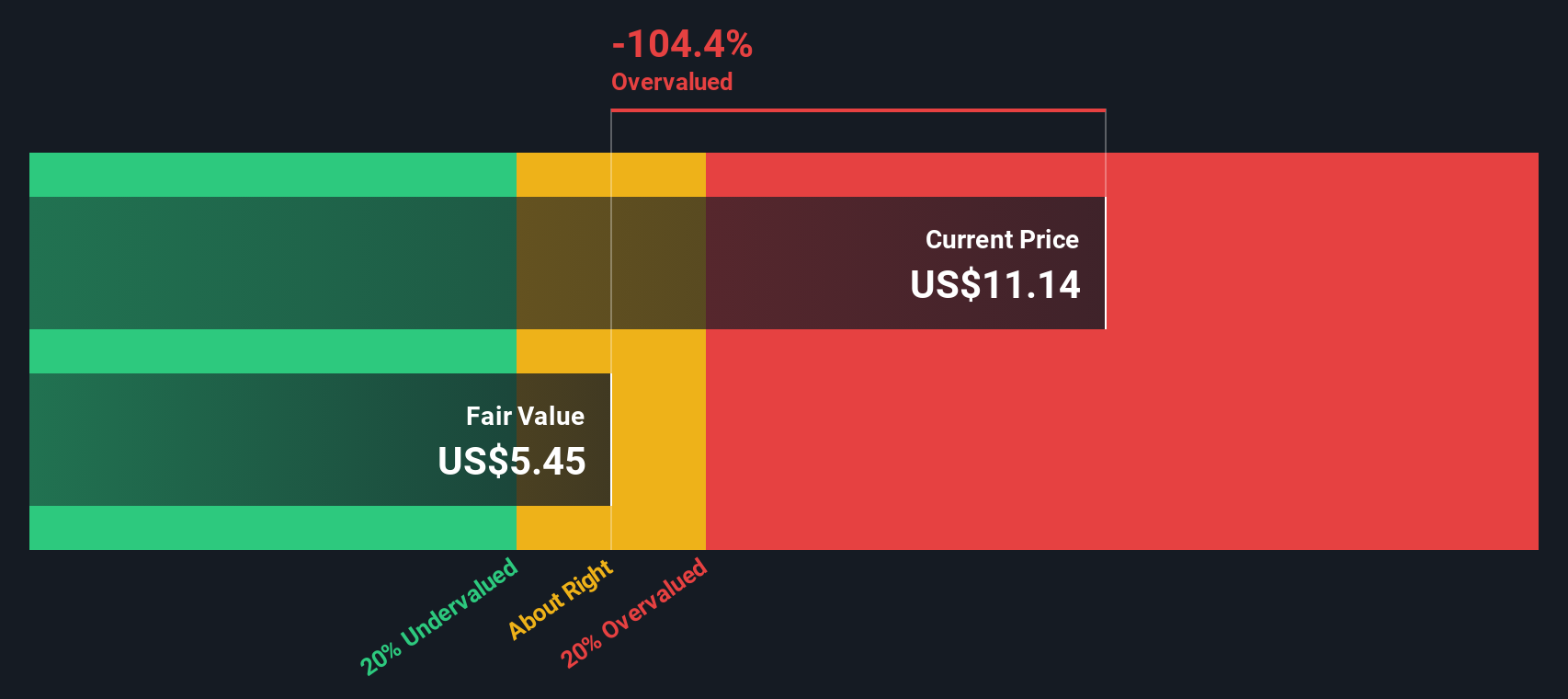

Wall Street JournalHas DigitalBridge’s Recent 45% Surge Outrun Its Fundamentals?

- If you are wondering whether DigitalBridge Group is still a smart way to play digital infrastructure, you are not alone. This stock has been catching more eyes lately as investors reassess what fair value really looks like.

- After a sharp 45.4% jump over the last 7 days and a 21.0% gain over the past month, the stock is now up 27.3% year to date. However, its 5 year return of 24.9% still tells a more cautious story.

- Recent attention has centered on DigitalBridge's ongoing pivot toward being a pure play digital infrastructure investor and asset manager, with the market reacting to portfolio reshaping and capital recycling moves. Those strategic shifts have helped reset expectations around both growth potential and risk, which is showing up in the share price momentum.

- Even so, our valuation framework currently gives DigitalBridge Group a value score of 1/6, meaning it screens as undervalued on only one of six checks. Next, we will unpack the different valuation methods behind that number and, by the end, look at a more nuanced way to judge whether the stock really deserves a place in your portfolio.

DigitalBridge Group scores just 1/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: DigitalBridge Group Excess Returns Analysis

The Excess Returns model looks at whether a company can consistently earn more on its shareholders equity than the return investors demand. In other words, it tests if each additional dollar invested in the business creates value or quietly destroys it.

For DigitalBridge Group, the starting point is a Book Value of $6.89 per share and a Stable EPS of $0.59 per share, based on the median return on equity from the past 5 years. Against this, the model applies a Cost of Equity of $0.77 per share, implying an Excess Return of $-0.18 per share. That negative figure suggests the company is not expected to earn enough on its equity base to cover investors required return.

The Average Return on Equity of 6.58% and a projected Stable Book Value of $8.90 per share, derived from weighted future estimates by two analysts, feed into this view. Together, they point to modest profitability that does not justify the current market optimism.

On this basis, the Excess Returns valuation implies the stock is about 156.0% overvalued relative to its intrinsic value.

Result: OVERVALUED

Our Excess Returns analysis suggests DigitalBridge Group may be overvalued by 156.0%. Discover 906 undervalued stocks or create your own screener to find better value opportunities.

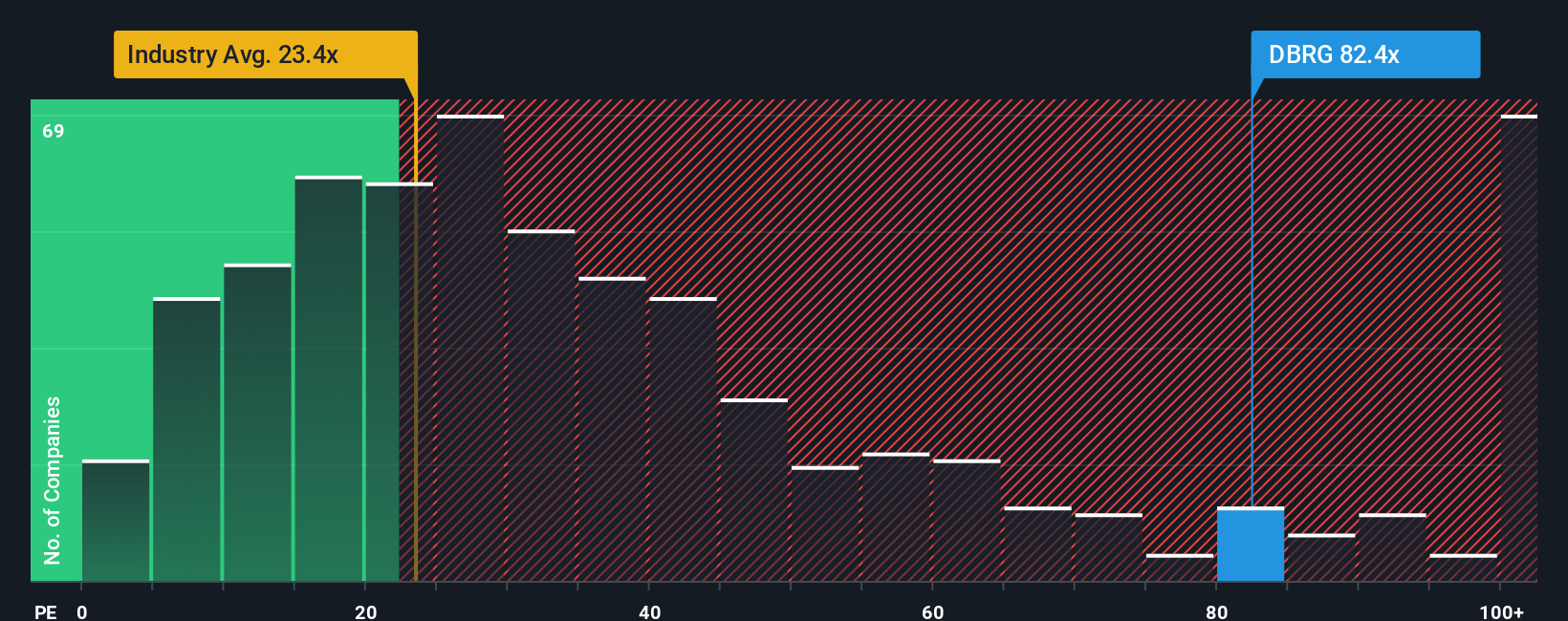

Approach 2: DigitalBridge Group Price vs Earnings

For companies that are generating profits, the price to earnings ratio is a useful way to gauge how much investors are willing to pay today for each dollar of current earnings. It links a familiar bottom line measure, earnings, directly to the share price, so it tends to be intuitive for assessing whether expectations look stretched or reasonable.

What counts as a normal or fair PE ratio depends heavily on how fast earnings are expected to grow and how risky those earnings are. Higher and more reliable growth can justify a richer multiple, while slower or less predictable profits usually command a discount. With that in mind, DigitalBridge currently trades on a steep PE of about 126.5x. This is far above both the Capital Markets industry average of around 24.0x and the peer group average of roughly 13.4x, signaling that the market is baking in very optimistic assumptions.

Simply Wall St’s Fair Ratio framework estimates that, after accounting for DigitalBridge’s earnings growth profile, margins, industry, market cap and company specific risks, a more appropriate PE would be closer to 29.8x. Because this approach adjusts for the factors that actually drive sustainable valuation, it offers a more tailored benchmark than simple industry or peer comparisons. Set against the current 126.5x multiple, the shares still screen as significantly overvalued on this metric.

Result: OVERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1442 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your DigitalBridge Group Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives, a simple way to attach your own story about a company to the numbers behind its fair value, including your assumptions for future revenue, earnings and margins.

A Narrative links three things together in one place: the business story, a financial forecast based on that story, and a resulting fair value estimate that you can compare with today’s share price to help inform a buy, hold, or sell decision.

On Simply Wall St’s Community page, used by millions of investors, Narratives are easy to explore and create, and they automatically update when new information, like earnings releases or major news, changes the outlook.

For DigitalBridge Group, one investor’s Narrative might see AI driven data center demand, rising margins toward 40% and a fair value near $20.0, while a more cautious Narrative might focus on competition, funding risks and regulatory headwinds and land closer to $11.0. This gives you a clear framework to decide which story, and valuation, you find more compelling.

Do you think there's more to the story for DigitalBridge Group? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com