- PREMIUM

- LIVE QUOTES

Index Options

Index Options State Street

State Street CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street JournalIs Sk KakenLtd (TSE:4628) Using Too Much Debt?

Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. As with many other companies Sk Kaken Co.,Ltd. (TSE:4628) makes use of debt. But should shareholders be worried about its use of debt?

What Risk Does Debt Bring?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. The first step when considering a company's debt levels is to consider its cash and debt together.

What Is Sk KakenLtd's Net Debt?

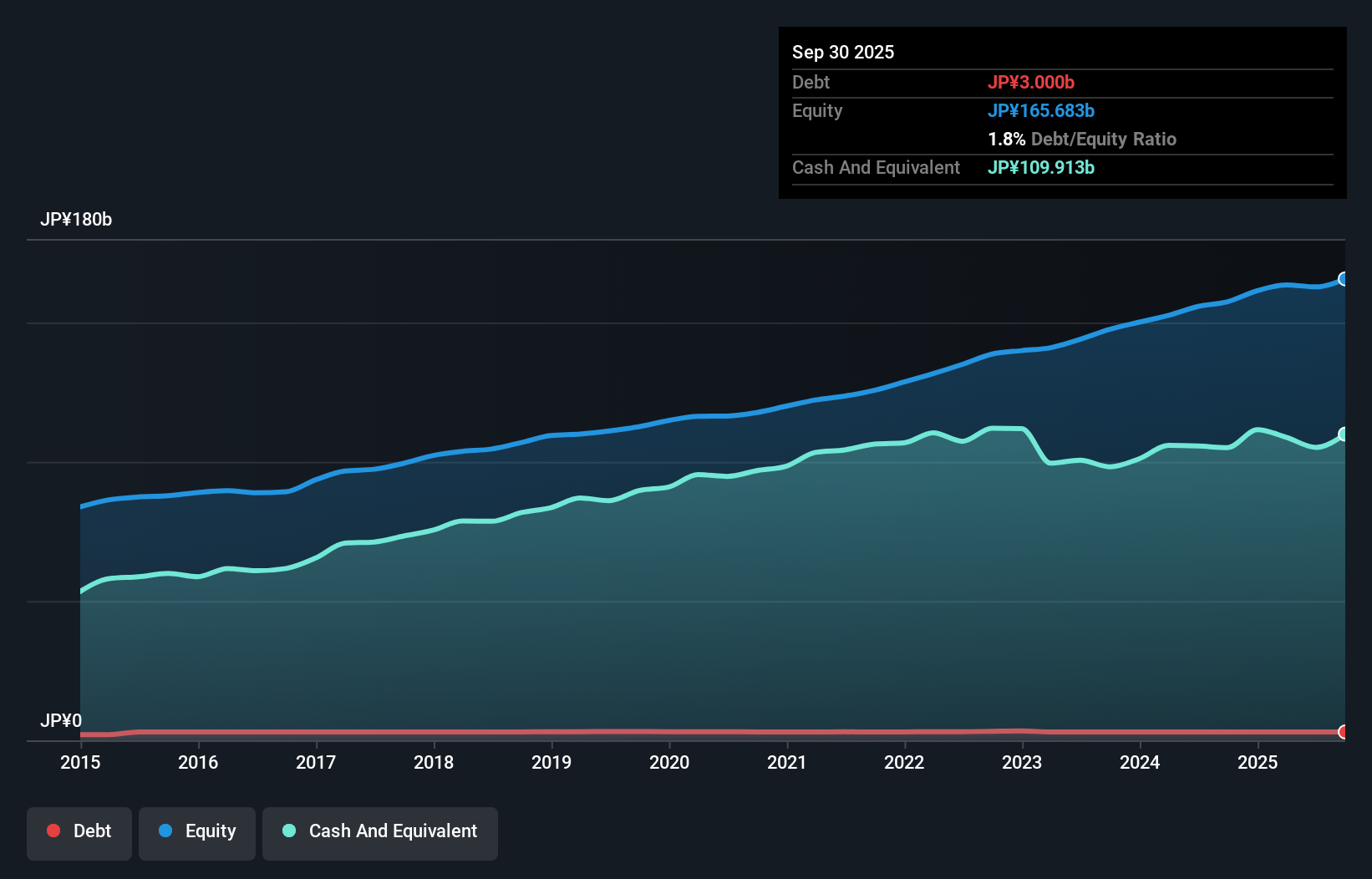

The chart below, which you can click on for greater detail, shows that Sk KakenLtd had JP¥3.00b in debt in September 2025; about the same as the year before. But it also has JP¥109.9b in cash to offset that, meaning it has JP¥106.9b net cash.

How Healthy Is Sk KakenLtd's Balance Sheet?

According to the last reported balance sheet, Sk KakenLtd had liabilities of JP¥23.4b due within 12 months, and liabilities of JP¥4.34b due beyond 12 months. Offsetting these obligations, it had cash of JP¥109.9b as well as receivables valued at JP¥22.8b due within 12 months. So it can boast JP¥104.9b more liquid assets than total liabilities.

This excess liquidity is a great indication that Sk KakenLtd's balance sheet is almost as strong as Fort Knox. On this view, lenders should feel as safe as the beloved of a black-belt karate master. Simply put, the fact that Sk KakenLtd has more cash than debt is arguably a good indication that it can manage its debt safely.

See our latest analysis for Sk KakenLtd

But the other side of the story is that Sk KakenLtd saw its EBIT decline by 4.4% over the last year. That sort of decline, if sustained, will obviously make debt harder to handle. There's no doubt that we learn most about debt from the balance sheet. But you can't view debt in total isolation; since Sk KakenLtd will need earnings to service that debt. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. While Sk KakenLtd has net cash on its balance sheet, it's still worth taking a look at its ability to convert earnings before interest and tax (EBIT) to free cash flow, to help us understand how quickly it is building (or eroding) that cash balance. During the last three years, Sk KakenLtd produced sturdy free cash flow equating to 63% of its EBIT, about what we'd expect. This cold hard cash means it can reduce its debt when it wants to.

Summing Up

While it is always sensible to investigate a company's debt, in this case Sk KakenLtd has JP¥106.9b in net cash and a decent-looking balance sheet. So we don't think Sk KakenLtd's use of debt is risky. Above most other metrics, we think its important to track how fast earnings per share is growing, if at all. If you've also come to that realization, you're in luck, because today you can view this interactive graph of Sk KakenLtd's earnings per share history for free.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.