- PREMIUM

- LIVE QUOTES

- INSTITUTION

Index Options

Index Options State Street

State Street CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street JournalIs Akamai Technologies a Hidden Opportunity After Its Recent 22.2% Share Price Jump?

- If you are wondering whether Akamai Technologies is quietly turning into a value opportunity while many investors focus on flashier tech names, you are not alone.

- The stock has climbed 22.2% over the last month even though it is still down 7.8% year to date and 9.7% over the past year. This combination often signals shifting market expectations rather than a simple momentum story.

- Recent attention has centered on Akamai's evolution from a content delivery network provider into a broader cloud security and edge computing platform. Many investors increasingly see this shift as key to its long term relevance. At the same time, moves to deepen its security offerings and expand edge capabilities have sparked debate about whether the market is fully appreciating the durability of its cash flows.

- On our numbers, Akamai scores a solid 5/6 valuation checks, suggesting it screens as undervalued on most, but not all, of the usual metrics. In the sections that follow we will walk through those methods, then explore an even more powerful way to make sense of what the valuation is really telling you.

Find out why Akamai Technologies's -9.7% return over the last year is lagging behind its peers.

Approach 1: Akamai Technologies Discounted Cash Flow (DCF) Analysis

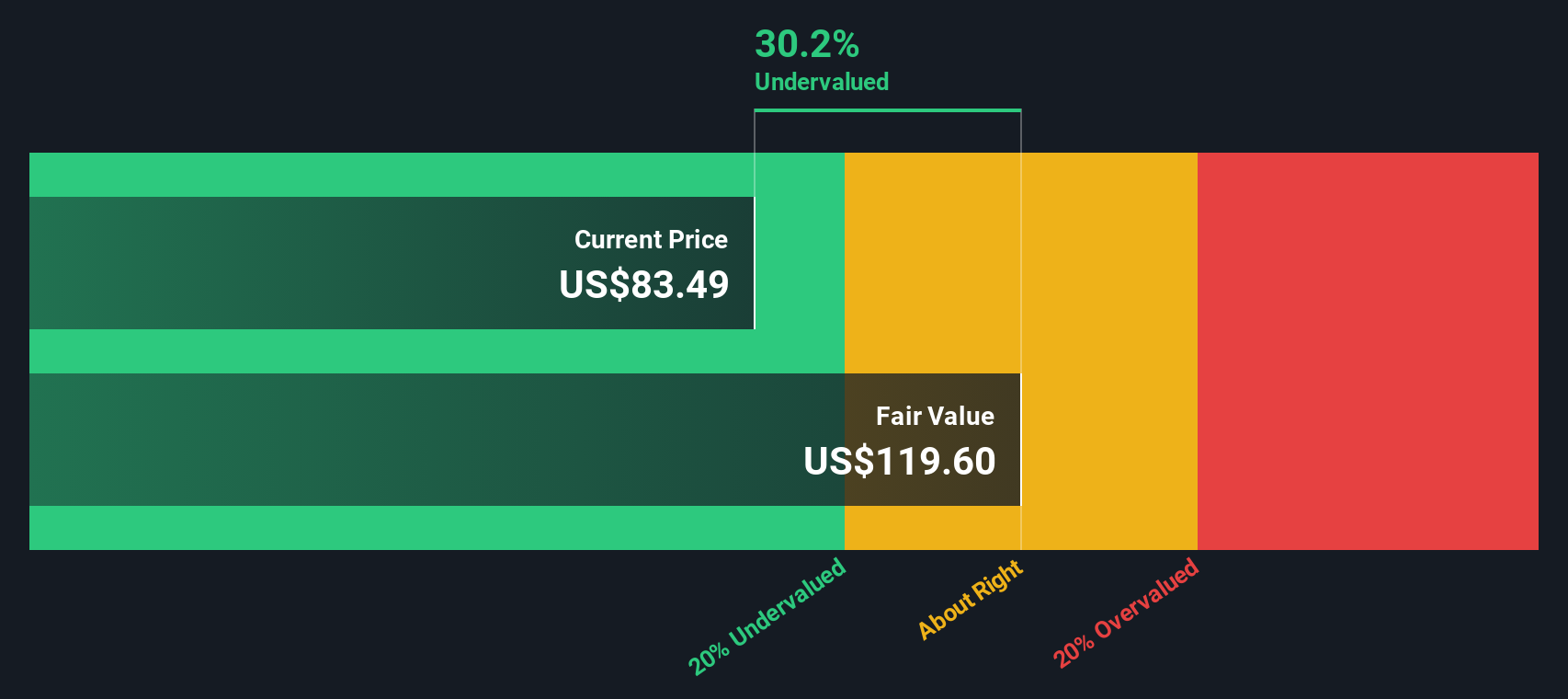

A Discounted Cash Flow, or DCF, model estimates what a company is worth by projecting the cash it can generate in the future and then discounting those cash flows back to today in dollar terms. For Akamai Technologies, the 2 Stage Free Cash Flow to Equity model starts with last twelve month free cash flow of about $649.8 million and then layers on growth assumptions.

Analysts explicitly model out several years, with free cash flow expected to reach about $1.04 billion by 2027. Beyond that point, Simply Wall St extrapolates further, with projections climbing to roughly $1.72 billion by 2035 as growth gradually moderates over time. All of these future figures are discounted back to arrive at an intrinsic value estimate of $120.50 per share in dollar terms.

Compared with the current share price, this implies roughly a 27.0% discount, suggesting Akamai trades materially below its modeled long term cash generation potential.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Akamai Technologies is undervalued by 27.0%. Track this in your watchlist or portfolio, or discover 914 more undervalued stocks based on cash flows.

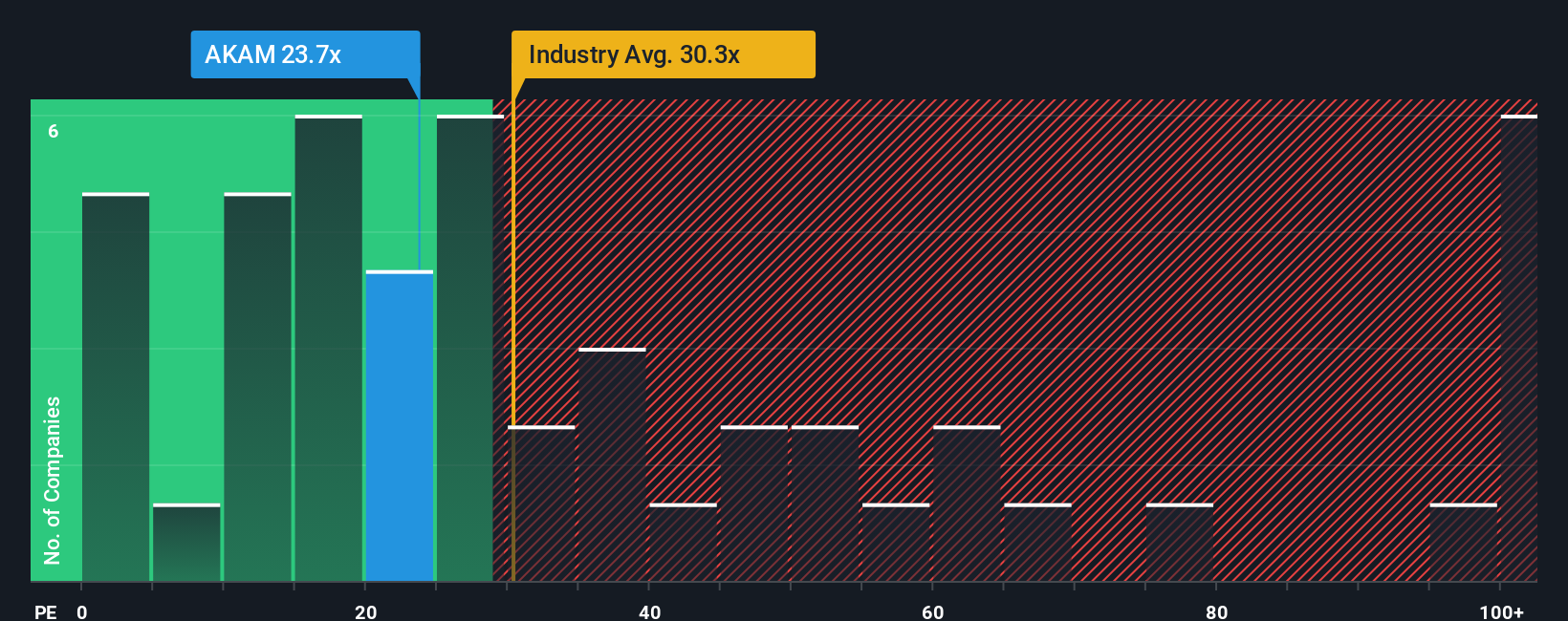

Approach 2: Akamai Technologies Price vs Earnings

For a consistently profitable company like Akamai Technologies, the price to earnings, or PE, ratio is a practical way to gauge how much investors are willing to pay for each dollar of earnings. In general, faster growing and lower risk businesses deserve higher PE multiples, while slower or riskier names should trade on lower ones.

Akamai currently trades on a PE of about 25.0x. That sits below both the broader IT industry average of roughly 29.7x and the peer group average near 42.2x, implying the market is applying a discount to Akamai relative to many comparable stocks. To move beyond simple comparisons, Simply Wall St uses a proprietary “Fair Ratio” of 31.7x, which estimates the multiple Akamai should trade on after factoring in its earnings growth outlook, margins, risk profile, industry and market cap.

This Fair Ratio is more informative than raw peer or industry benchmarks because it adjusts for company specific fundamentals rather than assuming all tech names deserve the same multiple. Comparing Akamai’s current 25.0x PE to the Fair Ratio of 31.7x suggests the shares are trading below what its fundamentals would typically justify.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1442 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Akamai Technologies Narrative

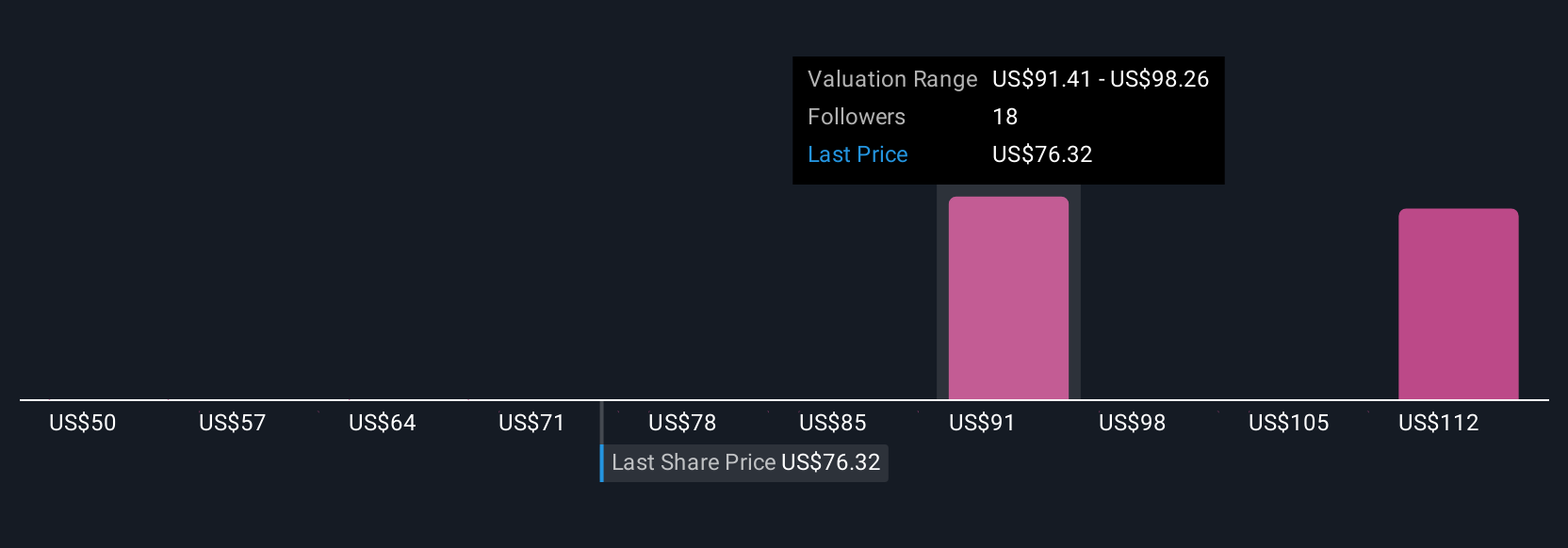

Earlier we mentioned that there is an even better way to understand valuation. On Simply Wall St's Community page you can use Narratives, simple story driven forecasts that let you spell out your view on a company, translate that story into assumptions for future revenue, earnings and margins, and then see the Fair Value that drops out so you can compare it to today’s price. You can track when the gap suggests it might be time to buy or sell, and watch that view update dynamically as new earnings or news arrives. One Akamai Narrative might lean bullish with a Fair Value near the top of analysts’ range around $133.0, based on strong AI, security and edge growth. Another more cautious Narrative could anchor closer to $66.0, reflecting concerns about CDN decline, execution risk and competition. This gives you a clear, easy to use framework to decide which story, and which price, you actually believe.

Do you think there's more to the story for Akamai Technologies? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com