- PREMIUM

- LIVE QUOTES

- INSTITUTION

Index Options

Index Options State Street

State Street CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street JournalUranium Energy (UEC) Valuation Check After Strong Long-Term Returns and Recent Share Price Volatility

Uranium Energy (UEC) has been quietly riding uranium’s renewed spotlight, with the stock up sharply this year as investors reassess long term nuclear demand, its growth pipeline, and lingering profitability questions.

See our latest analysis for Uranium Energy.

That surge to a recent share price of $12.95 comes after a choppy stretch, with a negative 1 month share price return but a strong year to date share price gain and powerful 5 year total shareholder return that suggest long term momentum is still intact.

If UEC’s run has you thinking about where the next long term winners might come from, this could be a smart moment to explore fast growing stocks with high insider ownership.

With the shares still trading below the average analyst price target, but profitability yet to follow surging revenues, investors face a key question: Is Uranium Energy undervalued today, or has the market already priced in its future growth?

Price to Book of 6.4x: Is it justified?

Uranium Energy trades at a rich price to book ratio of 6.4 times, a clear premium to both its peers and the broader US Oil and Gas industry.

Price to book compares a company’s market value with the net assets on its balance sheet. It is a common yardstick for asset heavy resource businesses where reserves, plants, and equipment dominate.

For UEC, paying such a steep multiple means investors are already baking in ambitious expectations that future uranium production, revenue growth, and eventual profitability will materially lift returns on equity from today’s negative levels.

The contrast is stark. UEC’s 6.4 times price to book towers over the peer average of 4.3 times and the US Oil and Gas industry’s 1.4 times benchmark, underscoring how much more investors are willing to pay for each dollar of its net assets.

See what the numbers say about this price — find out in our valuation breakdown.

Result: Price to Book of 6.4x (OVERVALUED)

However, stubborn losses and execution risk around scaling profitable production could quickly challenge today’s rich valuation and investors’ optimistic uranium demand assumptions.

Find out about the key risks to this Uranium Energy narrative.

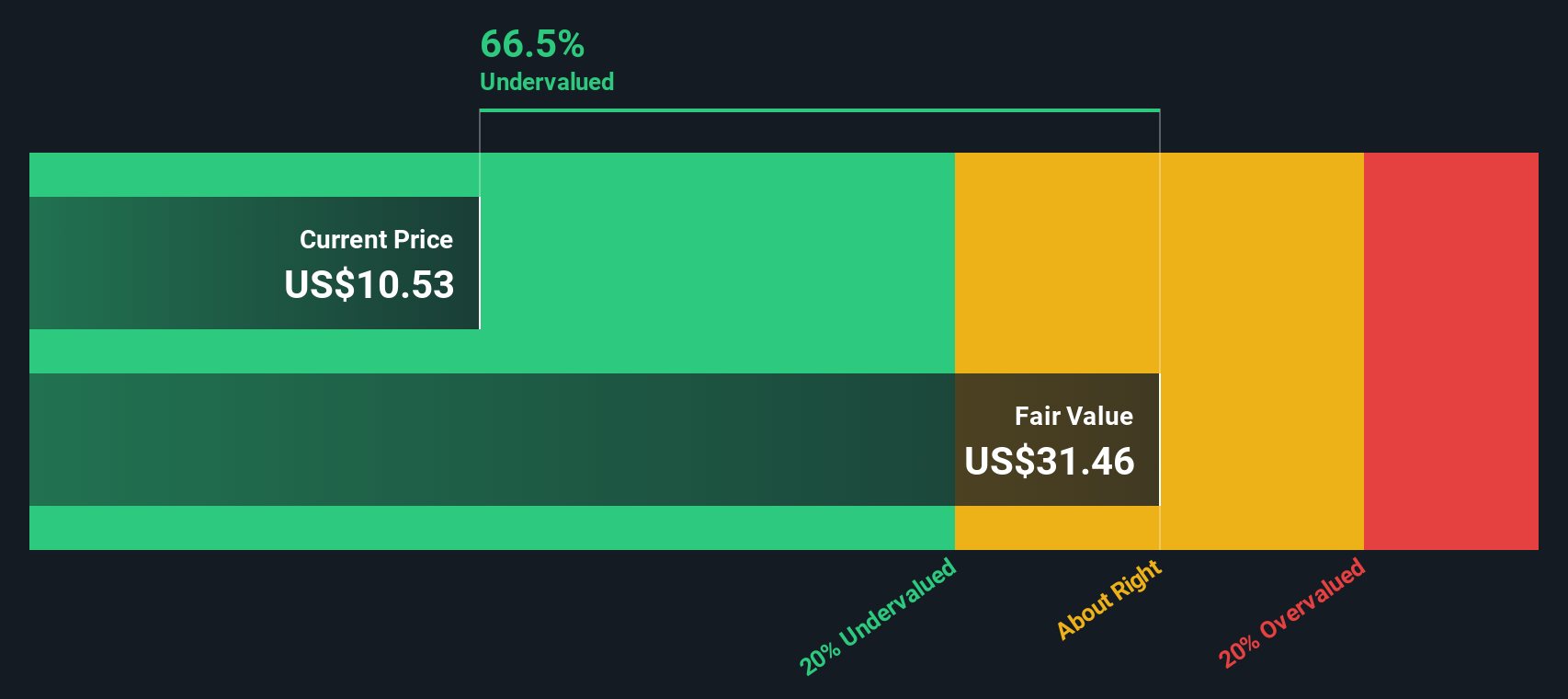

Another View, Fair Value Looks More Supportive

Our DCF model tells a softer story than the rich 6.4 times book value. On this view, UEC trades about 4.5% below its estimated fair value, suggesting the current price might slightly underestimate long term cash flows rather than fully overhype them.

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Uranium Energy for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 917 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Uranium Energy Narrative

If you see the story differently and want to dig into the numbers yourself, you can build a custom view in just minutes using Do it your way.

A great starting point for your Uranium Energy research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

Ready for more high conviction ideas?

Do not stop at one opportunity. Let the Simply Wall St Screener show you fresh, data backed ideas that could reshape your portfolio’s long term returns.

- Target future growth engines by scanning these 25 AI penny stocks that are using artificial intelligence to transform industries and capture powerful, compounding revenue streams.

- Lock in potential cash flow and stability by reviewing these 14 dividend stocks with yields > 3% that can strengthen your income base while markets stay unpredictable.

- Seize mispriced opportunities before the crowd by tracking these 917 undervalued stocks based on cash flows that our models flag as trading below their estimated intrinsic worth.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com