- PREMIUM

- LIVE QUOTES

- INSTITUTION

Index Options

Index Options State Street

State Street CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street JournalHas Google’s AI Momentum Already Been Priced In After Its 84% One Year Surge?

- If you are wondering whether Alphabet is still a smart buy after its massive run, or if the big gains are already behind it, you are not alone. That is exactly what this breakdown is here to explore.

- Despite a small 7 day dip of 0.1%, Alphabet is still up 12.7% over the last month, 68.7% year to date and 84.1% over the past year, which naturally raises the question of how much upside is really left.

- Recent moves have been driven by ongoing excitement around Alphabet's AI efforts, from integrating generative tools into Search and Workspace to expanding its cloud based AI services for enterprise customers. At the same time, investors are reacting to regulatory headlines around antitrust cases and privacy rules, which can shift sentiment quickly even when the core business remains strong.

- Right now, Alphabet scores a 2/6 valuation score, suggesting it looks undervalued on only a couple of our checks. Next, we will unpack how different valuation methods view the stock, and then finish with a more holistic way to judge whether the current price really makes sense.

Alphabet scores just 2/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: Alphabet Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model estimates what a business is worth today by taking its expected future cash flows and discounting them back to a present value. For Alphabet, this means projecting how much cash the company can return to shareholders over time, and then working out what that stream of cash is worth in $ today.

Alphabet generated roughly $92.6 billion in free cash flow over the last twelve months. Analysts and internal estimates expect this to rise steadily, with projections reaching about $257.8 billion by 2035. The first several years of cash flows are based on analyst forecasts, and the later years are extrapolated using Simply Wall St growth assumptions within a 2 stage Free Cash Flow to Equity framework.

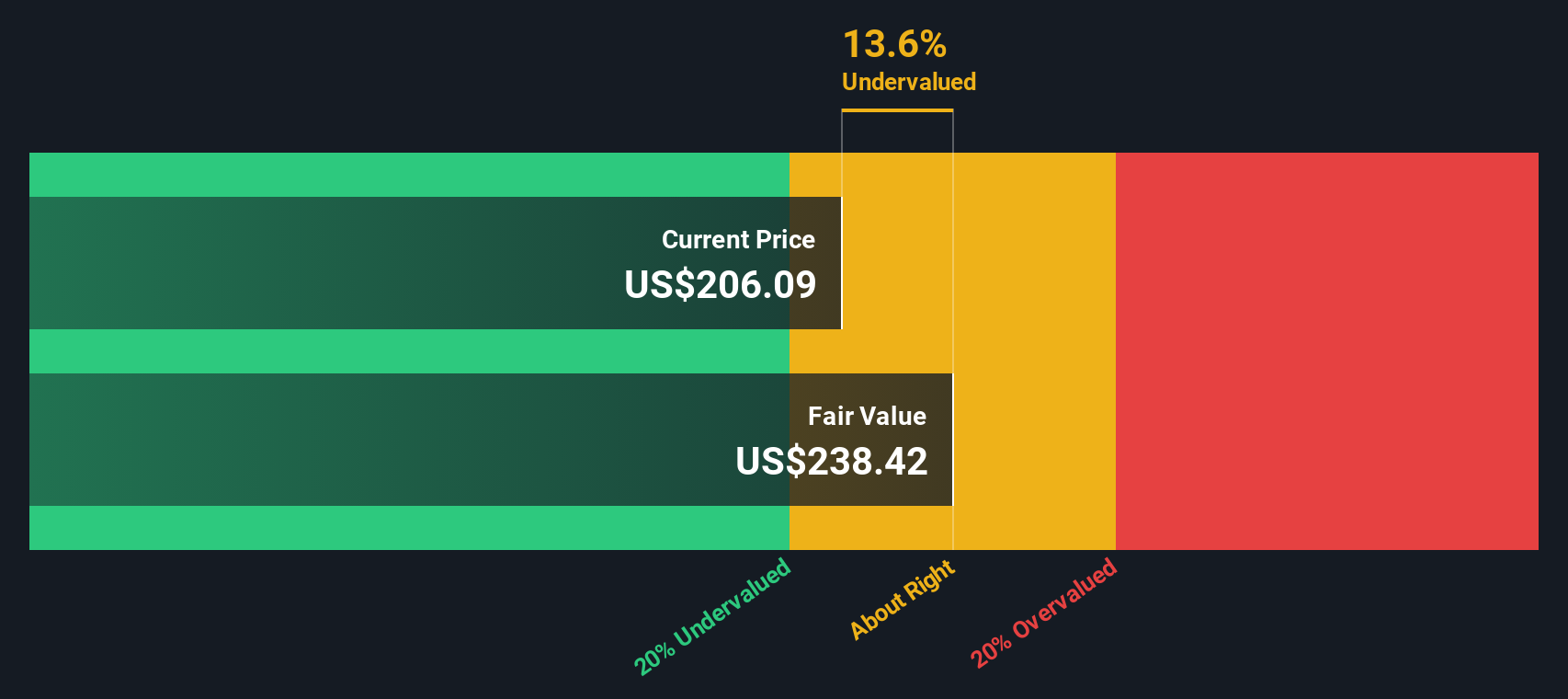

On this basis, the DCF model arrives at an intrinsic value of around $289.53 per share. Compared with the current market price, this implies Alphabet is trading about 10.4% above its estimated fair value. This suggests the stock screens as modestly overvalued on cash flow fundamentals.

Result: OVERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Alphabet may be overvalued by 10.4%. Discover 920 undervalued stocks or create your own screener to find better value opportunities.

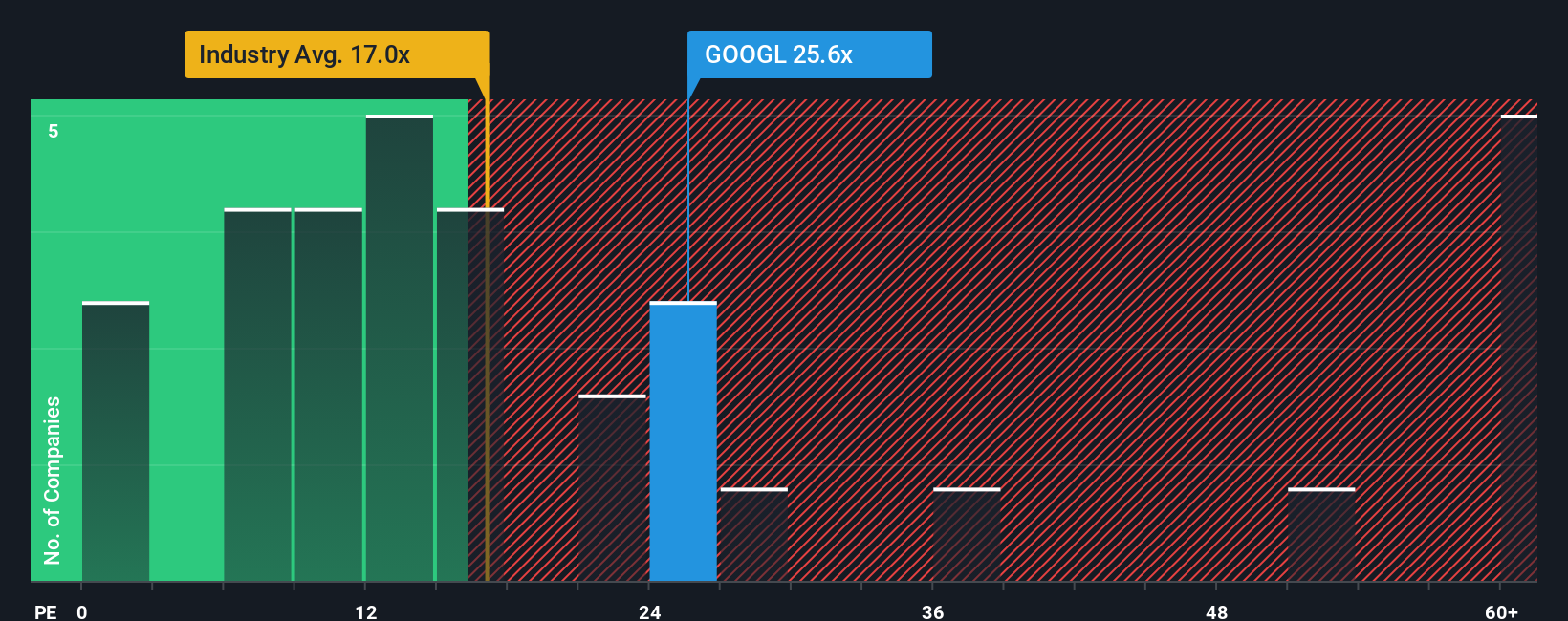

Approach 2: Alphabet Price vs Earnings

For profitable businesses like Alphabet, the price to earnings, or PE, ratio is a natural way to gauge valuation because it ties the share price directly to the profits the company is generating today. In general, higher growth and lower risk justify a higher PE, while slower growth or higher uncertainty should come with a lower, more conservative multiple.

Alphabet currently trades on a PE of about 31.0x. That is well above the broader Interactive Media and Services industry average of roughly 16.4x, but below the peer group average of around 47.6x, suggesting investors see Alphabet as higher quality than the typical company in its space, but not the most aggressively priced name in the group.

Simply Wall St’s Fair Ratio for Alphabet is 37.3x, a proprietary estimate of what PE the stock deserves given its earnings growth outlook, margins, risk profile, industry, and market cap. Because this measure is tailored to Alphabet’s fundamentals and risk rather than just simple comparisons, it offers a more nuanced benchmark than industry or peer averages. With the current 31.0x multiple sitting below the 37.3x Fair Ratio, the stock appears modestly undervalued on an earnings basis.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1439 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Alphabet Narrative

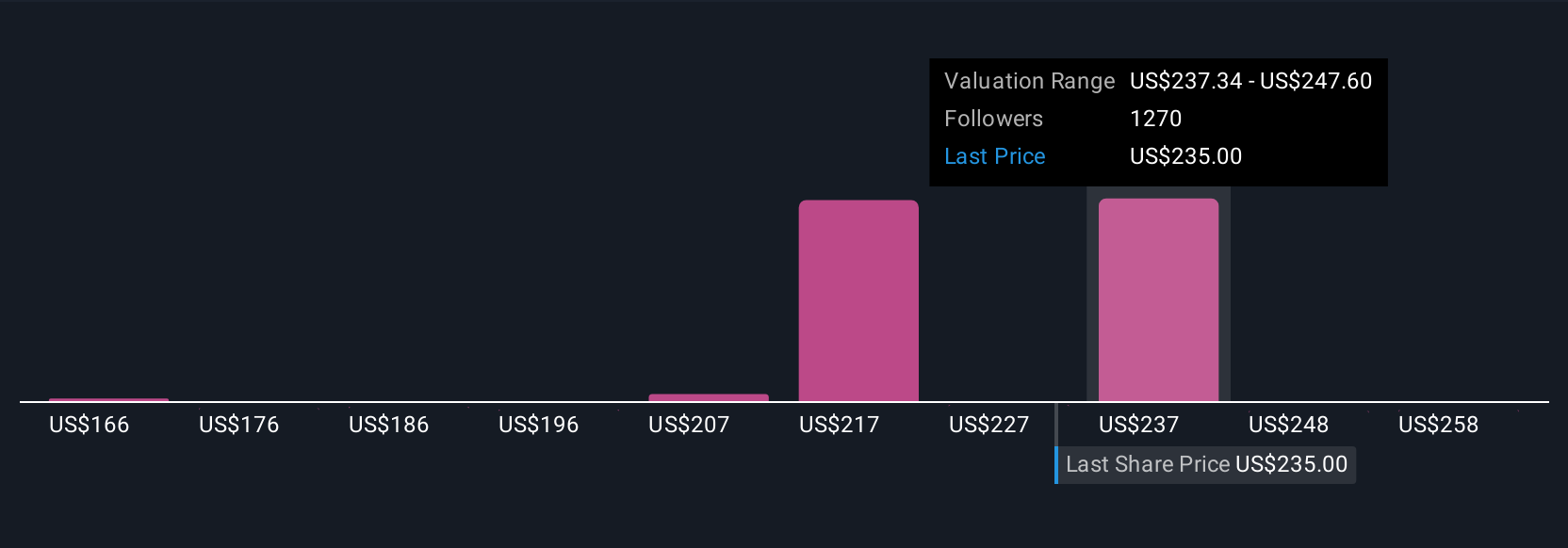

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives, a simple but powerful way to connect your view of Alphabet’s future to numbers by writing the story you believe about its growth drivers, margins and risks, linking that story to a financial forecast and fair value, and then comparing that Fair Value to today’s Price to decide whether to buy, hold or sell. On Simply Wall St’s Community page, millions of investors use Narratives as an accessible tool where their assumptions, like revenue growth rates and profit margins, are turned into dynamic valuations that automatically update as new information such as earnings, AI product launches or regulatory news comes in. For Alphabet, one investor might build a Narrative that assumes moderate 10 percent annual revenue growth, 30 percent long term profit margins and a fair value around 171 dollars, while another may expect faster 17 percent growth, a slightly higher margin profile and arrive at a fair value closer to 340 dollars, and Narratives makes those different perspectives transparent, structured and directly comparable.

For Alphabet however we'll make it really easy for you with previews of two leading Alphabet Narratives:

Fair value: $340.00

Implied undervaluation: -6.4%

Revenue growth assumption: 17.36%

- Sees Alphabet as a cash generative giant, combining dominant digital ads, a now profitable Google Cloud and deep AI expertise from DeepMind and Gemini.

- Highlights a fortress balance sheet, powerful optionality from assets like YouTube, Android and Waymo, and growing buybacks to amplify long term returns.

- Argues that Berkshire’s stake could trigger a higher future P/E multiple as markets increasingly treat Alphabet as a quality compounder rather than just an ad business.

Fair value: $212.34

Implied overvaluation: 50.5%

Revenue growth assumption: 13.47%

- Expects digital advertising and cloud trends to stay supportive, but not explosive, keeping Alphabet on a steadier, more mature growth path.

- Views generative AI as sustaining rather than disruptive, but notes that high compute costs and regulation could cap near term profitability and adoption.

- Builds a thesis on slower but durable growth, rising margins from cost cutting and cloud scale, and a future P/E around 30x that is below today’s market price.

Do you think there's more to the story for Alphabet? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com