- PREMIUM

- LIVE QUOTES

Index Options

Index Options State Street

State Street CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street JournalWill Medicare’s 2026 Rule Shift and Amedisys Integration Strengthen Pennant Group’s (PNTG) Narrative?

- Earlier this week, Truist Securities upgraded The Pennant Group to a buy rating, highlighting solid operating trends, strong sector demand, and reduced reimbursement risk following a less restrictive 2026 Medicare home health rule.

- Analysts also pointed to Pennant’s smooth integration of 54 acquired Amedisys locations as a key factor supporting its operational and earnings outlook.

- With that backdrop, we’ll now explore how the favorable 2026 Medicare rule update may affect Pennant’s broader investment narrative.

Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 36 best rare earth metal stocks of the very few that mine this essential strategic resource.

Pennant Group Investment Narrative Recap

To own Pennant Group, you generally need to believe in long term demand for home health and senior living, and in Pennant’s ability to scale efficiently through acquisitions. The recent Truist upgrade and less restrictive 2026 Medicare home health rule directly soften one of the biggest near term risks from reimbursement cuts, while integration and labor costs remain key swing factors for results over the next few years.

Among recent updates, Pennant’s Q3 2025 results and reiterated full year 2025 revenue guidance of US$911.4 million to US$948.6 million stand out alongside the Medicare rule news. Together, they frame a story where growth from acquisitions, including the Amedisys locations, is showing up in reported numbers, but investors still need to watch how higher debt capacity and margin pressures interact with evolving reimbursement rules.

However, investors should also be aware that Pennant’s heavy reliance on government payers means future policy shifts could...

Read the full narrative on Pennant Group (it's free!)

Pennant Group's narrative projects $1.2 billion revenue and $59.3 million earnings by 2028. This requires 13.6% yearly revenue growth and a roughly $32.5 million earnings increase from $26.8 million today.

Uncover how Pennant Group's forecasts yield a $33.60 fair value, a 15% upside to its current price.

Exploring Other Perspectives

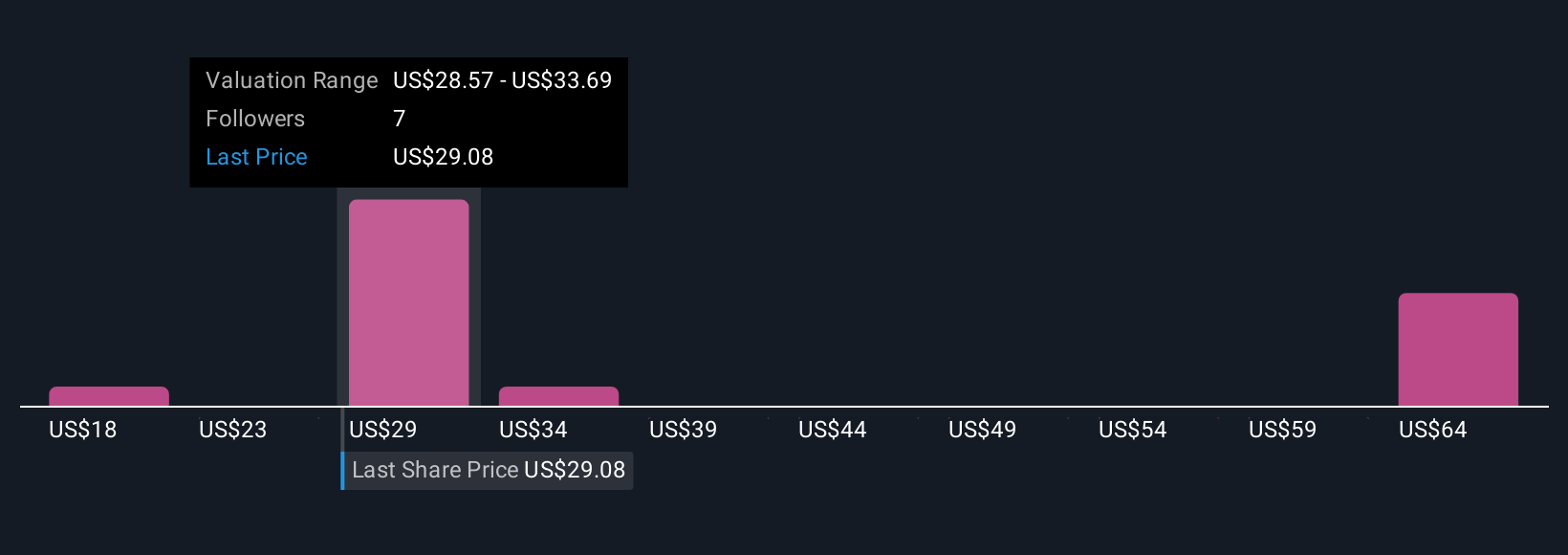

Five members of the Simply Wall St Community currently estimate Pennant’s fair value between US$18.33 and US$69.53, reflecting very different expectations. Against that backdrop, the eased 2026 Medicare rule helps some concerns, but reimbursement dependence and integration execution still shape how Pennant’s performance could unfold, so it is worth comparing several viewpoints before deciding what the stock is worth.

Explore 5 other fair value estimates on Pennant Group - why the stock might be worth over 2x more than the current price!

Build Your Own Pennant Group Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Pennant Group research is our analysis highlighting 3 key rewards that could impact your investment decision.

- Our free Pennant Group research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Pennant Group's overall financial health at a glance.

Contemplating Other Strategies?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- These 12 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- AI is about to change healthcare. These 30 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Trump has pledged to "unleash" American oil and gas and these 22 US stocks have developments that are poised to benefit.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com