Is It Too Late To Consider ASML After Its 58.3% Surge In 2025?

- Wondering if ASML Holding is still worth buying after its huge run, or if the easy money has already been made? This article will walk through what the current price is really baking in.

- The stock has climbed about 6.5% over the last week, 3.9% over the past month, and is up a hefty 58.3% year to date. This naturally raises questions about how much upside is left versus the risk of a pullback.

- Recent moves have come as investors double down on the long term demand story for advanced lithography tools and ASML's crucial role in enabling cutting edge chips. The stock has also been in focus amid ongoing discussions about export controls and supply chain resilience for semiconductor equipment makers, which adds both excitement and uncertainty to the outlook.

- Despite that, our valuation checks suggest ASML scores just 1/6 on undervaluation. We will break down what different valuation approaches say about the current price, and then finish with a more nuanced way to think about ASML's true worth beyond the usual multiples and models.

ASML Holding scores just 1/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: ASML Holding Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow model estimates what a business is worth today by projecting the cash it can generate in the future and then discounting those cash flows back to the present.

For ASML Holding, the model starts with last twelve months free cash flow of about €8.6 billion and uses analyst estimates for the next few years, then extrapolates further out. By 2029, free cash flow is projected to reach roughly €17.3 billion, with longer term estimates continuing to rise as ASML benefits from demand for advanced lithography tools. These figures are all converted into today’s money using a required rate of return and then summed to get a total equity value.

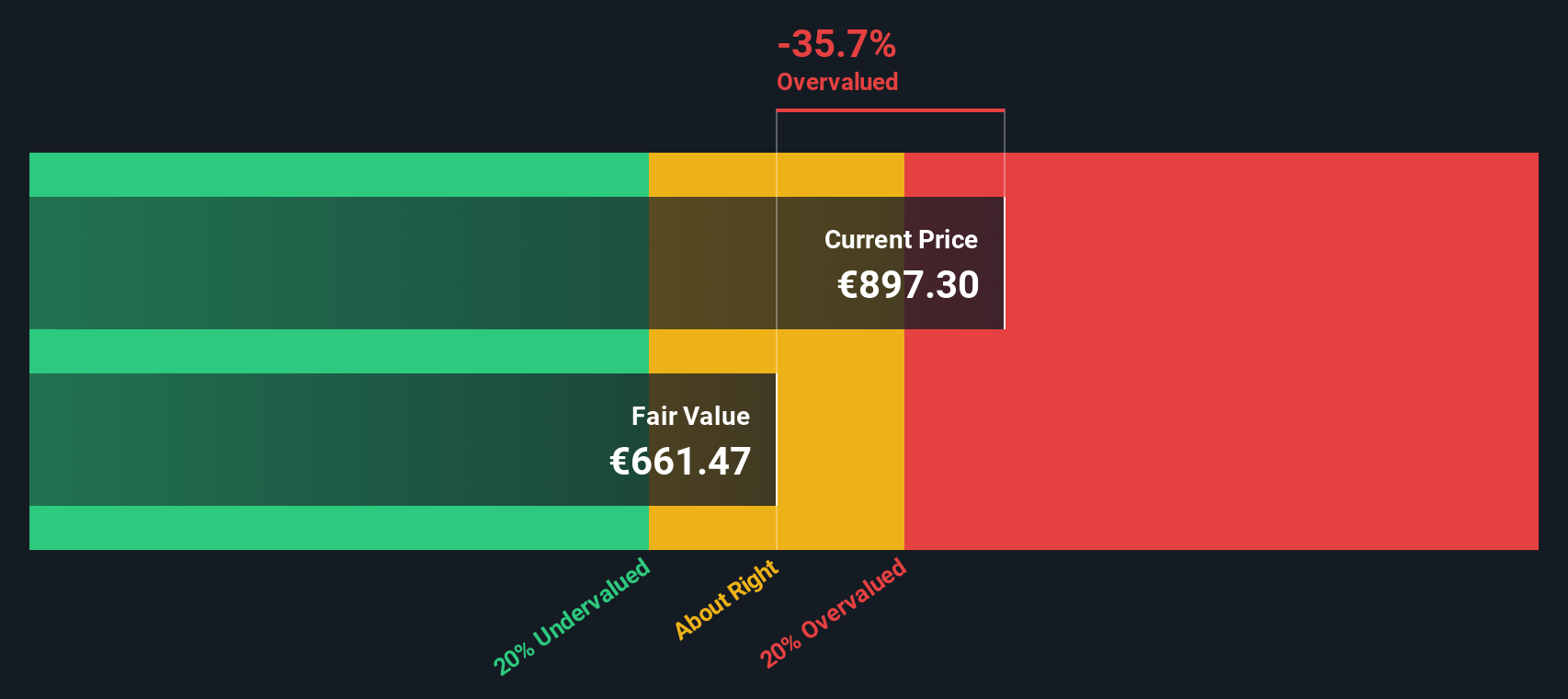

On this basis, the DCF points to an intrinsic value of about $779.56 per share, which implies the stock is roughly 42.2% above where the cash flow outlook would justify.

Result: OVERVALUED

Our Discounted Cash Flow (DCF) analysis suggests ASML Holding may be overvalued by 42.2%. Discover 927 undervalued stocks or create your own screener to find better value opportunities.

Approach 2: ASML Holding Price vs Earnings

For a profitable, relatively mature business like ASML, the price to earnings (PE) ratio is a useful shorthand for how much investors are willing to pay for each dollar of current earnings. In general, faster growth and lower perceived risk justify a higher PE, while slower growth or higher uncertainty should pull a “normal” or “fair” PE lower.

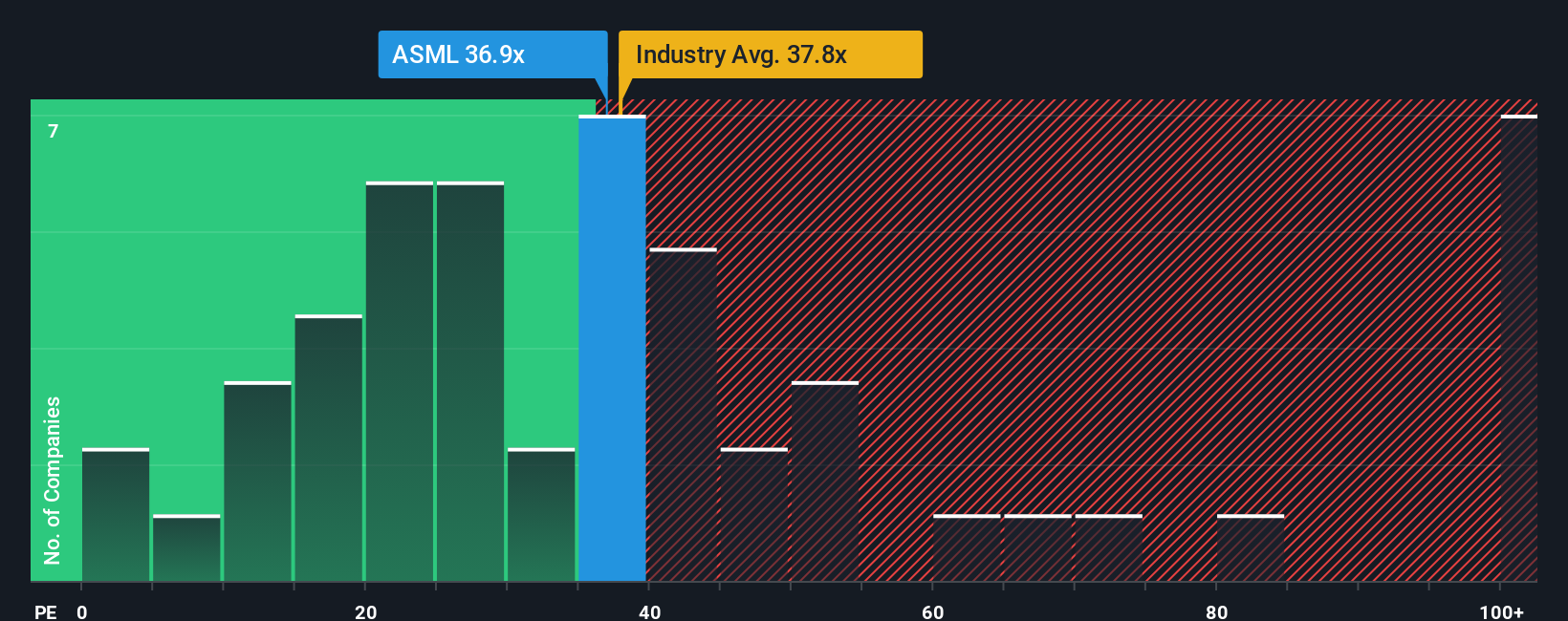

ASML currently trades at about 38.4x earnings, which is above the broader Semiconductor industry average of roughly 36.2x, but below the 42.1x PE seen across close peers. To move beyond simple comparisons, Simply Wall St calculates a proprietary “Fair Ratio” of 30.9x. This figure reflects what ASML’s PE might reasonably be given its earnings growth outlook, profitability, size, industry dynamics and risk profile.

This Fair Ratio is more informative than raw peer or industry averages because it adjusts for ASML’s specific strengths and risk factors rather than assuming all chip equipment makers deserve the same multiple. Comparing the current 38.4x PE with the 30.9x Fair Ratio suggests the market is pricing in a premium above what those fundamentals would support, pointing to a stock that looks expensive on this metric.

Result: OVERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1440 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your ASML Holding Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives, a simple way to connect the story you believe about a company with the numbers behind its fair value.

A Narrative is your own structured view of a business, where you spell out how you think revenue, earnings and margins will evolve, then link that story directly to a financial forecast and a resulting fair value.

On Simply Wall St’s Community page, investors use Narratives as an easy, accessible tool to turn their perspective on a company into a living valuation that updates dynamically whenever new information, such as earnings or major news, comes in.

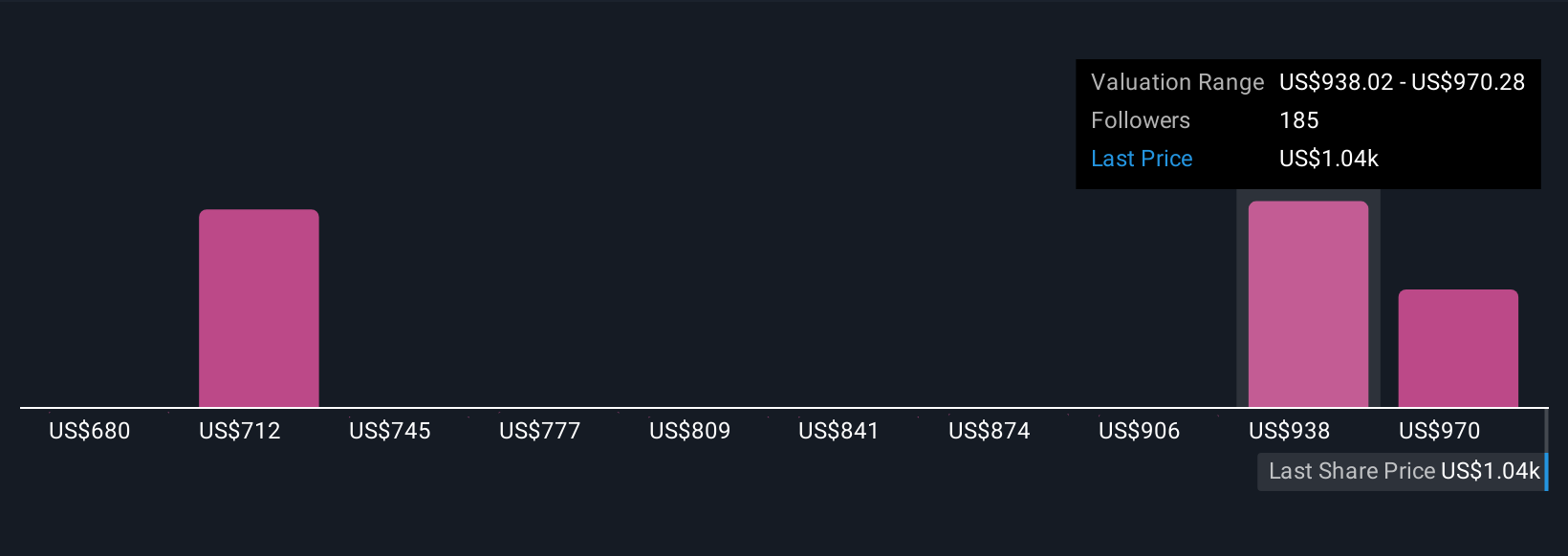

Because each Narrative produces a Fair Value, you can quickly compare that to the current share price to decide how ASML might fit into a buy, hold or sell framework. You can also see how other investors might reach very different conclusions, with some viewing ASML as worth around $1,002 per share while others see value closer to $650.

Do you think there's more to the story for ASML Holding? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com