- PREMIUM

- LIVE QUOTES

Index Options

Index Options State Street

State Street CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street JournalExploring Middle East's Hidden Gems With 3 Promising Stocks

In recent times, Middle East stock markets have experienced a subdued atmosphere, primarily influenced by weak oil prices and anticipation of key U.S. economic data that could signal shifts in Federal Reserve interest rates. Despite these challenges, the region remains fertile ground for identifying promising stocks, as investors seek companies with strong fundamentals and resilience to navigate the current economic landscape.

Top 10 Undiscovered Gems With Strong Fundamentals In The Middle East

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Mendelson Infrastructures & Industries | 17.65% | 4.48% | 4.46% | ★★★★★★ |

| Qassim Cement | NA | 4.02% | -11.40% | ★★★★★★ |

| MOBI Industry | 18.09% | 6.66% | 22.02% | ★★★★★★ |

| Y.D. More Investments | 51.67% | 27.49% | 36.12% | ★★★★★★ |

| Baazeem Trading | 10.02% | -1.27% | -1.66% | ★★★★★★ |

| Sure Global Tech | NA | 10.11% | 15.42% | ★★★★★★ |

| Nofoth Food Products | NA | 15.49% | 26.47% | ★★★★★★ |

| Gür-Sel Turizm Tasimacilik ve Servis Ticaret | 4.69% | 36.04% | 53.41% | ★★★★★☆ |

| Bosch Fren Sistemleri Sanayi ve Ticaret | 36.11% | 41.59% | 7.72% | ★★★★☆☆ |

| Marmaris Altinyunus Turistik Tesisler | NA | 47.16% | -34.78% | ★★★★☆☆ |

Let's review some notable picks from our screened stocks.

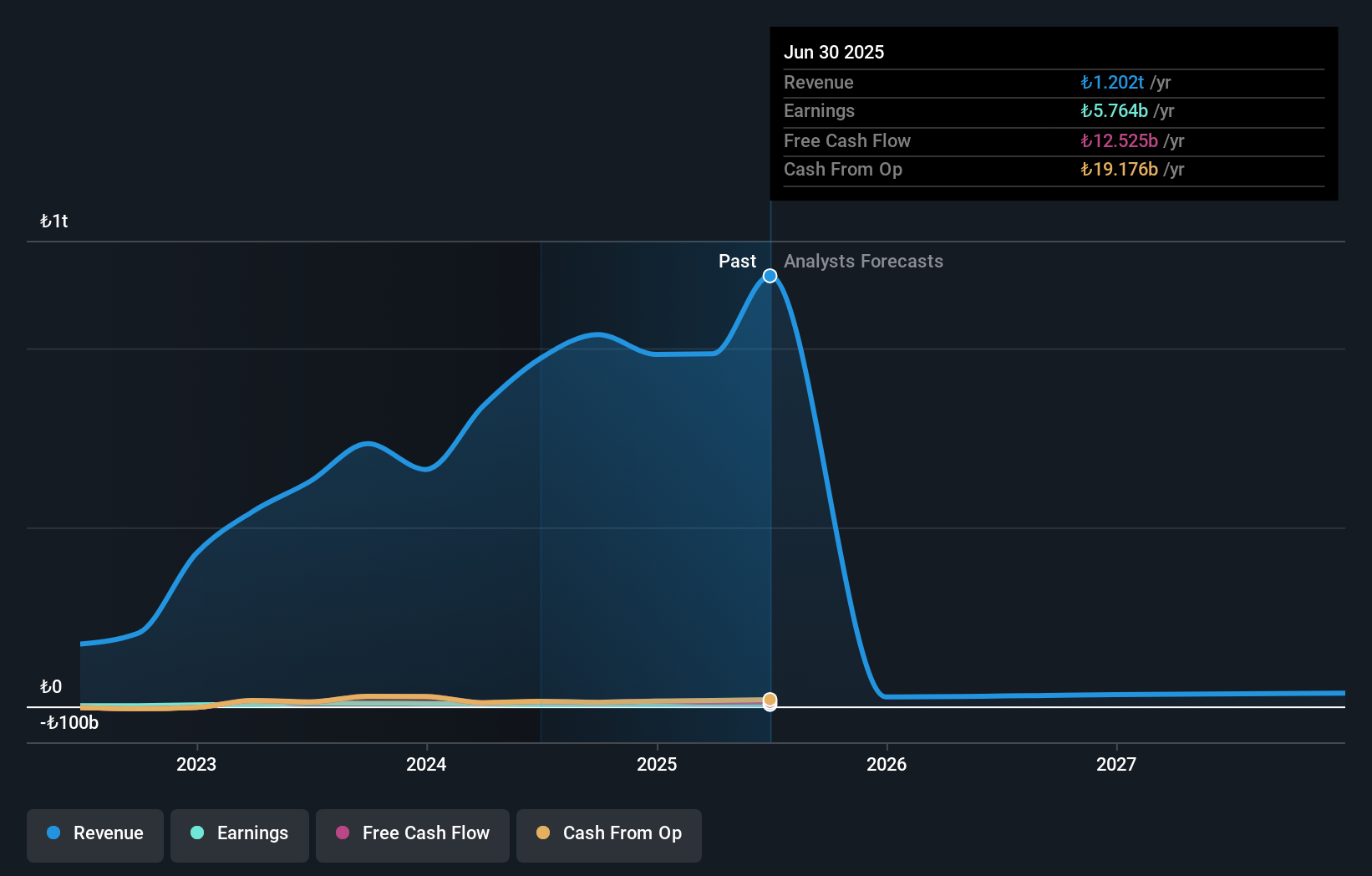

Is Yatirim Menkul Degerler Anonim Sirketi (IBSE:ISMEN)

Simply Wall St Value Rating: ★★★★★☆

Overview: Is Yatirim Menkul Degerler Anonim Sirketi offers capital market services to both individual and corporate investors in Turkey and abroad, with a market capitalization of TRY62.25 billion.

Operations: The company's revenue primarily comes from venture capital, which generated TRY17.68 billion, followed by portfolio management at TRY2.91 billion and investment partnership at TRY0.89 billion.

Is Yatirim Menkul Degerler Anonim Sirketi, a vibrant player in the capital markets, has seen its debt to equity ratio improve significantly from 41.5% to 21.3% over five years, indicating prudent financial management. Despite a challenging year with earnings growth at -15.9%, the company boasts high-quality past earnings and maintains a competitive price-to-earnings ratio of 11.3x against the TR market's 17.8x. Recent reports show third-quarter net income at TRY 1,514 million, slightly down from TRY 1,768 million last year; however, nine-month figures remain stable at TRY 4,800 million compared to TRY 4,777 million previously.

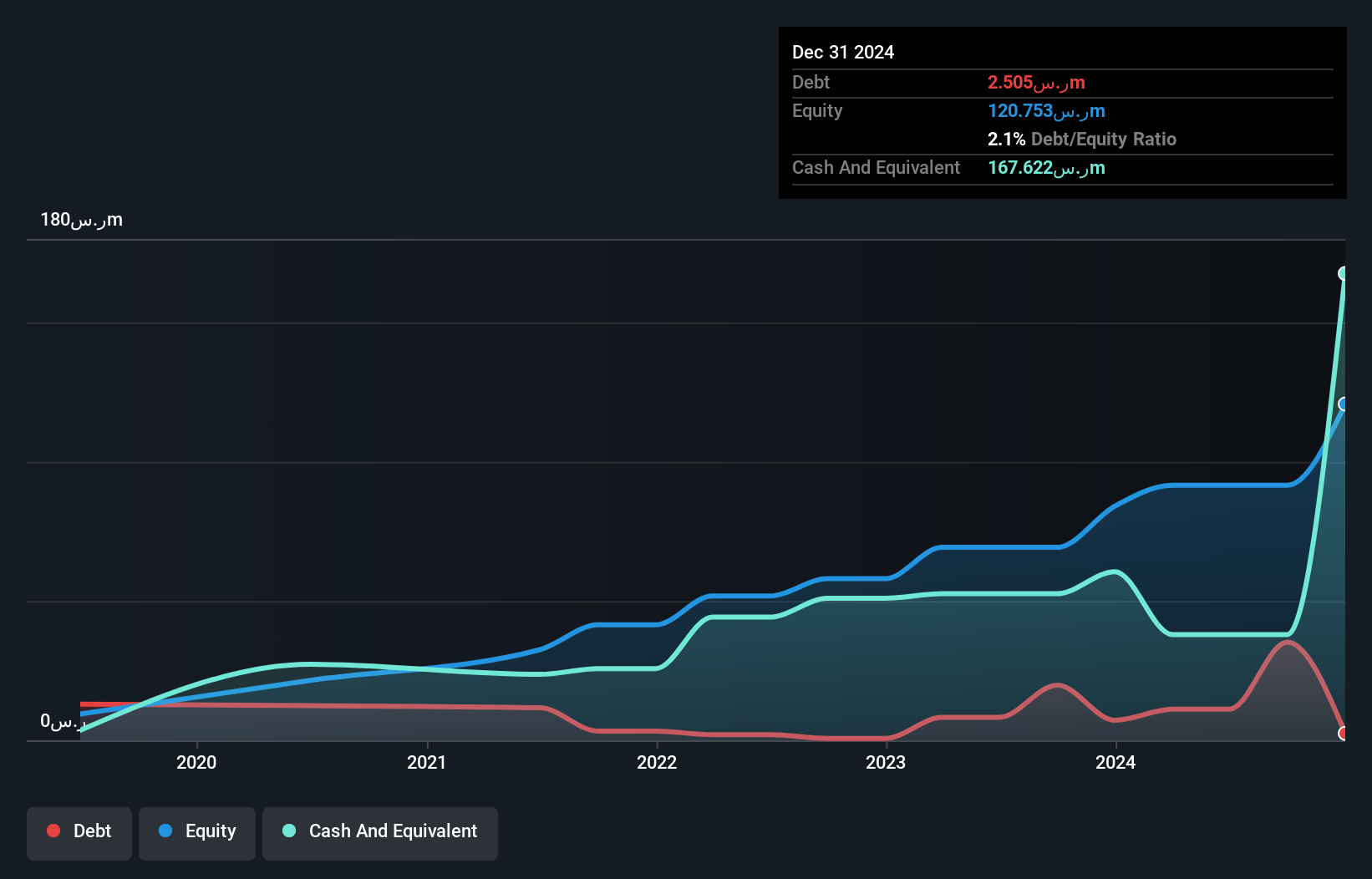

Saudi Azm for Communication and Information Technology (SASE:7211)

Simply Wall St Value Rating: ★★★★★★

Overview: Saudi Azm for Communication and Information Technology Company, along with its subsidiaries, offers business and digital technology solutions in Saudi Arabia, with a market capitalization of SAR 1.43 billion.

Operations: Saudi Azm generates revenue primarily from four segments: Advisory (SAR 35.83 million), Enterprise Services (SAR 139.27 million), Proprietary Technologies (SAR 54.04 million), and Platforms for Third Parties (SAR 33.29 million).

Saudi Azm for Communication and Information Technology has shown impressive growth, with earnings increasing by 31.8% over the past year, outpacing the IT industry's -8.3%. The company boasts high-quality earnings and a robust debt-to-equity ratio improvement from 43.9% to 3.3% in five years, indicating strong financial health. Recent announcements highlight a SAR 69.96 million sales figure for Q1 ending September 2025, alongside net income of SAR 13.45 million and basic earnings per share of SAR 0.24. With new projects like consulting services to enhance broadband quality across Saudi Arabia, future prospects appear promising for this emerging player in the region's tech landscape.

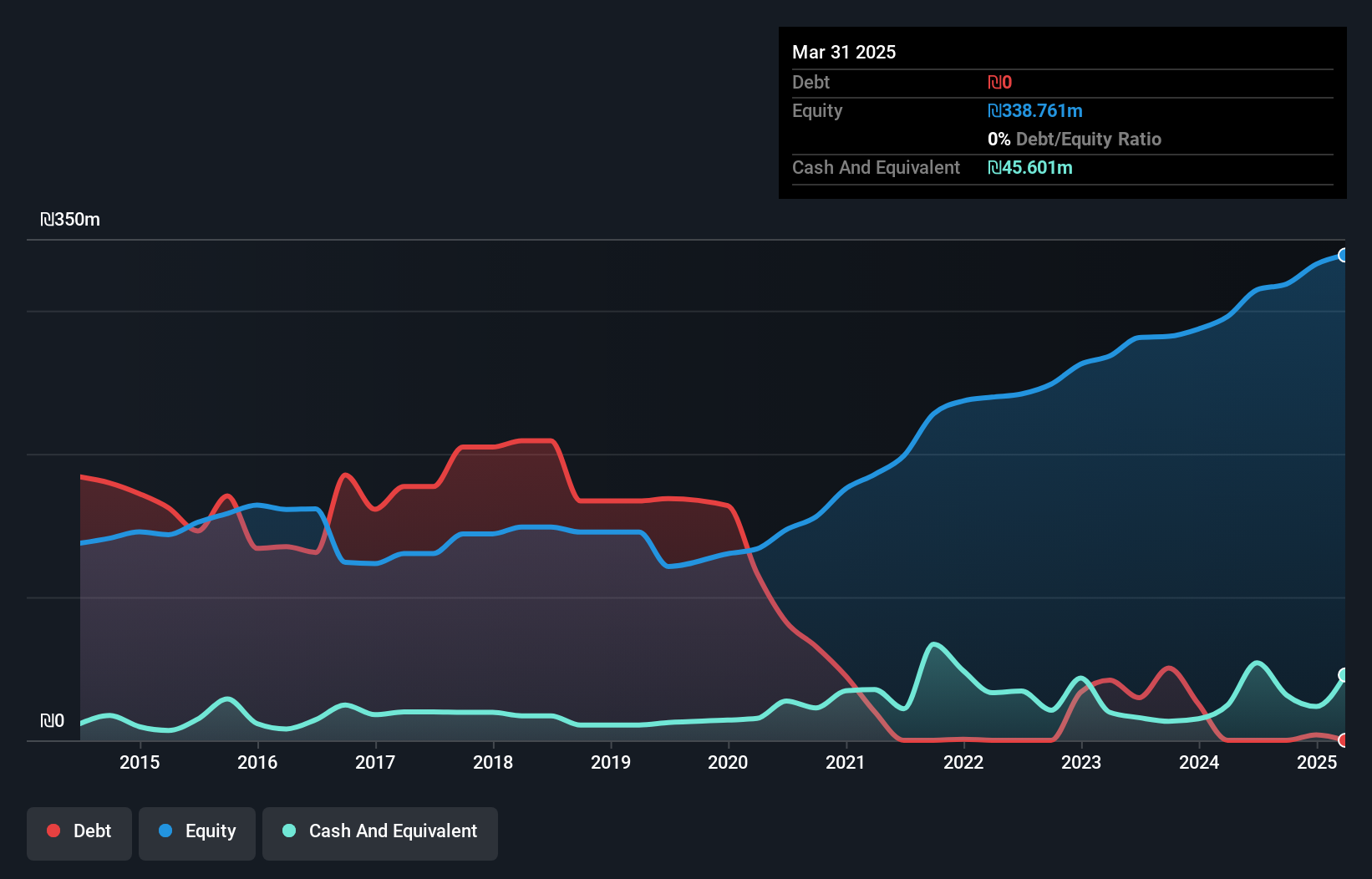

Tiv Taam Holdings 1 (TASE:TTAM)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Tiv Taam Holdings 1 Ltd. is engaged in the production, marketing, and importation of food products in Israel, with a market capitalization of ₪1.08 billion.

Operations: Tiv Taam generates revenue primarily through the production, marketing, and importation of food products in Israel. The company's net profit margin has shown variability over recent periods.

Tiv Taam Holdings 1, a dynamic player in the Middle East's consumer retail sector, has shown impressive growth with earnings surging by 38.8% over the past year, outpacing industry peers. Despite a historical average decline of 4.5% annually over five years, recent figures highlight a turnaround with Q3 sales reaching ILS 528.74 million and net income at ILS 15.55 million compared to last year's ILS 10 million. The company trades at an attractive valuation, about 46% below its estimated fair value while maintaining a satisfactory net debt to equity ratio of just 0.9%, suggesting robust financial health and potential for future growth.

Make It Happen

- Unlock more gems! Our Middle Eastern Undiscovered Gems With Strong Fundamentals screener has unearthed 179 more companies for you to explore.Click here to unveil our expertly curated list of 182 Middle Eastern Undiscovered Gems With Strong Fundamentals.

- Are these companies part of your investment strategy? Use Simply Wall St to consolidate your holdings into a portfolio and gain insights with our comprehensive analysis tools.

- Maximize your investment potential with Simply Wall St, the comprehensive app that offers global market insights for free.

Contemplating Other Strategies?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com