Has BlackBerry’s Stock Drop Created Opportunity After Recent Cybersecurity Expansion?

- Wondering if BlackBerry's stock price actually signals a true bargain or a value trap? You are not alone, as plenty of investors are curious about what lies beneath the recent numbers.

- After strong 55.6% gains over the past year, the stock has slipped by 18.7% in the last month. This could be an early sign of a shift in sentiment or risk appetite.

- Recent headlines have focused on BlackBerry's moves to strengthen its cybersecurity offerings and developments in its IoT initiatives, keeping the company top of mind for those watching tech innovation. Industry chatter also hints at renewed takeover speculation and strategic partnerships, which have played a role in fueling both optimism and caution among investors.

- Right now, BlackBerry scores just 2 out of 6 on our valuation checks. We have to dig deeper to see what this actually means. We are about to walk through the core valuation methods the market relies on, and at the end, we will look at an even more insightful way to judge what BlackBerry is really worth.

BlackBerry scores just 2/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: BlackBerry Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow (DCF) model estimates a company’s intrinsic value by projecting future cash flows and discounting them back to their present value. This approach tries to answer what BlackBerry is truly worth today, based on how much cash the business is expected to generate over time.

BlackBerry's latest Free Cash Flow stands at $17.3 Million. Analysts have provided projections for the next five years, estimating a jump to $130.5 Million in 2027. Beyond that, Simply Wall St extrapolates the trend, with forecasts suggesting Free Cash Flow could reach as high as $1.2 Billion by 2035 if growth continues. All values here are reported in dollars.

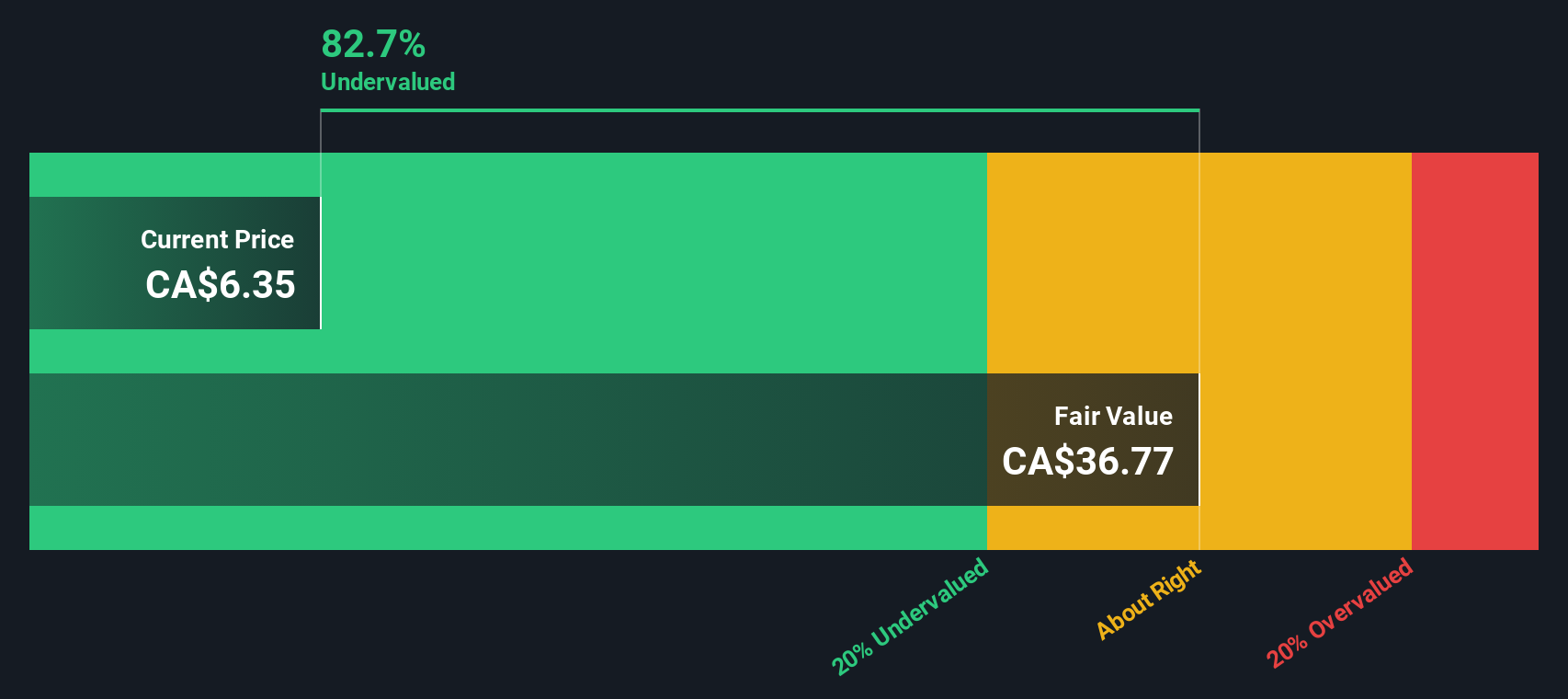

After crunching these numbers using the 2 Stage Free Cash Flow to Equity model, the estimated intrinsic value per share comes out to $37.84. This figure suggests that BlackBerry’s stock is currently trading at an 85.3% discount to its calculated fair value under this model, meaning the market may be substantially undervaluing these future cash flows.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests BlackBerry is undervalued by 85.3%. Track this in your watchlist or portfolio, or discover 932 more undervalued stocks based on cash flows.

Approach 2: BlackBerry Price vs Earnings (PE)

The Price-to-Earnings (PE) ratio is one of the most widely used valuation metrics for profitable companies because it relates a company’s stock price to its current earnings, offering a snapshot of how much investors are willing to pay for each dollar of profit. A high PE often reflects higher expected growth or lower risk. In contrast, a lower PE might suggest slower growth or greater uncertainty.

Currently, BlackBerry is trading at a PE ratio of 119.2x. For context, the average PE for the Software industry is 50.7x, and BlackBerry’s peer group average is 73.0x. These benchmarks show that the company’s valuation is well above both industry and peer norms, likely due to expectations of future turnaround or significant growth in earnings.

Simply Wall St’s proprietary “Fair Ratio” tool goes beyond simple comparisons. It considers BlackBerry’s specific characteristics, such as its earnings growth prospects, risk profile, profit margin, size, and its Software industry placement. According to this model, a fair PE ratio for BlackBerry would be 36.6x. This approach provides a more tailored measure than just using broad averages. As a result, it offers a more accurate reflection of what BlackBerry could reasonably be worth.

With the company’s actual PE ratio (119.2x) coming in much higher than its calculated fair PE (36.6x), BlackBerry appears overvalued based on this metric alone. Investors seem to be paying a significant premium for anticipated growth or a turnaround, which may not yet be justified by the fundamentals.

Result: OVERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1445 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your BlackBerry Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let's introduce you to Narratives. A Narrative is simply a user’s story or perspective about a company. It connects their view of BlackBerry’s future with concrete numbers, such as what they believe its fair value, future revenue, and margins could be. Narratives link the company’s story to a financial forecast and, ultimately, to a fair value estimate. This helps investors look beyond just the numbers to see the bigger picture.

On Simply Wall St's Community page, Narratives let anyone easily build, update, or compare investment opinions in real time, just like millions of other users already do. Narratives empower you to decide when to buy or sell by setting your own fair value and instantly comparing it to the current price. They also update automatically as fresh news or earnings come in. For example, one BlackBerry Narrative might confidently forecast a turnaround with a high fair value based on strong IoT growth, while another sets a much lower estimate citing continued profitability challenges. Narratives offer a smarter, more personalized way to transform how you invest.

Do you think there's more to the story for BlackBerry? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com