- PREMIUM

- LIVE QUOTES

Index Options

Index Options State Street

State Street CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street JournalInsights into HealthEquity's Upcoming Earnings

HealthEquity (NASDAQ:HQY) is gearing up to announce its quarterly earnings on Wednesday, 2025-12-03. Here's a quick overview of what investors should know before the release.

Analysts are estimating that HealthEquity will report an earnings per share (EPS) of $0.83.

The market awaits HealthEquity's announcement, with hopes high for news of surpassing estimates and providing upbeat guidance for the next quarter.

It's important for new investors to understand that guidance can be a significant driver of stock prices.

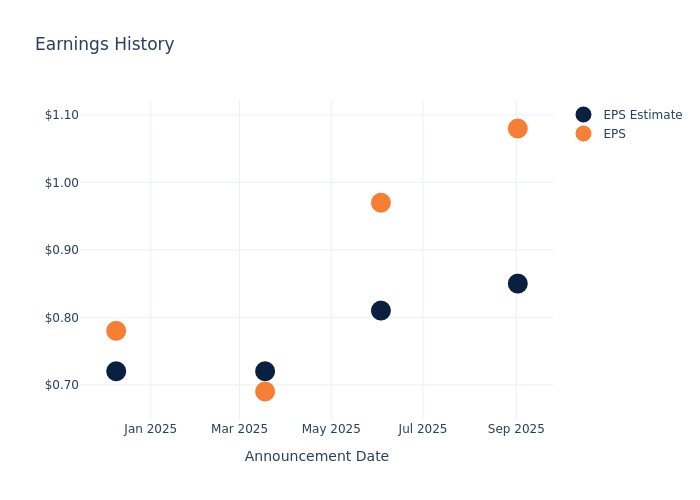

Past Earnings Performance

In the previous earnings release, the company beat EPS by $0.23, leading to a 7.53% increase in the share price the following trading session.

Here's a look at HealthEquity's past performance and the resulting price change:

| Quarter | Q2 2026 | Q1 2026 | Q4 2025 | Q3 2025 |

|---|---|---|---|---|

| EPS Estimate | 0.85 | 0.81 | 0.72 | 0.72 |

| EPS Actual | 1.08 | 0.97 | 0.69 | 0.78 |

| Price Change % | 8.00 | 9.00 | -17.00 | -6.00 |

Stock Performance

Shares of HealthEquity were trading at $102.41 as of November 28. Over the last 52-week period, shares are down 0.57%. Given that these returns are generally negative, long-term shareholders are likely a little upset going into this earnings release.

Analyst Views on HealthEquity

For investors, grasping market sentiments and expectations in the industry is vital. This analysis explores the latest insights regarding HealthEquity.

The consensus rating for HealthEquity is Outperform, derived from 6 analyst ratings. An average one-year price target of $119.17 implies a potential 16.37% upside.

Peer Ratings Overview

The below comparison of the analyst ratings and average 1-year price targets of Molina Healthcare, Alignment Healthcare and Progyny, three prominent players in the industry, gives insights for their relative performance expectations and market positioning.

- Analysts currently favor an Neutral trajectory for Molina Healthcare, with an average 1-year price target of $187.3, suggesting a potential 82.89% upside.

- Analysts currently favor an Neutral trajectory for Alignment Healthcare, with an average 1-year price target of $19.0, suggesting a potential 81.45% downside.

- Analysts currently favor an Neutral trajectory for Progyny, with an average 1-year price target of $27.33, suggesting a potential 73.31% downside.

Insights: Peer Analysis

Within the peer analysis summary, vital metrics for Molina Healthcare, Alignment Healthcare and Progyny are presented, shedding light on their respective standings within the industry and offering valuable insights into their market positions and comparative performance.

| Company | Consensus | Revenue Growth | Gross Profit | Return on Equity |

|---|---|---|---|---|

| HealthEquity | Outperform | 8.64% | $232.59M | 2.80% |

| Molina Healthcare | Neutral | 11.00% | $927M | 1.80% |

| Alignment Healthcare | Neutral | 43.51% | $125.67M | 2.46% |

| Progyny | Neutral | 9.32% | $72.83M | 2.58% |

Key Takeaway:

HealthEquity is positioned in the middle for revenue growth among its peers. It ranks at the bottom for gross profit. In terms of return on equity, HealthEquity is at the top compared to its peers.

Delving into HealthEquity's Background

HealthEquity Inc provides solutions that allow consumers to make healthcare saving and spending decisions. It provides payment processing services, personalized benefit information, the ability to earn wellness incentives, and investment advice to grow their tax-advantaged healthcare savings. It manages consumers' tax-advantaged health savings accounts (HSAs) and other consumer-directed benefits (CDBs) offered by employers, including flexible spending accounts and health reimbursement arrangements (FSAs and HRAs), and administers Consolidated Omnibus Budget Reconciliation Act (COBRA), commuter and other benefits. It also provides investment advisory services to customers whose account balances exceed a certain threshold. HealthEquity generates its revenue in the United States.

Financial Milestones: HealthEquity's Journey

Market Capitalization Analysis: Falling below industry benchmarks, the company's market capitalization reflects a reduced size compared to peers. This positioning may be influenced by factors such as growth expectations or operational capacity.

Revenue Growth: HealthEquity displayed positive results in 3 months. As of 31 July, 2025, the company achieved a solid revenue growth rate of approximately 8.64%. This indicates a notable increase in the company's top-line earnings. In comparison to its industry peers, the company trails behind with a growth rate lower than the average among peers in the Health Care sector.

Net Margin: HealthEquity's net margin excels beyond industry benchmarks, reaching 18.37%. This signifies efficient cost management and strong financial health.

Return on Equity (ROE): HealthEquity's ROE surpasses industry standards, highlighting the company's exceptional financial performance. With an impressive 2.8% ROE, the company effectively utilizes shareholder equity capital.

Return on Assets (ROA): The company's ROA is a standout performer, exceeding industry averages. With an impressive ROA of 1.75%, the company showcases effective utilization of assets.

Debt Management: HealthEquity's debt-to-equity ratio is below industry norms, indicating a sound financial structure with a ratio of 0.49.

To track all earnings releases for HealthEquity visit their earnings calendar on our site.

This article was generated by Benzinga's automated content engine and reviewed by an editor.