Park Hotels Rebounds 5% This Month as Valuation Metrics Suggest Room for Growth

- Wondering if Park Hotels & Resorts could be a hidden value play or if there are warning signs you should notice before jumping in? If you have an eye for real estate stocks and are curious where the real opportunity lies, you are in the right place.

- The stock has posted a modest rebound lately, moving up 2.9% over the past week and 5.2% in the last month. However, it is still down about 21% for both the year-to-date and the past year, despite a 24.6% gain over the last three years.

- These moves come as the hospitality sector finds its footing after bouts of market volatility and shifting travel demand. Real estate investment trusts like Park Hotels & Resorts have seen renewed attention from investors as broader market outlooks improve and travel trends continue to evolve.

- When it comes to valuation, Park Hotels & Resorts scores a strong 5 out of 6 on our valuation checks, signaling potential undervaluation based on key metrics. We will dig into what these numbers mean using a few classic valuation methods, but make sure to stick around for an even smarter approach we will reveal at the end.

Find out why Park Hotels & Resorts's -21.1% return over the last year is lagging behind its peers.

Approach 1: Park Hotels & Resorts Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow (DCF) model estimates a company's intrinsic value by projecting its expected adjusted funds from operations, often using free cash flow reports, and then discounting those future cash flows back to present-day dollars. This approach helps investors understand how much the company's future potential is worth in today’s terms.

For Park Hotels & Resorts, the current Free Cash Flow stands at $430 million. Analyst forecasts and internal estimates suggest this figure will grow gradually over time, with projections reaching about $424 million by 2035. Most of the estimates for the next few years are directly from analysts, while longer-term forecasts beyond 2027 are extrapolated by Simply Wall St using recent trends.

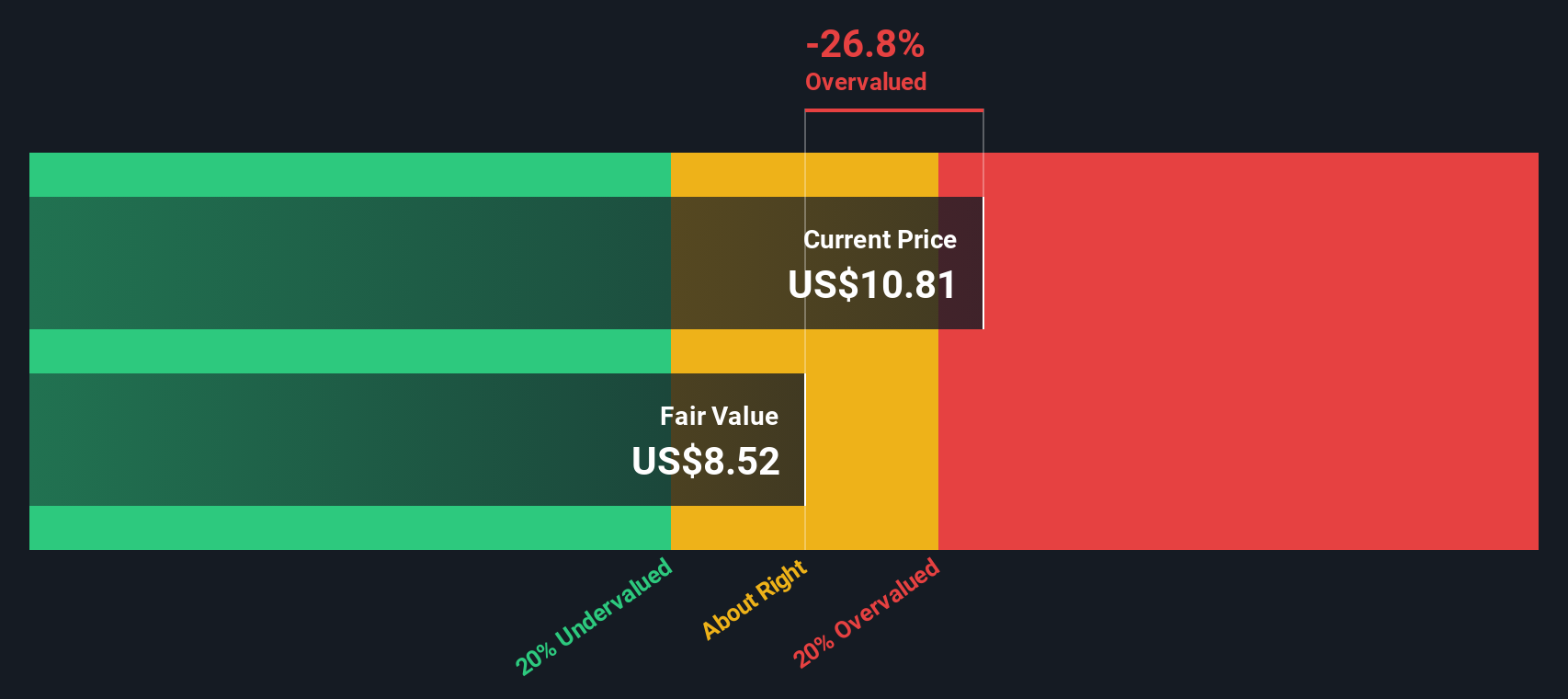

Based on this DCF analysis, Park Hotels & Resorts has an estimated intrinsic value of $20.85 per share. This amount reflects a 48.1% discount compared to the stock’s current market price, signaling significant undervaluation.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Park Hotels & Resorts is undervalued by 48.1%. Track this in your watchlist or portfolio, or discover 915 more undervalued stocks based on cash flows.

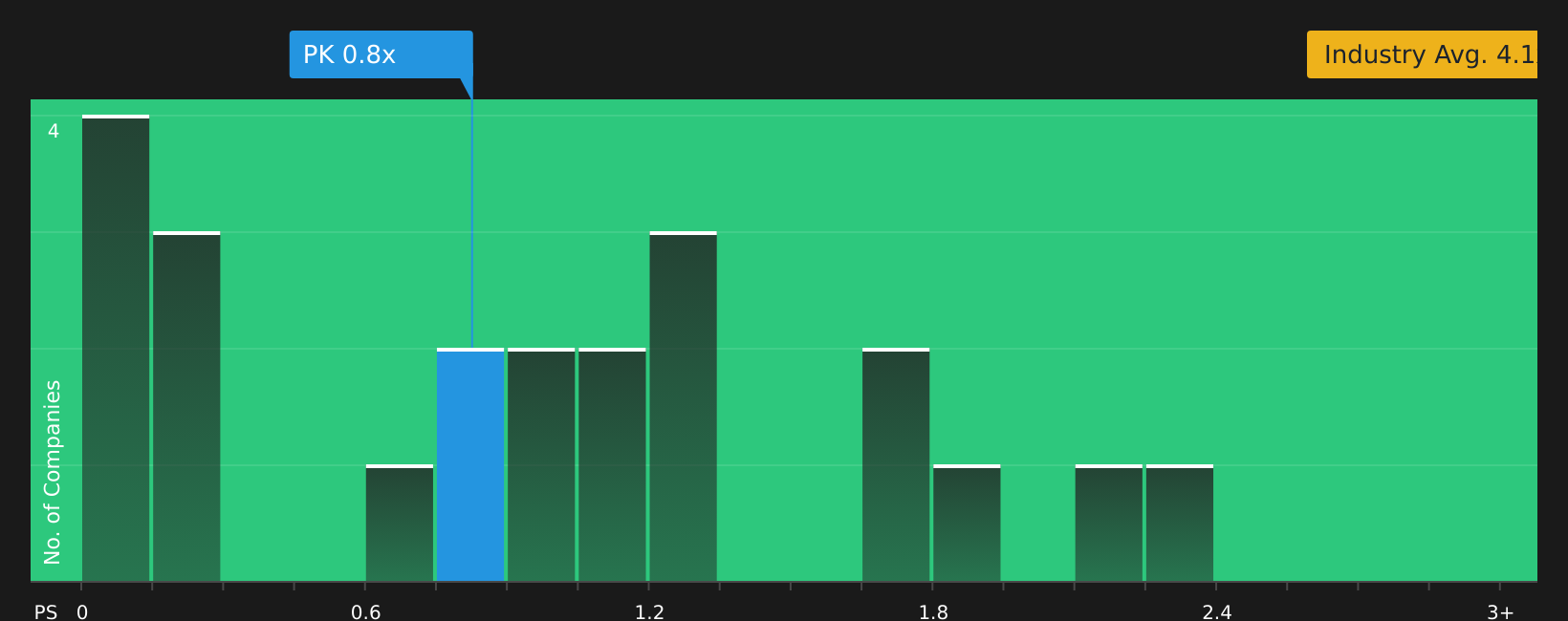

Approach 2: Park Hotels & Resorts Price vs Sales

For companies like Park Hotels & Resorts, the Price-to-Sales (P/S) ratio is a useful valuation metric. The P/S multiple highlights the value investors are placing on each dollar of the company’s revenue. This is particularly relevant for real estate investment trusts and capital-intensive businesses, where profitability may fluctuate from period to period.

Generally, growth expectations and business risk both influence what constitutes a "fair" P/S ratio. Investors tend to pay higher multiples for companies with strong revenue growth and lower perceived risk. Firms experiencing slower growth or facing elevated risks will usually command lower multiples.

Currently, Park Hotels & Resorts trades at a P/S ratio of 0.85x. This figure stands well below the Hotel and Resort REITs industry average of 3.77x and the peer average of 1.69x. This indicates the stock is priced much lower than many comparable companies in its sector.

Simply Wall St’s proprietary “Fair Ratio” model is designed to calculate an appropriate multiple by considering the company’s earnings growth, profit margins, risk profile, industry characteristics, and market cap. This model suggests a fair P/S ratio for Park Hotels & Resorts would be 1.63x. Compared to generic industry or peer averages, this Fair Ratio better reflects the company’s unique specifics and helps identify whether the current price is actually justified.

Since Park Hotels & Resorts is trading at a P/S ratio more than 0.10x lower than its fair value benchmark, the stock currently appears undervalued by this measure.

Result: UNDERVALUED

PS ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1441 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Park Hotels & Resorts Narrative

Earlier we mentioned that there is an even better way to understand valuation. Let us introduce you to Narratives. Narratives transform investing beyond just numbers by connecting each investor's unique view of a company’s story, including how it may grow, which risks are most important, and what the future could look like, to real financial forecasts and an estimated fair value. Simply put, a Narrative is your way of expressing why you think a company is worth more or less, based on the assumptions you believe are most realistic.

Narratives are simple and accessible. They are featured right on Simply Wall St’s Community page, where millions of investors share and compare their perspectives on companies like Park Hotels & Resorts. You can instantly see how a Narrative links expected revenue growth, margins, and risks to a fair value, and then compare this to the current market price to help determine whether it may be time to buy, hold, or sell.

Best of all, Narratives automatically update as new information, such as breaking news or quarterly earnings, becomes available, so your story and your calculations always stay relevant. For example, some investors currently view Park Hotels & Resorts as a turnaround story poised for a $21.00 valuation due to high-end renovations and premium travel demand, while others warn of risks that could keep fair value closer to $10.00.

Do you think there's more to the story for Park Hotels & Resorts? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com