CICC: Dividends have become a “safe haven” in the midst of Hong Kong stock turbulence, focusing on dividend assets and the three major structural opportunities

The Zhitong Finance App learned that CICC released a research report saying that in the past two months, the Hong Kong stock market has been volatile, tangled, and lacking direction. In this context, dividends have become the first choice in a “no match between good and bad” environment. The banking sector has rebounded nearly 10% since the end of September. Regarding dividend assets and the three major structures (AI industry trends, traditional domestic demand, and external demand drive the procyclical cycle), CICC believes that the advantage of the AI industry is that industry trends are still there and domestic policy support; the shortcomings are high valuations and high expectations, and new catalysts are needed; choosing the path of domestic hardware replacement in the short term, and the implementation of application-side demand and profit in the long term.

In terms of external demand, external demand drives the procyclical cycle. The US credit cycle restarts expansion or drives the recovery of the global manufacturing cycle. It is not enough to look at the whole year level or lack sustainability; in addition, the domestic PPI phase picked up in the first quarter or provided a short-term trading window; and the selection of lines combined with capacity supply to find flexibility. However, the advantage of traditional domestic demand is that valuations and expectations are not high, and the shortcoming is that it lacks profit support; it may have potential swing trading opportunities under policy catalysts, but beware of “static valuation traps.” In terms of dividends, the essence of dividends is a hedge against “weak domestic demand”. Hong Kong stock dividend rates are still attractive, but the optional range is shrinking.

CICC's main views are as follows:

Over the past two months, the market has been volatile, tangled, and lacking direction. On the one hand, it is because the expectations and positions of the technology growth sector are high, making investors sensitive to negative losses. Coupled with concerns about the AI bubble in the US stock market and “adding chaos” to the cooling expectations of the Federal Reserve's interest rate cut, they all amplified fluctuations. Hang Seng Technology once pulled back about 16.6% at most.

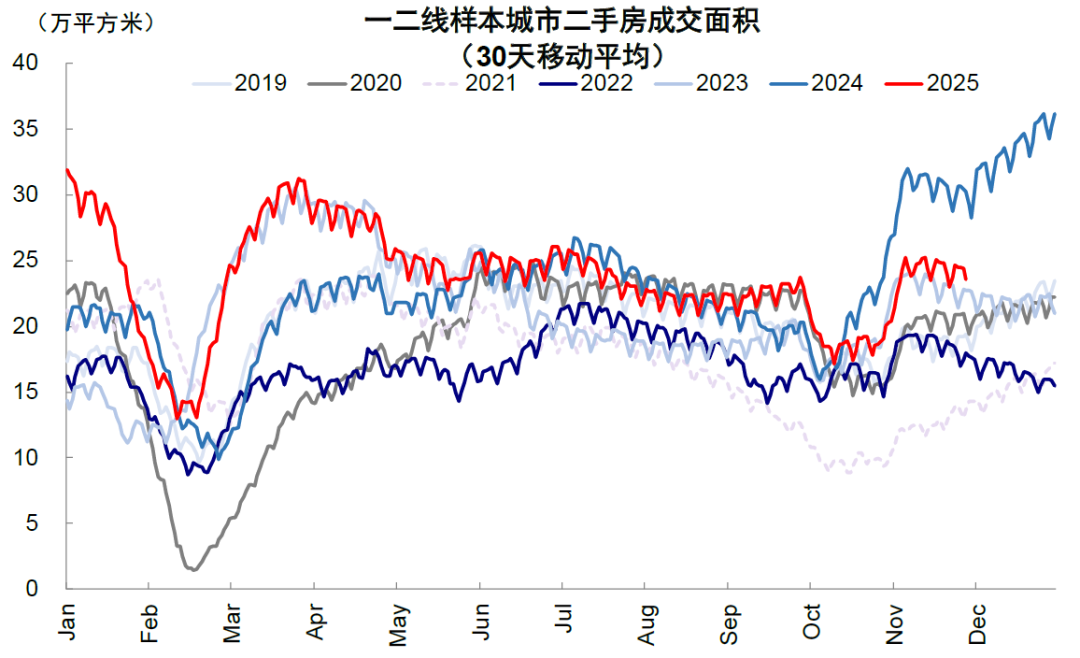

On the other hand, the domestic demand consumption and real estate chain, which is a “high cut and low” candidate, although valuations and positions are very cost-effective, the recent accelerated weakening of fundamentals (Chart 1) makes it difficult to reach consensus within investors. In this context, dividends have become the first choice in a “no match between good and bad” environment. The banking sector has rebounded nearly 10% since the end of September. Our optimism about the Hang Seng Index at 26,000 points is still appropriate. Even if it broke through once in October, we have not raised it; it has been verified at present.

Chart 1: Recent marginal weakening of real estate data

Source: WinD, CICC Research Division

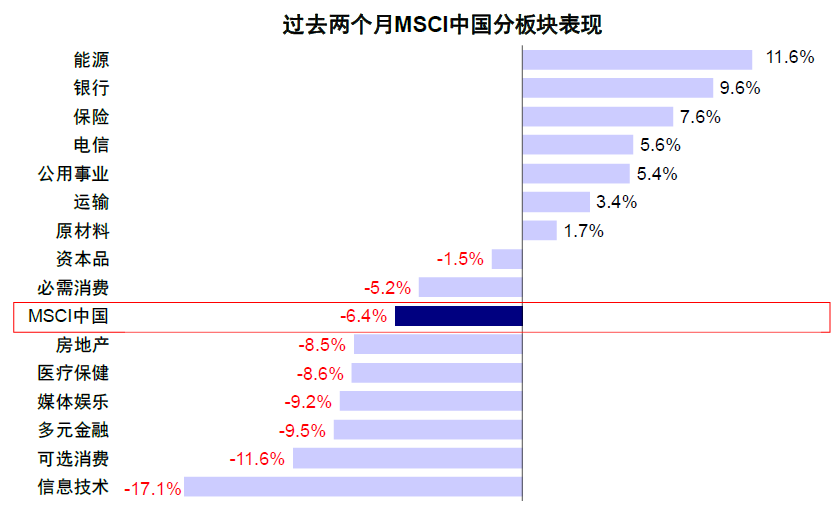

Chart 2: Overall, Hong Kong stocks have fluctuated in the past two months, and dividend-style industries such as banks have performed well

Source: FactSet, CICC Research Division

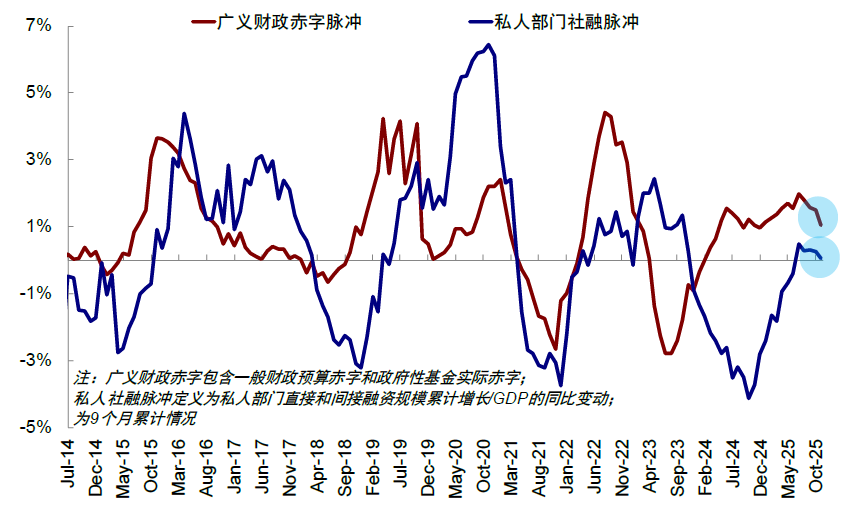

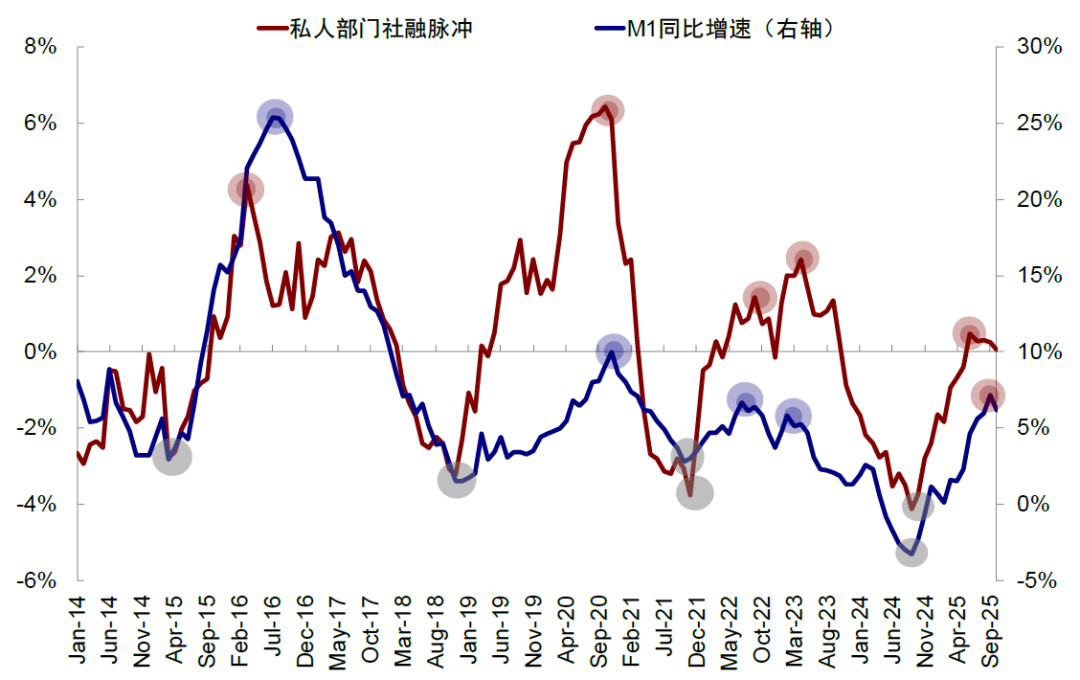

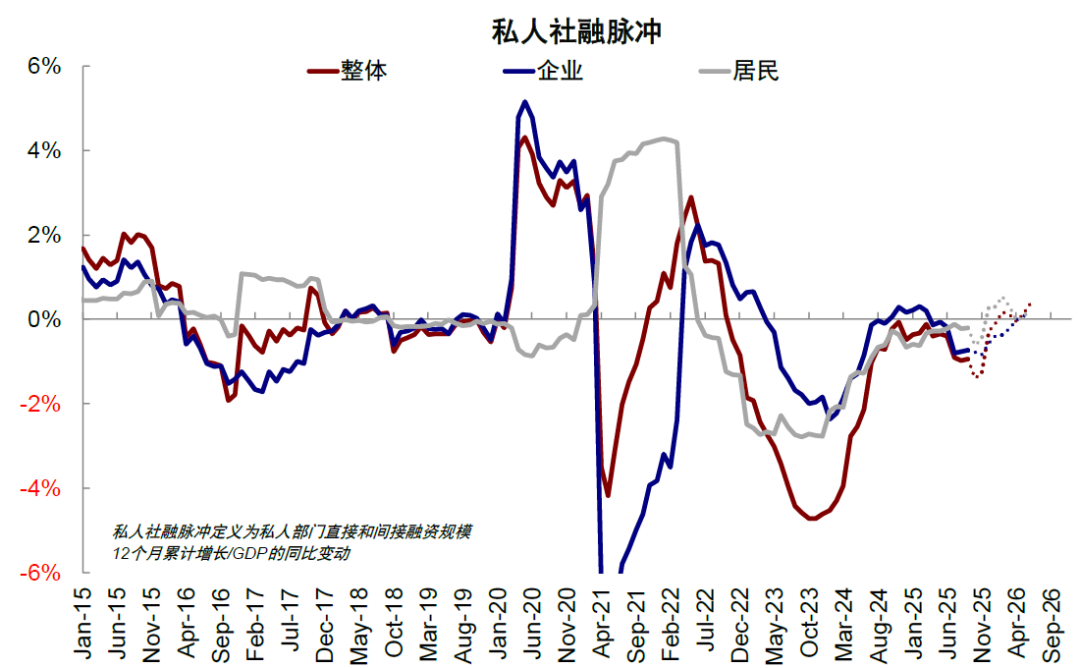

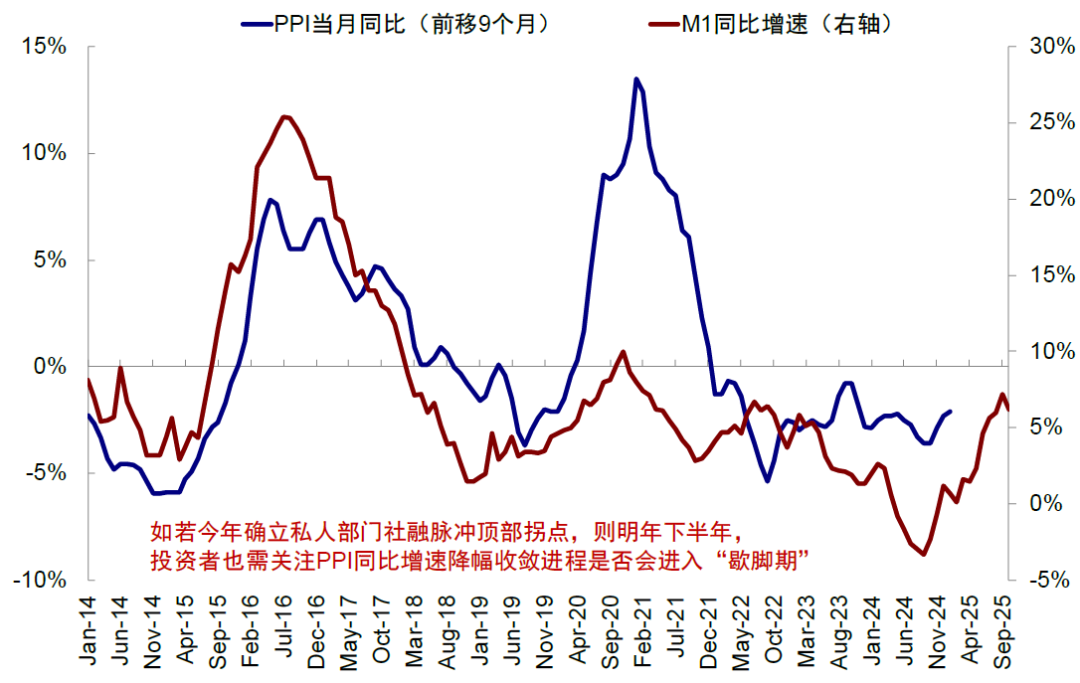

Whether the market is entangled or dividends and technology fluctuate back and forth, they are essentially all “out of touch” between current fundamentals and expectations, and they are also a direct reflection of the weakening of domestic credit cycle fluctuations (Chart 3). This has been verified whether the private social finance pulse peaked first in June or the domestic M1 growth rate declined marginally in October (Chart 4). We also had tips before. In previous research reports, we suggested that if policies cannot be hedged in a timely manner, they will either take risk in stages or return to the boom structure.

Chart 3: Behind market performance is weak domestic credit expansion

Source: Wind, CICC Research Division

Chart 4: The year-on-year growth rate of M1 also began to decline marginally in October

Source: Wind, CICC Research Division

Tangled up is entanglement. Looking ahead, how should it be distributed is a common concern in the current market: is it possible to fix technology and not relax, or to balance more dividends, or can it be possible to advance domestic demand consumption that no one has paid attention to for a long time? We believe that the credit cycle can not only guide the overall macroeconomic trend, but also an effective comparison framework that can help us choose the direction of allocation.

Following credit expansion: It is the direction of demand and return, as well as the direction of allocation

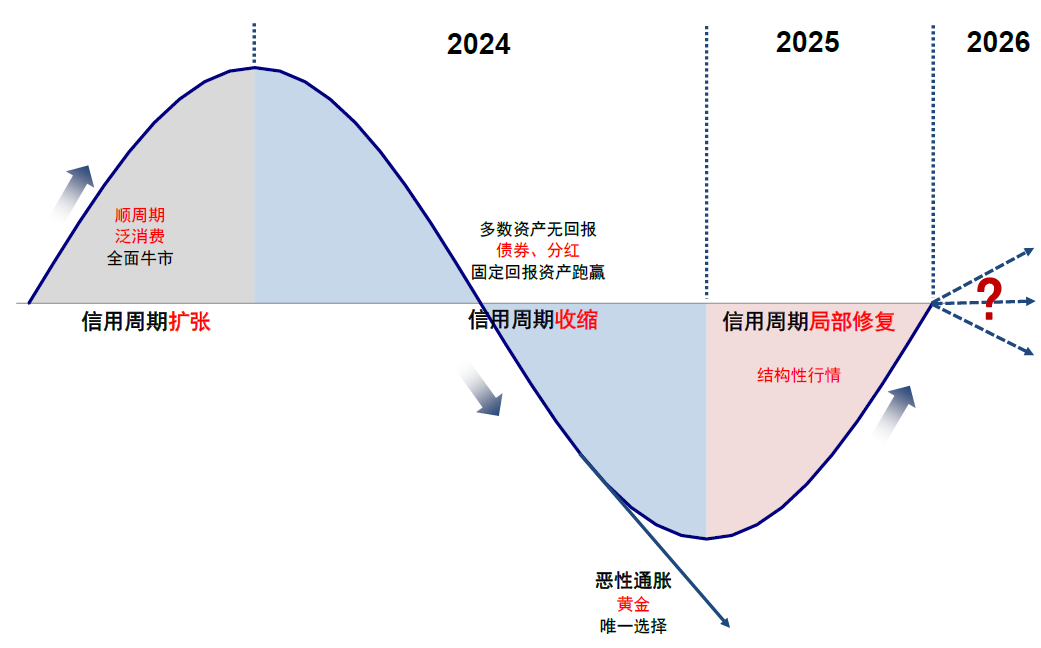

The essence of the context and rotation characteristics of China's assets over the past two years can be summed up as “excess liquidity” chasing “scarce assets.” In the digital economy era, information gaps are getting smaller, and it is easy to reach consensus. Once an asset is recognized as a “scarce asset,” market consensus will drive a large influx of excess liquidity, causing asset prices to rise rapidly in the short term, leading to overdrafts, and then liquidity will flock to the next opportunity. Over the past two years, dividends, treasury bonds, gold, and growth have all been the same, which is why they have continuously rotated.

On the one hand, “excess liquidity” is essentially the result of a sluggish credit cycle. The “excess” of liquidity is relative; it is the other side of this coin where effective demand is insufficient. Liquidity cannot be converted into credit expansion, leading to idling and stagnation. On the other hand, “scarce assets” are also determined by the credit cycle: 1) when the overall credit cycle shrinks, assets such as bonds and dividends are “scarce assets”, such as 2024; 2) when the credit cycle is partially repaired, they will be reflected in structured markets, such as the fluctuating Internet, new consumption, and innovative drugs in 2025. At this time, searching for scarce assets is the direction of seeking structural credit expansion; 3) If the entire credit cycle is repaired, it can only be reflected in an overall bullish market with procyclical and widespread consumption; 4) In extreme cases, even fixed assets can return in an all-round bull market with pro-cyclical and pan-consumption; 4) In extreme cases, even fixed assets are returned in an overall bull market with pro-cyclical and widespread consumption; 4) In extreme cases, even fixed assets are returned in an overall bull market with pro-cyclical and widespread consumption; 4) In extreme cases, even fixed assets are returned in an overall bull market with pro-cyclical and widespread consumption; 4) In extreme cases, even fixed assets are returned in an all-out bull market with pro-cyclical and pan-consumption returns; 4) Center for hyperinflation Eroded, and gold became the only option (Chart 5).

Chart 5: Different credit cycle quadrants correspond to different scarce assets

Source: Wind, CICC Research Division

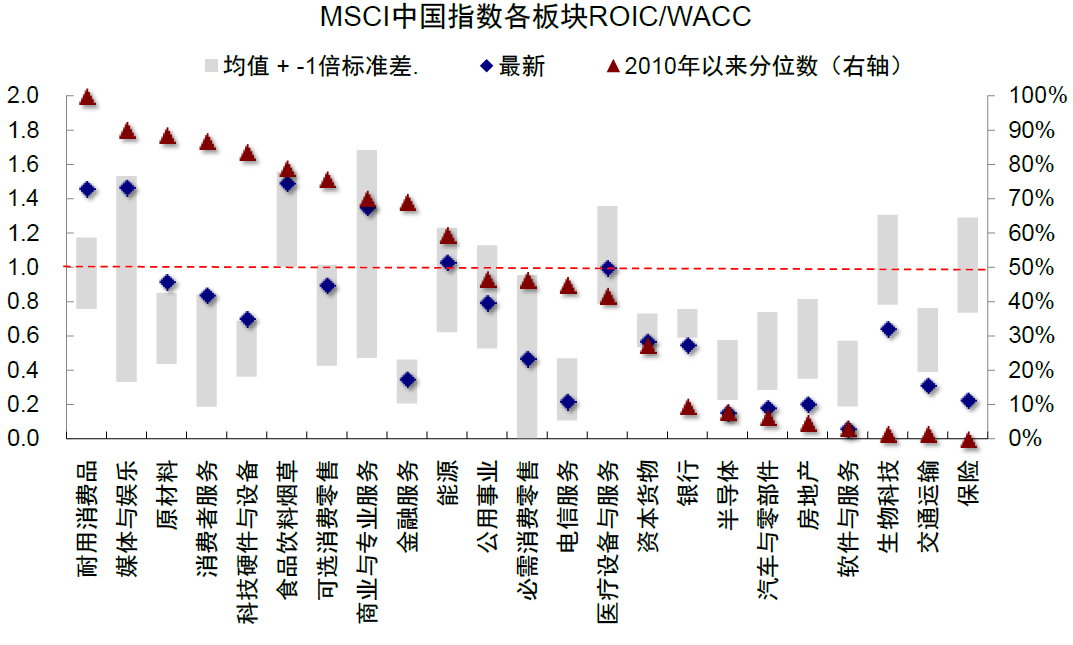

Chart 6: The ROIC/WACC sector of enterprises is clearly divided

Note: Data as of September 30, 2025

Source: Wind, Bloomberg, CICC Research Division

Judging from the 2026 Hong Kong stock outlook, in the face of a high base, declining revenue expectations, and structural problems where return costs are still inverted, China's credit cycle is likely to fluctuate or even decline in stages unless fiscal strength is greatly accelerated. Previously, optimistic expectations of low base restoration, boom industry structure, and liquidity narratives “covered up” the structural problems that had always existed to a certain extent. When the momentum of these factors gradually ran out, structural problems became prominent again, so it is not surprising that real estate has weakened again recently.

Following this line of thought, when choosing an industry, it is still necessary to follow the direction of credit expansion, which at least represents the direction of demand and expected returns. Specifically: 1) Whether viewed from the perspective of the AI industry itself or the 15th Five-Year Plan policy bias, technology will still be a continuous boom direction. It can be further divided into A-share hardware and Hong Kong stock software. The former is highly flexible and the latter is resilient; however, the downside is that valuations, positions, and expectations are high, so additional industrial progress or liquidity is needed to catalyze; 2) Domestic demand consumption and real estate chains. Although expectations, positions, and valuations are all low, it is difficult to form a continuous consensus. If policy catalysis occurs, it may be difficult to form a continuous consensus. Opportunities, beware of “static valuation traps”; 3) In the context of domestic demand credit contraction, dividends are still a good hedging option. 4) The external demand chain can focus on strong cycles and early cycles. The catalyst comes from the US treasury to increase physical investment efforts ahead of the midterm elections. Interest rate cuts by the Federal Reserve exceed expectations. At the same time, domestic PPI in the first quarter benefited from a low base and the lagging effects of rising M1 in the previous period will continue to rise, such as the recent rise in copper prices, which can be combined with capacity supply (Chart 7).

Chart 7: Investment advantages and disadvantages in the four major sectors, and ways to choose the right time

Source: CICC Research Division

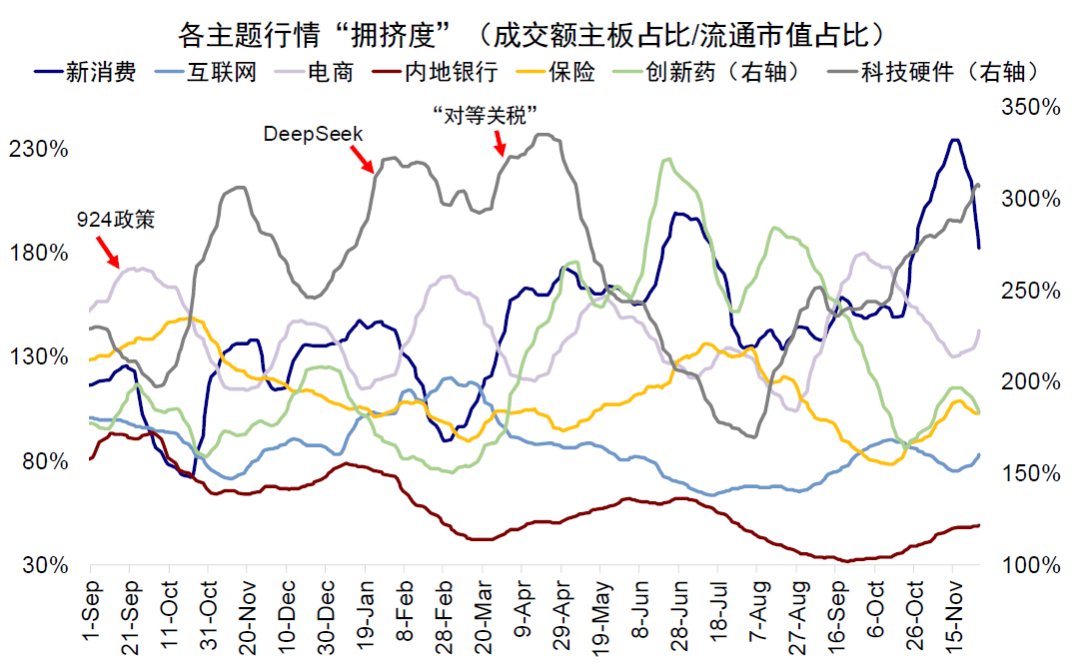

Overall, investors can still continue to use the “dumbbell” combination (dividend+technology internet) as an allocation base and dynamically adjust the weight of the portfolio in line with the level of congestion (Chart 8), which can have a good hedging and balancing effect. On this basis, procyclics driven by external demand (non-ferrous materials such as copper and aluminum, chemicals, construction machinery, and even real estate chains) and innovative drugs can be combined as flexible choices, especially in the first quarter. In contrast, the domestic consumer sector will still be dragged down by fundamentals.

Figure 8: Combined configuration weights can be dynamically adjusted in conjunction with congestion

Source: Wind, CICC Research Division

Comparison of four categories of directions: technology, procyclical external demand, domestic consumption, dividends

Regarding dividend assets and the three major structures (AI industry trends, traditional domestic demand and external demand drive the procyclical cycle), we discuss each asset sector in more detail from a credit cycle perspective, sort out the current strengths and weaknesses of each sector through systematic classification, and provide timing signals and path selection ideas:

AI industry: The advantage is that industry trends are still ongoing, and domestic policy support; the shortcoming is that high valuations and expectations are high, and new catalysts are needed; choosing the path depends on domestic hardware replacement in the short term, and the implementation of application-side demand and profit in the long term.

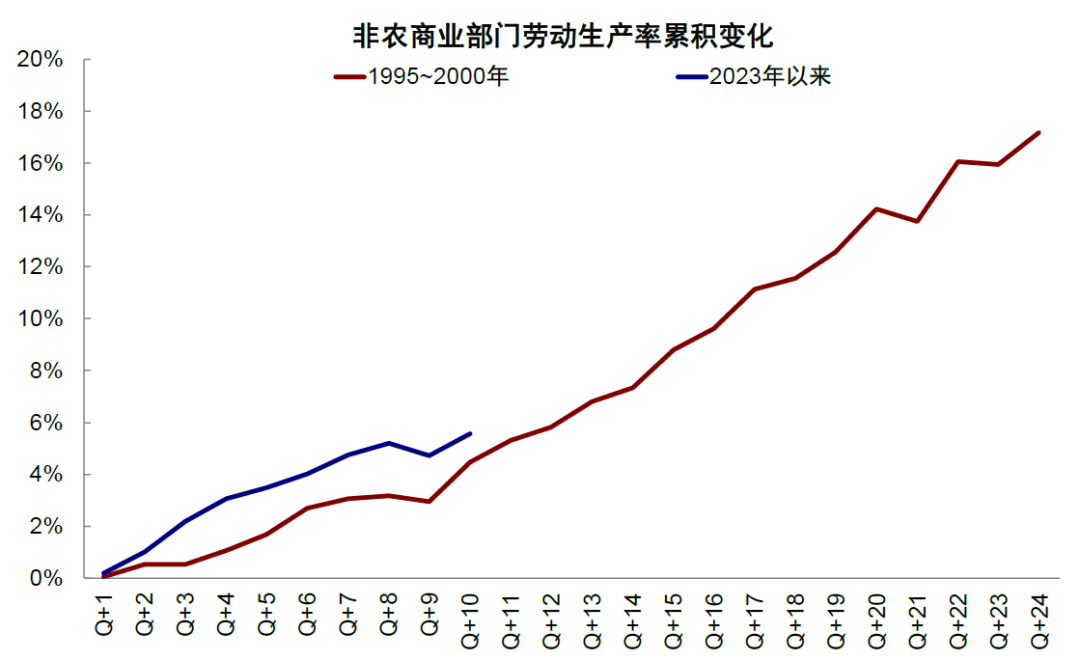

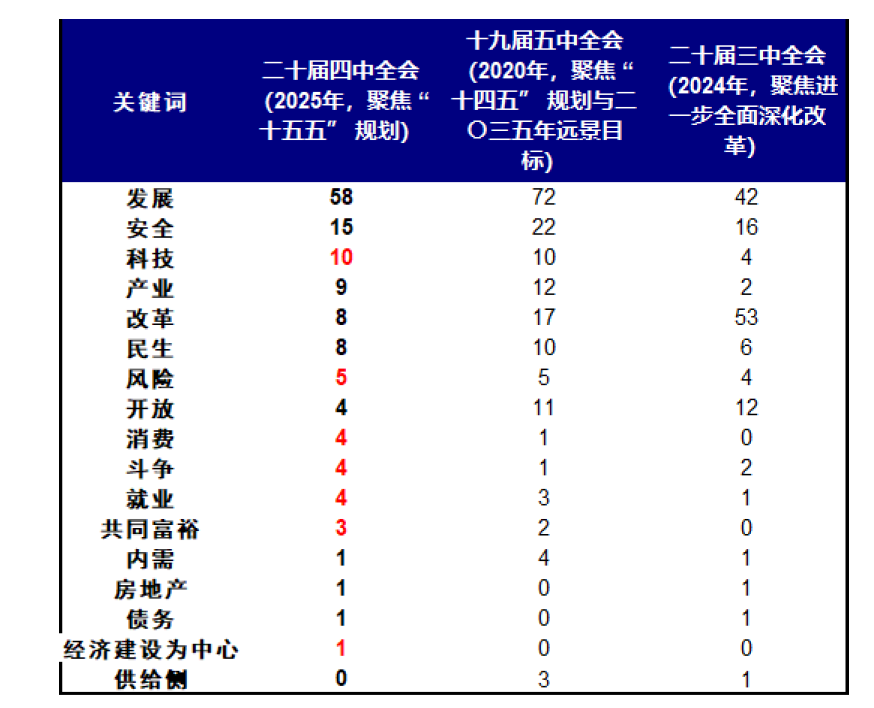

The advantage lies in fundamental support. First, the global AI industry trend is likely to continue. Although the recent market has once again sparked discussions and concerns about the AI bubble, we believe that the current stage of development of the AI industry may be more similar to the situation in the 1996-1998 technology network market. Referring to previous research reports, judging from the three dimensions of current demand, financing capacity, and market pricing, 1) demand is close to 1996-1997. Endogenous cost reduction and efficiency have been realized, and epitaxial demand still needs to be broken through. The increase in revenue and productivity is similar to 1996-1997 (Chart 9). 2) The investment is close to 1997-1998, and the scale is still in its infancy, but the dependence on financing is far lower than at that time (Chart 11). 3) The primary market pricing is close to 1999, and the secondary market valuation and policy environment is close to 1998. Second, domestic policies are also biased towards the AI sector. Technological innovation and industrial development have always been China's key policy directions. The frequency statistics announced by the Fourth Plenary Session of the Central Committee (Chart 13) and the recent investment direction of new policy financial instruments also show that developing China's own technology industry chain and reducing dependence on other countries is still a top priority in industrial development. Based on this, domestic substitution will continue to be the direction of policy strength, and the domestic AI industry chain (in particular, hardware links such as semiconductors) will also receive a steady stream of policy preferences and investment support, making the investment and development of the domestic AI industry chain more fundamentally certain.

Chart 9: The current productivity increase brought about by AI is similar to that of the 1996-1997 period of the Internet market

Source: FactSet, CICC Research Division

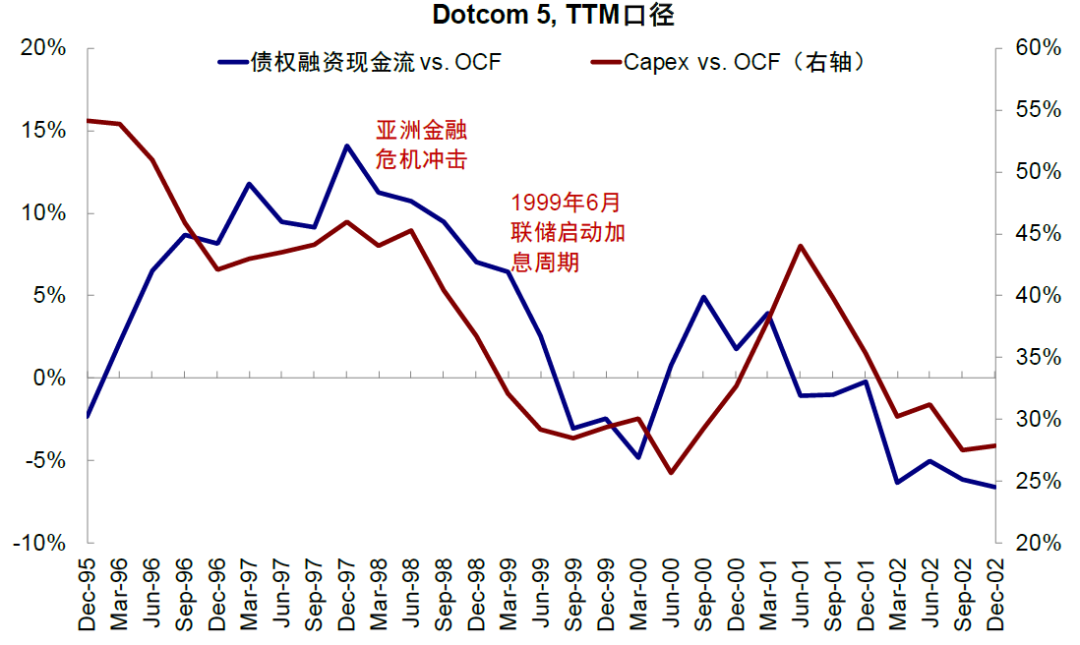

Chart 10: During the Internet revolution, marginal changes in bond financing cash flow were strongly correlated with marginal changes in capital expenditure

Source: FactSet, CICC Research Division

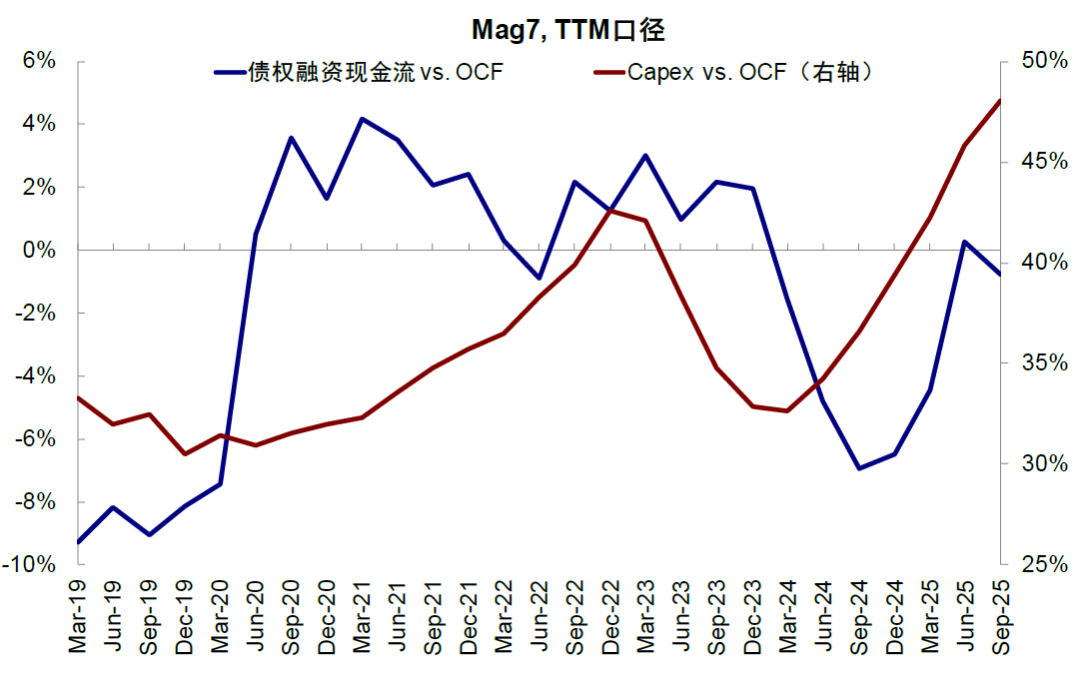

Chart 11: Up to now, there is no clear correlation between Mag 7 bond financing cash flow and marginal changes in capital expenditure in this round of markets

Source: FactSet, CICC Research Division

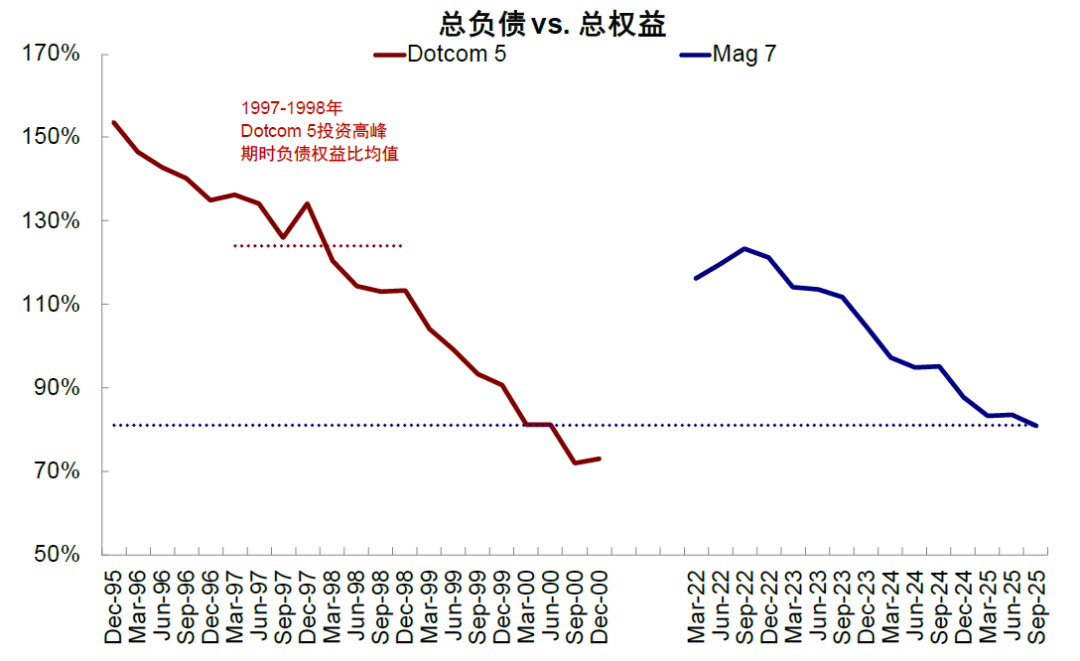

Chart 12: The current debt-to-equity ratio of Mag7 is lower than the peak level of Capex, the leading company during the Internet revolution

Source: FactSet, CICC Research Division

Figure 13: Word frequency statistics show that technology is still a top priority for the current government

Source: Chinese Government Network, CICC Research Department

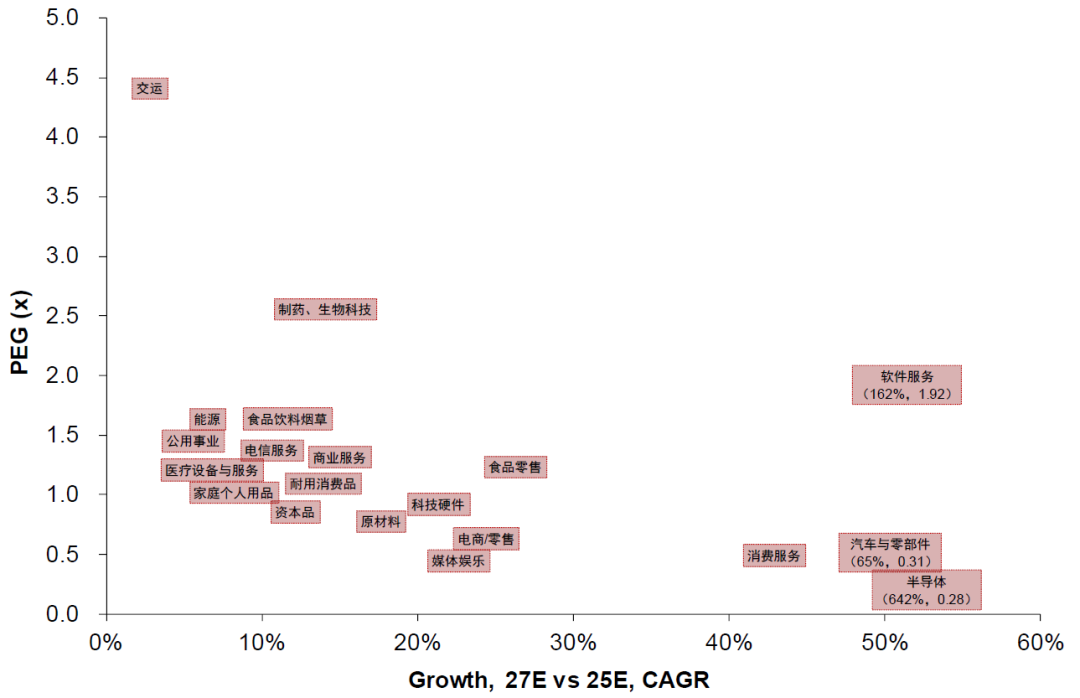

It is insufficient for “high expectations”, “high valuations” and “high volatility” derived from both; further upward space may be needed to drive it. Based on FactSet's unanimous expectations, the market currently expects the 10-year performance growth rate of the US stock Mag 7 and China Terr to be around 20% (based on the 27E and 25E EPS calculation 2-year CAGR growth rate as the standard for “growth”), and the current market expectations are relatively high. For Mag 7, considering that its forward price-earnings ratio is currently around the 30x line, the PEG valuation of about 1.5x water level is also difficult to “underestimate”, which also shows a certain “fragility” in its market performance. For Terr 10, although the absolute valuation is lower than that of leading US stocks, when combined with its static operating situation, the market actually expects the future performance of leading Chinese stocks to be relatively high; furthermore, if Mag 7 fluctuates in valuation, the corresponding Chinese assets are also “inevitably mapped.” Therefore, if there are new catalysts, such as breakthroughs at the domestic hardware level, or further breakthroughs on the AI application side, the AI sector may open up room for further upward growth; if there is no new catalysis, the AI sector may continue to fluctuate, and potential profit space may stem from a phased retracement.

Timing signals: One is the progress of the industry, and the other is the liquidity environment. When choosing the AI sector, on the one hand, it is necessary to constantly observe whether there are new catalysts in the progress of the industry, especially whether there are key breakthroughs on the demand application side. On the other hand, the liquidity environment, such as the pace of the Fed's interest rate cuts and table expansion, will also affect the performance of the period. There are three window periods: 1) whether the FOMC cuts interest rates in December, which we believe “should and can be lowered”; 2) progress in subsequent table expansion at the end of this year and the beginning of next year, after the new Federal Reserve chairman is elected, the market will reprice its views and subsequent interest rate cut path.

How to select lines within the AI sector? Look at domestic hardware replacement in the short term, and look at application-side demand and profit fulfillment in the long term. The current market's performance growth expectations for hardware (such as MSCI China's semiconductor industry, etc.) are higher than in the application sector (such as MSCI China software, media entertainment, etc.) (Chart 14). Underlying the differences are certainly large differences in calculation results brought about by a high or low performance base, but there are also factors of strong domestic policies, especially domestic substitution policies, and this is also the biggest difference between China's AI-related assets and the AI sector of US stocks. In the long run, if the AI industry continues to develop and the application side makes significant breakthroughs in the future (such as explosion-level AI applications and monetization progress), it may further open up valuation space for the AI software sector in China and the US.

Chart 14: Current market expectations for AI hardware assets are higher than software

Source: FactSet, CICC Research Division

External demand drives the procyclical cycle: the US credit cycle restarts expansion or drives the global manufacturing cycle to pick up; it is not sustainable in terms of the whole year; choosing the right time to look at manufacturing PMI and existing housing sales; in addition, the domestic PPI phase picked up in the first quarter or provided a short-term trading window; choosing a line to find flexibility in combination with capacity supply.

Judging from the 2026 outlook for the global market, the US credit cycle may gradually recover or even “overheat” under certain conditions. In short, dismantling the three parts of the credit cycle: 1) As mentioned earlier, the AI industry trend may continue; 2) fiscal expansion, which gradually improves after the “Big Beauty” Act. The annual expenditure of 340 billion US dollars is equivalent to 1% of GDP. We estimate that the deficit rate will rise from 5.9% to 6.4%, and if tariffs are excluded, it will rise to 7.5%; the increase comes from investment commitments of up to 5 trillion US dollars in tariff agreements, with an average distribution of close to 1 trillion US dollars in 2026; 3) traditional demand has improved slightly, and has continued to be sluggish since the 2022 interest rate hike cycle of the Federal Reserve, and more so Because Costs are too high rather than insufficient, so it is expected that interest rates will gradually recover after interest rate cuts, although the magnitude is limited by the magnitude and pace of interest rate cuts. In summary, in an environment where fiscal and monetary “double easing” and technology investment continues, the credit cycle is upward (Chart 15).

Chart 15: The overall direction of the US credit cycle is improving next year

Source: Haver, CICC Research Division

The restarting US credit cycle may lead to a recovery in the global manufacturing cycle, leading to increased performance in both the export sector (such as machinery, chemicals, and even household goods) and the globally priced commodity sector (such as color, etc.). First, on the broad fiscal side, if the “Big Beauty” Act and investment expenses promised by other countries are implemented, US real investment may increase demand in related sectors; second, in terms of traditional demand, the Federal Reserve's interest rate cuts may cause the traditional manufacturing industry and US real estate cycles to rise steadily. The above two pieces of US demand may drive the recovery of the global manufacturing cycle, so that the corresponding Chinese assets benefit from direct exports to the US, or indirect exports to other countries (such as excavators exported to African mines, etc.), or global pricing mapping.

When to choose, you can look at manufacturing PMI and existing housing sales. In addition, the domestic PPI phase is picking up or providing a short-term trading window. The focus is on observing US fiscal strength in the first quarter and the pace of interest rate cuts by the Federal Reserve. The corresponding data verifies that the foothold is the US manufacturing PMI and existing housing sales. Furthermore, we expect China's PPI to rise in stages from the end of this year to the first and second quarter of next year (Chart 16), which can also guide investors to trade in stages and switch to industries with certain “pro-cyclical” attributes in this sector.

Chart 16: Domestic PPI is likely to continue to repair the trend in the first and second quarter of next year

Source: Wind, CICC Research Division

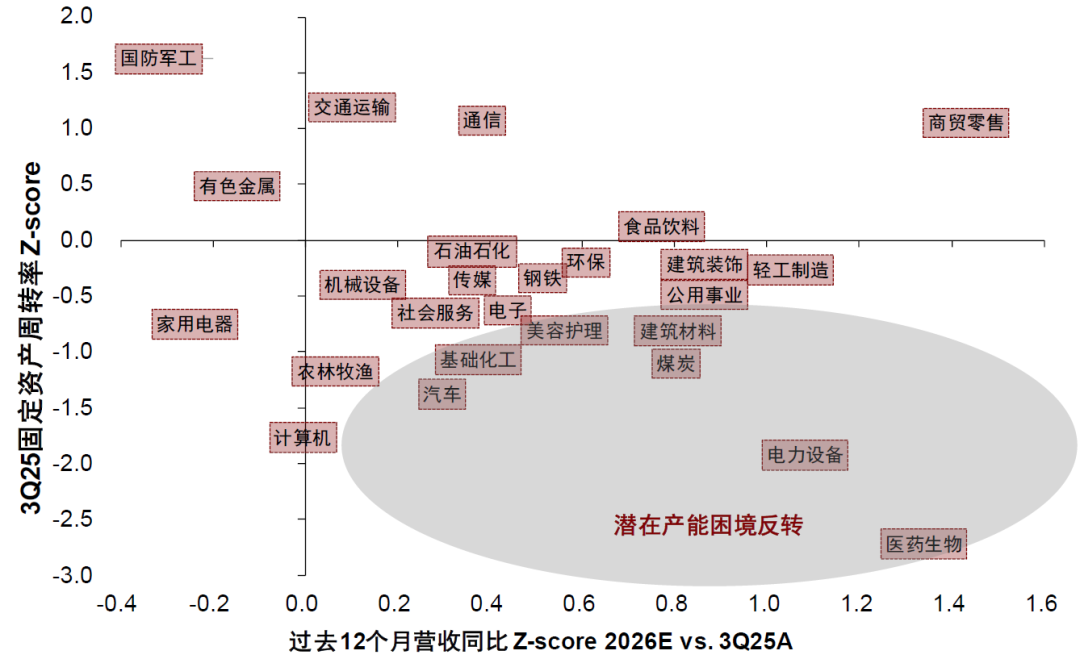

Line selection can be combined with capacity supply to find a more flexible direction. Although it is difficult to completely reverse the production capacity cycle next year, clues such as PPI may indicate that there are stages of stabilization in the production capacity cycle, which also means that some industries may have structural clues that production capacity will clear up (Chart 17). Referring to the annual outlook, combined with demand, turnover and valuation, the main industries in the external demand sector that have clear production capacity are electricity chains, chemicals, household goods, etc. If external demand is fulfilled as scheduled next year, these sectors may have better performance expectations and market performance flexibility.

Chart 17: Some industries may have clues that production capacity has been cleared

Note: Z-score is calculated using sample data from 1q11 to 3q25, using Shenwan's first-level industry classification. The financial data is based on the calculation of the 800 constituent stocks of China Securities, and the data is on a rolling basis for the past 12 months; Source: Wind, CICC Research Department

The downside is that opportunities are not sustainable enough on a year-round basis. First, the pace of the year-on-year restoration of domestic PPI determines that the PPI and external demand drive double “logical resonance” period is limited. After that, if PPI repair enters a “rest period”, it may be counterbalanced with external demand logic. At this time, if the relevant sectors want to continue excessive profits, they must rely on external demand to be “highly elastic”; second, the “high elasticity” period driven by external demand also has time constraints. More likely, the window period may be within the Federal Reserve interest rate cut cycle in the first half of the year.

Traditional domestic demand: The advantage is that valuations and expectations are not high; the disadvantage is that profit support is lacking; there may be potential swing trading opportunities under policy catalysts, but beware of “static valuation traps.”

The current advantage of traditional demand sectors represented by pan-consumption and real estate chains is that apparent valuations are cheap. Apart from some new consumer products, the market's valuation and expectations for them are not high. Therefore, if there is some policy catalyst, when valuations and expectations are at a lower level in a historically comparable range, the traditional domestic demand sector will not rule out certain trading opportunities.

The downside, however, is the lack of profit support, and its macroscopic internal logic has been explained in previous judgments on domestic credit cycles. Therefore, for this type of product, “simply cheap” is not a reason to buy; under the condition that the three logics of “cheap enough”, not “cheaper” in the short term, and an upward catalytic window exist at the same time, investors can have the possibility of having limited odds space during the position game stage.

Dividends: Essentially, they are hedging against “weak domestic demand”. The dividend rate of Hong Kong stocks is still attractive, but the optional range is shrinking.

Essentially, allocating dividend assets is essentially due to poor domestic demand: First, high dividends, as stable “cash” return assets to cope with poor credit expansion and declining overall returns, still have allocation value. Second, at present, the static dividend rate of the Hang Seng High Dividend Index is still around 5.8%; considering that the yield on 10-year Chinese treasury bonds is still at the top of the 1.8%-1.9% level, and the volatility of the bond market has increased since this year, dividend assets still have allocation value for absolute income capital, starting with insurance capital.

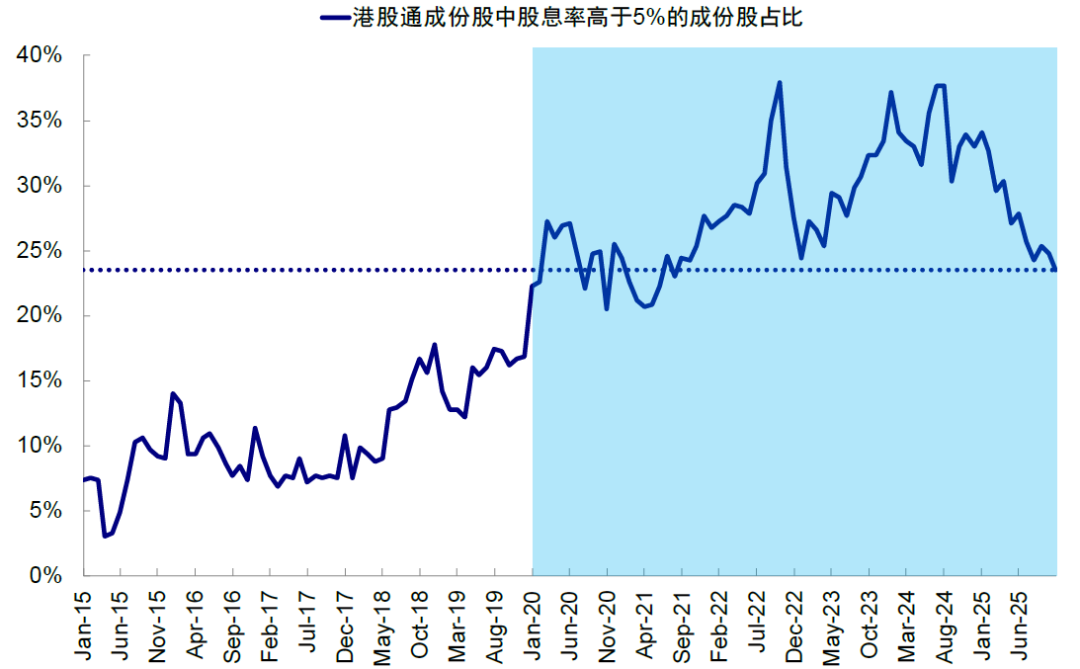

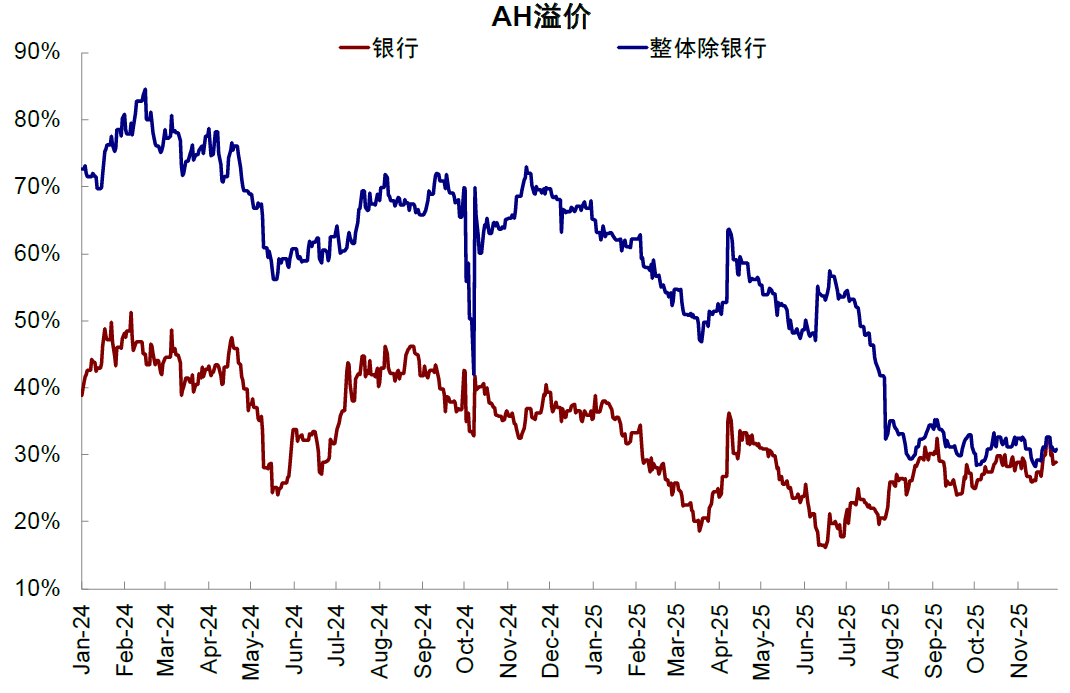

However, it is also important to note: First, along with the overall rise in the valuation level of dividend assets in recent years, there has been a “contraction” in the scope of “dividend assets.” As of November 2025, the share of targets with static dividend rates above 5% within the Hong Kong Stock Connect range was less than 1/4, which is in the 15% quantile since 2020 (Chart 18). Second, the AH premium shows that the ratio of Hong Kong stock dividends to A shares is not significant enough. Our weighted AH premium data calculated from the bottom up shows that currently the AH premium for both local listings and the banking sector is basically 130%, while considering the “top” of the reasonable AH premium after dividend tax is about 125%, there are not many relative valuation discounts provided (Chart 19).

Chart 18: Recently, there has been a “contraction” in the breadth of high-dividend assets

Source: Wind, CICC Research Division

Chart 19: The AH premium indicates that the current relative valuation discount level of Hong Kong stock dividend assets is not high

Source: Wind, CICC Research Division