Undervalued Asian Small Caps With Insider Action In November 2025

As Asian markets navigate a landscape marked by technological innovation and economic shifts, small-cap stocks have been capturing investor attention with their potential for growth amid broader market optimism. In this context, identifying promising small-cap opportunities often involves looking at companies with strong fundamentals and strategic insider activity, which can signal confidence in their future prospects.

Top 10 Undervalued Small Caps With Insider Buying In Asia

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| Security Bank | 4.4x | 1.0x | 26.99% | ★★★★★★ |

| East West Banking | 3.1x | 0.7x | 20.41% | ★★★★★☆ |

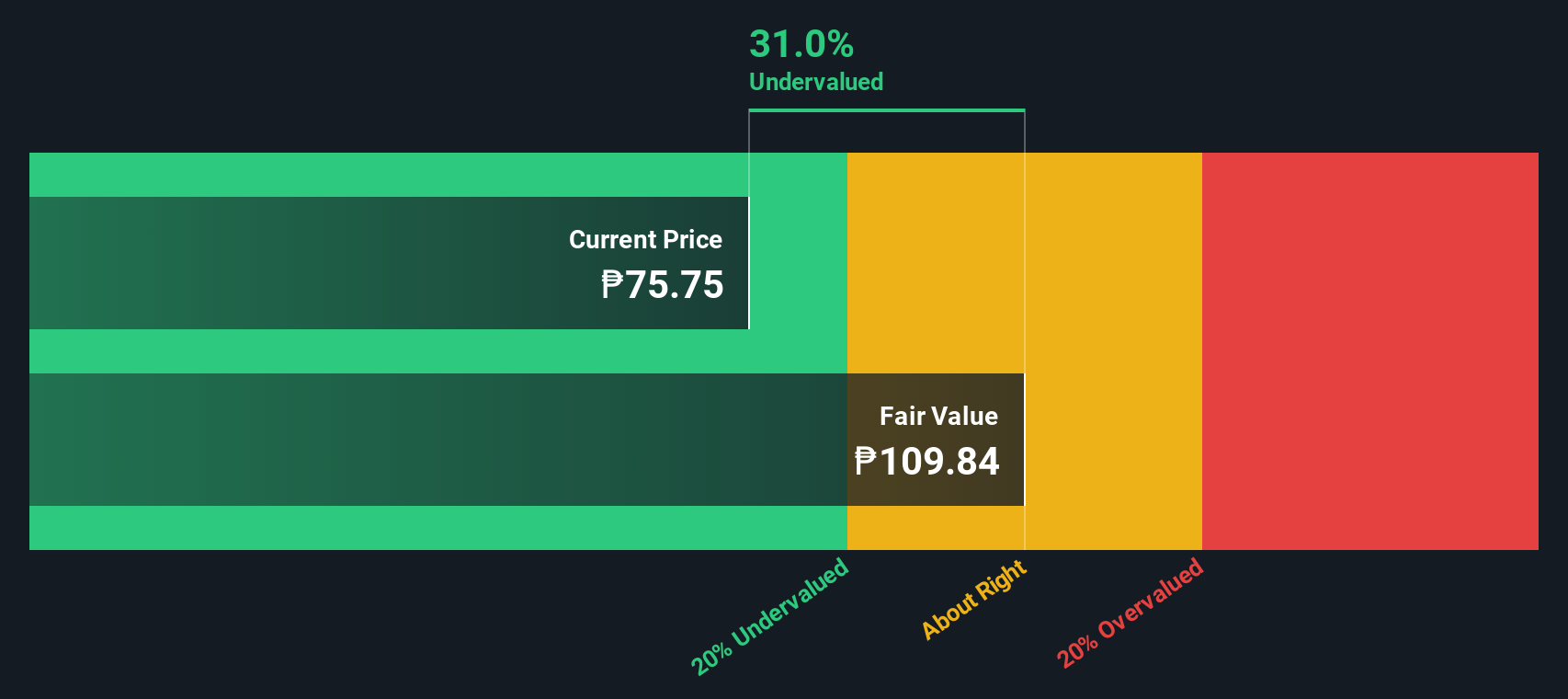

| Clover | 20.2x | 1.7x | 30.05% | ★★★★☆☆ |

| Centurion | 3.8x | 3.2x | -59.96% | ★★★★☆☆ |

| Chinasoft International | 21.9x | 0.7x | -1211.16% | ★★★★☆☆ |

| Hung Hing Printing Group | NA | 0.4x | 44.57% | ★★★★☆☆ |

| Dicker Data | 23.4x | 0.8x | -52.44% | ★★★☆☆☆ |

| Superloop | 1197.3x | 2.6x | 47.54% | ★★★☆☆☆ |

| Ever Sunshine Services Group | 6.6x | 0.4x | -440.01% | ★★★☆☆☆ |

| PSC | 9.9x | 0.4x | 18.94% | ★★★☆☆☆ |

We're going to check out a few of the best picks from our screener tool.

Dicker Data (ASX:DDR)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Dicker Data is an Australian wholesale distributor specializing in computer peripherals, with a market capitalization of A$1.89 billion.

Operations: The company generates revenue primarily through wholesale sales of computer peripherals. Over recent periods, the gross profit margin has shown an upward trend, reaching 14.01% by mid-2025. Operating expenses have steadily increased alongside revenue growth, impacting net income margins, which stood at 3.39% in mid-2025.

PE: 23.4x

Dicker Data, a tech distributor in Asia, stands out with insider confidence as Vladimir Mitnovetski recently purchased 25,000 shares for A$217,950. The company is navigating high debt levels but anticipates an 8.62% annual earnings growth. Despite relying solely on external borrowing for funding, Dicker Data maintains its dividend payouts with a recent affirmation of A$0.11 per share for Q3 2025. Investors may find interest in its potential growth trajectory amidst these financial dynamics.

- Click to explore a detailed breakdown of our findings in Dicker Data's valuation report.

Explore historical data to track Dicker Data's performance over time in our Past section.

Investore Property (NZSE:IPL)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Investore Property focuses on owning and managing large format retail properties, with a market capitalization of NZ$0.63 billion.

Operations: The primary revenue stream is derived from large format retail properties, generating NZ$76.72 million. The cost of goods sold (COGS) amounts to NZ$19.27 million, resulting in a gross profit of NZ$57.46 million and a gross profit margin of 74.89%. Operating expenses are recorded at NZ$2.61 million, while non-operating expenses stand at NZ$13.37 million, impacting the net income which is reported at NZ$41.47 million with a net income margin of 54.06%.

PE: 11.0x

Investore Property, a small-cap company in Asia, presents an intriguing opportunity with its recent financial performance. For the half year ending September 2025, sales reached NZ$38.86 million and net income climbed to NZ$12.79 million from NZ$9.66 million the previous year, showcasing growth despite reliance on external borrowing for funding. Insider confidence is evident with share purchases over the past months, suggesting potential value recognition within the company. Earnings are projected to grow annually by 5.69%, hinting at future prospects amidst current challenges like high-risk funding sources and one-off items impacting results.

- Delve into the full analysis valuation report here for a deeper understanding of Investore Property.

Assess Investore Property's past performance with our detailed historical performance reports.

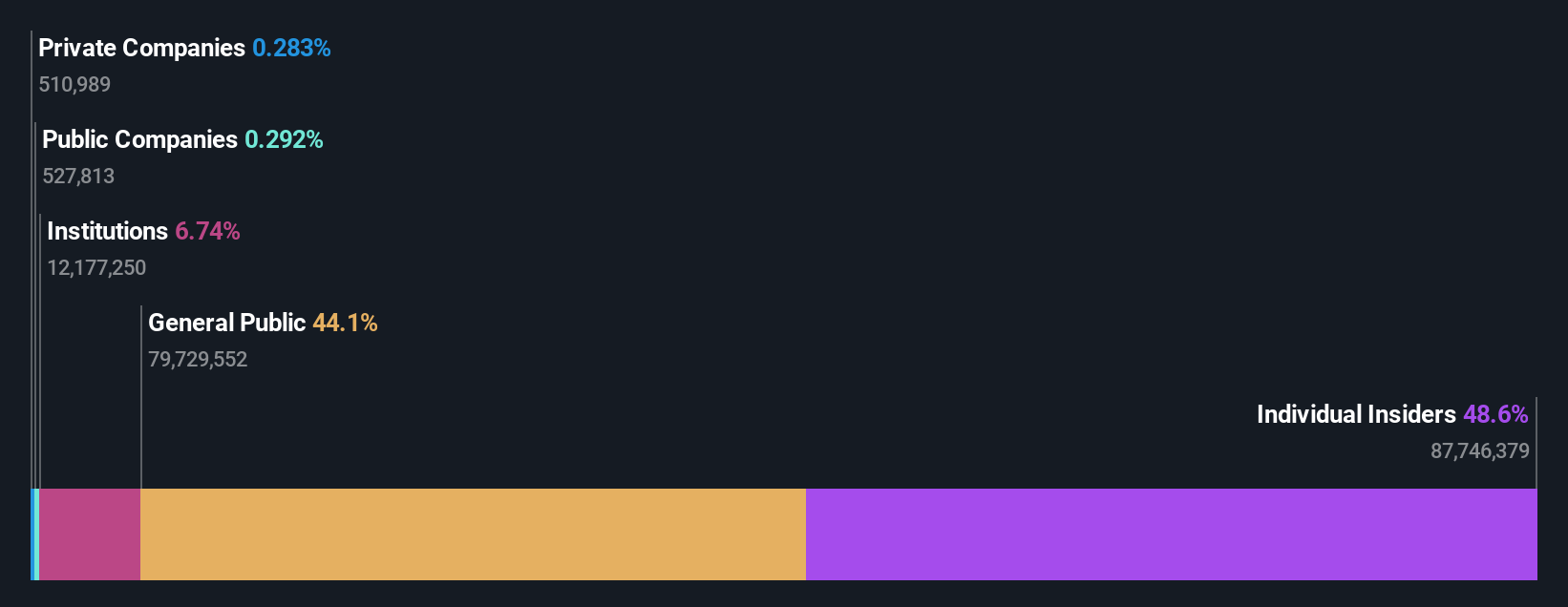

Security Bank (PSE:SECB)

Simply Wall St Value Rating: ★★★★★★

Overview: Security Bank is a financial institution offering a range of services including retail banking, business banking, financial markets, and wholesale banking with operations contributing to its market capitalization of ₱88.13 billion.

Operations: Security Bank generates revenue primarily from Retail Banking and Wholesale Banking, with significant contributions also from Business Banking and Financial Markets. The company has seen fluctuations in its net income margin, which was 44.89% as of December 2014 and decreased to 22.13% by September 2025. Operating expenses are a major component of costs, consistently surpassing ₱30 billion in recent periods.

PE: 4.4x

Security Bank, a smaller player in the Asian financial sector, has shown promising signs of being undervalued. Recent earnings for Q3 2025 highlight a net interest income of PHP 12.88 billion and net income of PHP 3.21 billion, both increases from last year. The bank's leadership transition to Victor Lee Meng Teck in January 2026 could drive strategic growth, given his successful track record at CIMB Singapore. Insider confidence is evident with recent share purchases, suggesting optimism about future performance despite challenges like a high bad loans ratio of 2.9%.

- Dive into the specifics of Security Bank here with our thorough valuation report.

Gain insights into Security Bank's historical performance by reviewing our past performance report.

Next Steps

- Embark on your investment journey to our 47 Undervalued Asian Small Caps With Insider Buying selection here.

- Have you diversified into these companies? Leverage the power of Simply Wall St's portfolio to keep a close eye on market movements affecting your investments.

- Elevate your portfolio with Simply Wall St, the ultimate app for investors seeking global market coverage.

Searching for a Fresh Perspective?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com