Why GDS Holdings (GDS) Is Up 9.9% After Return to Profit and Reaffirmed 2025 Guidance

- GDS Holdings Limited recently reported third quarter 2025 results, showing revenue of ¥2,887.13 million and net income of ¥725.98 million, reversing a net loss in the prior year period; the company also confirmed its full-year revenue guidance for 2025.

- The return to profitability and maintenance of guidance highlight renewed management confidence and a significant year-over-year turnaround in financial performance.

- We'll examine how the company's shift to net profit and reiterated guidance for 2025 impacts its overall investment narrative and risk profile.

The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 25 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

GDS Holdings Investment Narrative Recap

To be a shareholder in GDS Holdings, you need to believe in the company’s ability to capture sustained demand for digital infrastructure, particularly data centers serving AI and cloud computing in China and across Asia. While the recent return to profitability and confirmation of revenue guidance mark a clear positive, the biggest short-term catalyst, AI-driven data center demand, remains closely tied to improved chip supply, and the greatest risk continues to be declining average monthly service revenue (MSR) and pressure on margins; this news event does not materially resolve either issue in the short term.

Among the recent company developments, the repeated confirmation of 2025 revenue guidance is most relevant to the earnings announcement. It suggests management’s continued expectation of growth despite sector headwinds, but investors should remain focused on trends in contract pricing and ongoing shifts in business mix, as these will be crucial to future profitability beyond the current earnings rebound.

In contrast, while today’s results might seem to ease near-term concerns, investors should be aware that risks tied to high leverage and frequent asset sales may...

Read the full narrative on GDS Holdings (it's free!)

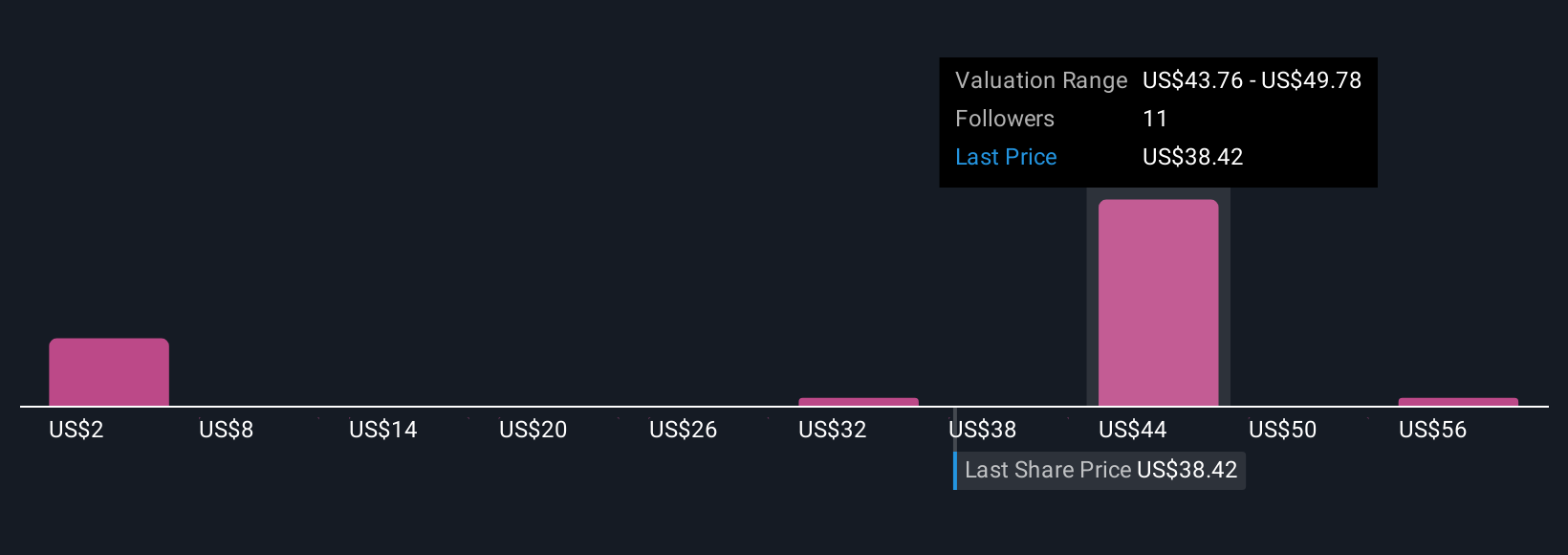

GDS Holdings' narrative projects CN¥16.2 billion revenue and CN¥734.2 million earnings by 2028. This requires 14.1% yearly revenue growth and a CN¥457 million earnings increase from the current CN¥277.2 million.

Uncover how GDS Holdings' forecasts yield a $48.21 fair value, a 42% upside to its current price.

Exploring Other Perspectives

Community fair value estimates for GDS range widely, from CN¥5.80 to CN¥61.83, with five perspectives represented in the Simply Wall St Community. This variety reflects how current optimism about AI-driven demand is still weighed against the risk of pressure on service revenue; your outlook could be quite different depending on which factors matter most to you.

Explore 5 other fair value estimates on GDS Holdings - why the stock might be worth as much as 82% more than the current price!

Build Your Own GDS Holdings Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your GDS Holdings research is our analysis highlighting 2 key rewards and 3 important warning signs that could impact your investment decision.

- Our free GDS Holdings research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate GDS Holdings' overall financial health at a glance.

No Opportunity In GDS Holdings?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- This technology could replace computers: discover 28 stocks that are working to make quantum computing a reality.

- These 13 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- Trump's oil boom is here - pipelines are primed to profit. Discover the 22 US stocks riding the wave.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com