- PREMIUM

- LIVE QUOTES

- INSTITUTION

Index Options

Index Options State Street

State Street CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street JournalDoximity’s Raised Revenue Guidance and Analyst Optimism Might Change the Case for Investing in DOCS

- Earlier this week, Doximity reported its fiscal Q2 2026 results, highlighting a 23% year-over-year revenue increase and strong EBITDA growth, while also raising its revenue forecast to a range of US$640 million to US$646 million.

- An upswing in analyst sentiment and supportive FDA reforms have reinforced the company’s growing significance in the healthcare professional platform space.

- We'll explore how Doximity’s raised revenue guidance may influence its long-term earnings outlook and market positioning.

Trump's oil boom is here - pipelines are primed to profit. Discover the 22 US stocks riding the wave.

Doximity Investment Narrative Recap

To be a shareholder in Doximity, you need to believe in its ability to entrench itself as an essential productivity platform for US clinicians, monetizing a leading network of healthcare professionals while expanding into AI-powered tools and services. The recent revenue beat and raised fiscal guidance reaffirm broad-based engagement and demand but do not materially change the most pressing risk: the company’s heavy reliance on pharmaceutical marketing spend, which remains exposed to regulatory and budget shifts in the sector. Among the company’s recent announcements, its Q2 2026 earnings results, showing strong revenue and net income growth, stand out as most relevant. Sustained top-line gains further support the thesis that demand for Doximity’s digital tools among health systems and pharma clients is resilient, and the momentum behind increased revenue guidance should reinforce the upcoming quarters as a period of continued platform expansion and commercial traction. On the other hand, investors should be aware that despite this momentum, Doximity’s reliance on pharma budgets means that even favorable results...

Read the full narrative on Doximity (it's free!)

Doximity's narrative projects $805.8 million revenue and $280.5 million earnings by 2028. This requires 11.0% yearly revenue growth and a $45.4 million earnings increase from $235.1 million.

Uncover how Doximity's forecasts yield a $71.11 fair value, a 40% upside to its current price.

Exploring Other Perspectives

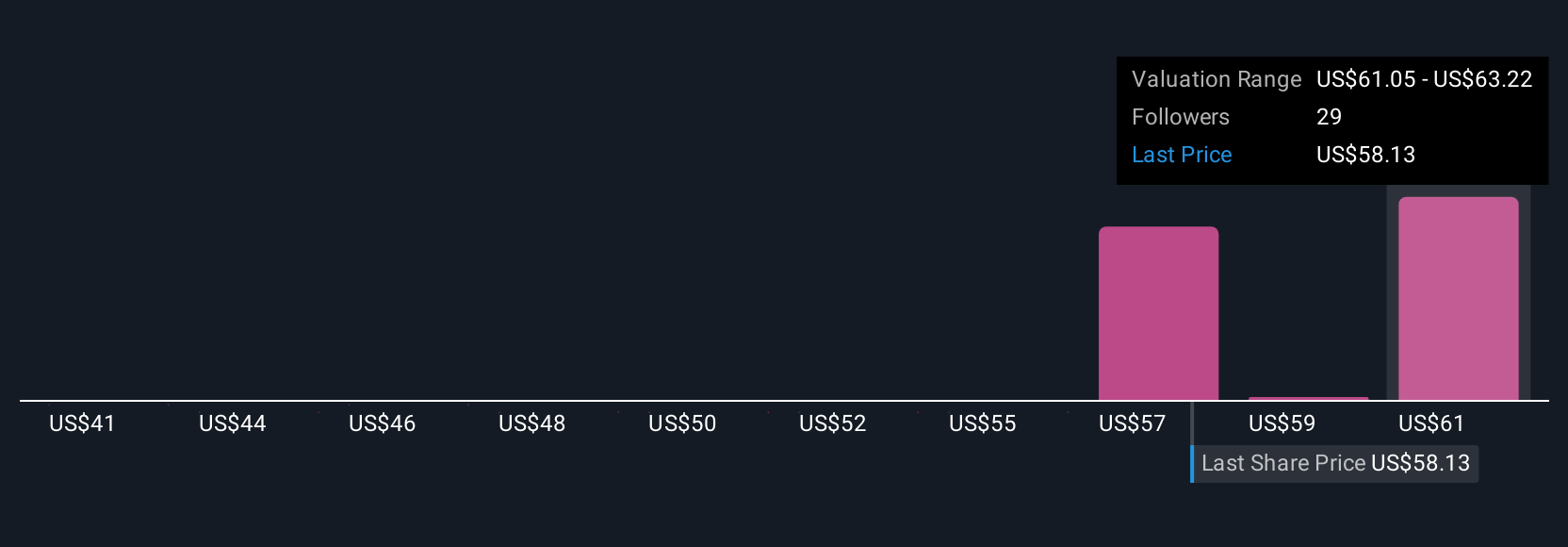

Eight members of the Simply Wall St Community valued Doximity between US$32.58 and US$78.58 per share, reflecting varied outlooks. Keep in mind, ongoing policy uncertainty around pharmaceutical marketing spend could shape how Doximity delivers consistent earnings over the next year.

Explore 8 other fair value estimates on Doximity - why the stock might be worth 36% less than the current price!

Build Your Own Doximity Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Doximity research is our analysis highlighting 4 key rewards that could impact your investment decision.

- Our free Doximity research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Doximity's overall financial health at a glance.

Seeking Other Investments?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 35 best rare earth metal stocks of the very few that mine this essential strategic resource.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 25 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com