Is Wingstop’s 12% Weekly Surge Justified After Expansion and Menu News?

- Curious if Wingstop is still serving up value, or whether investors are biting off more than they can chew? You are not alone. Plenty of savvy market watchers are looking for answers as the stock draws attention.

- Wingstop just popped 11.8% in the last week, a sharp change from its 1.6% gain over the past month and a notable -21.5% return over the past year, hinting at both fresh optimism and past volatility.

- Much of this action comes amid broader food and hospitality sector chatter, with analysts and commentators debating the resilience of "fast-casual" brands. Recent headlines focus on expansion plans and menu innovation, fueling speculation about future growth.

- For the number crunchers among us, Wingstop currently scores a 2/6 on undervaluation checks. This suggests there is more to the valuation story than just the headlines or price moves. Let's break down the classic ways investors dissect value, and then take a look at whether the stock could fit into a broader investment strategy.

Wingstop scores just 2/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: Wingstop Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow (DCF) model estimates a company's intrinsic value by projecting its future cash flows and then discounting those amounts back to the present. This process helps investors determine what a business is truly worth today, based on expected performance in the years ahead.

For Wingstop, the DCF analysis uses the 2 Stage Free Cash Flow to Equity approach. Wingstop's latest reported Free Cash Flow is $54.7 million. Looking forward, analysts estimate this figure will continue to grow, with projections reaching $287.2 million by 2029. After that, additional growth is extrapolated out to 2035 as shown by Simply Wall St's extended forecasts. All cash flows are measured in US dollars.

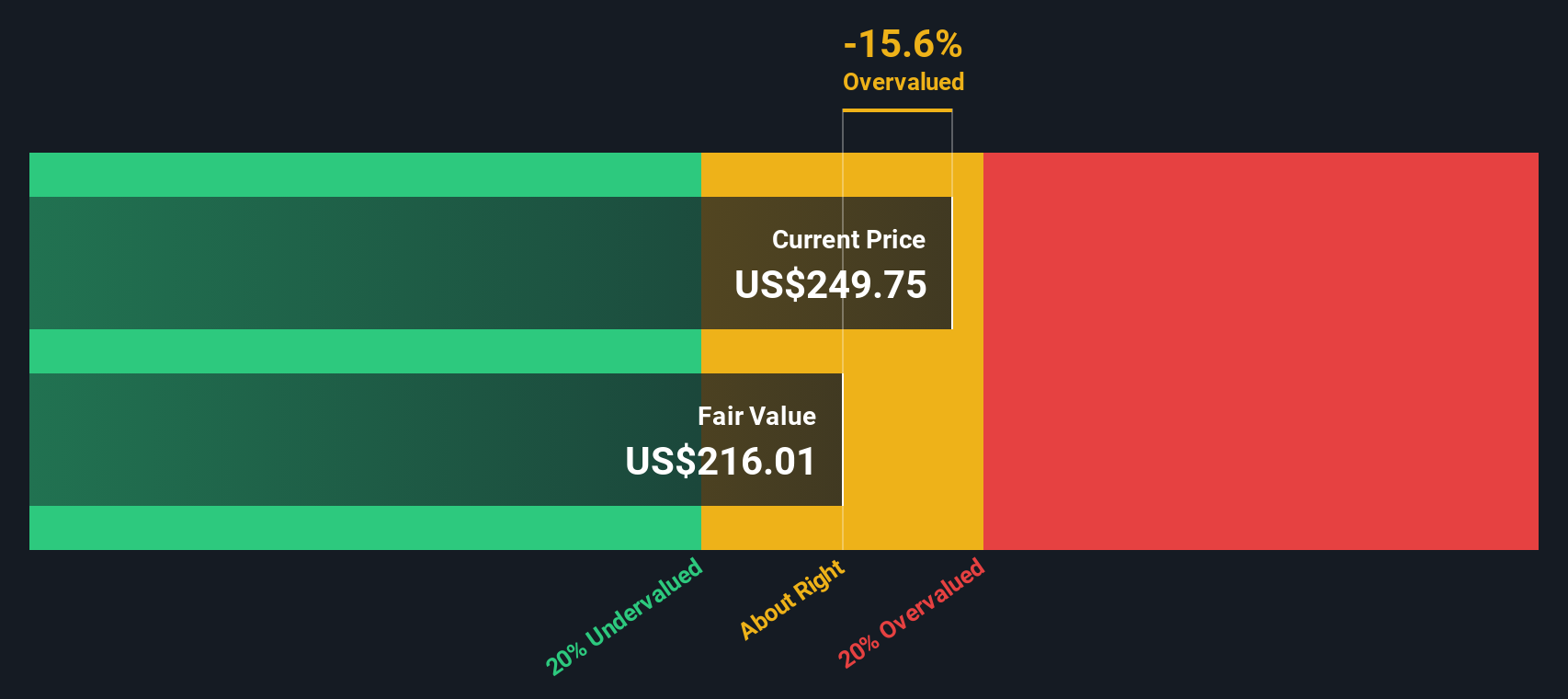

When these projections are processed through the DCF model, they yield an estimated intrinsic value of $219.91 per share. Compared to the current share price, this suggests Wingstop is trading at a 17.8% premium, which means the stock is more expensive than its projected future earnings would justify under this model.

Result: OVERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Wingstop may be overvalued by 17.8%. Discover 928 undervalued stocks or create your own screener to find better value opportunities.

Approach 2: Wingstop Price vs Earnings (PE)

The Price-to-Earnings (PE) ratio is one of the most reliable ways to value profitable companies like Wingstop. This multiple helps investors gauge what they are paying for each dollar of earnings. It is especially useful when companies have consistent profits and visibility into future growth.

What counts as a “fair” PE ratio depends on two key factors: the company’s expected future growth and the level of risk attached to its business. Fast-growing companies or those perceived as lower risk typically command higher PE ratios. Slow growth or higher risk usually means a lower PE is justified.

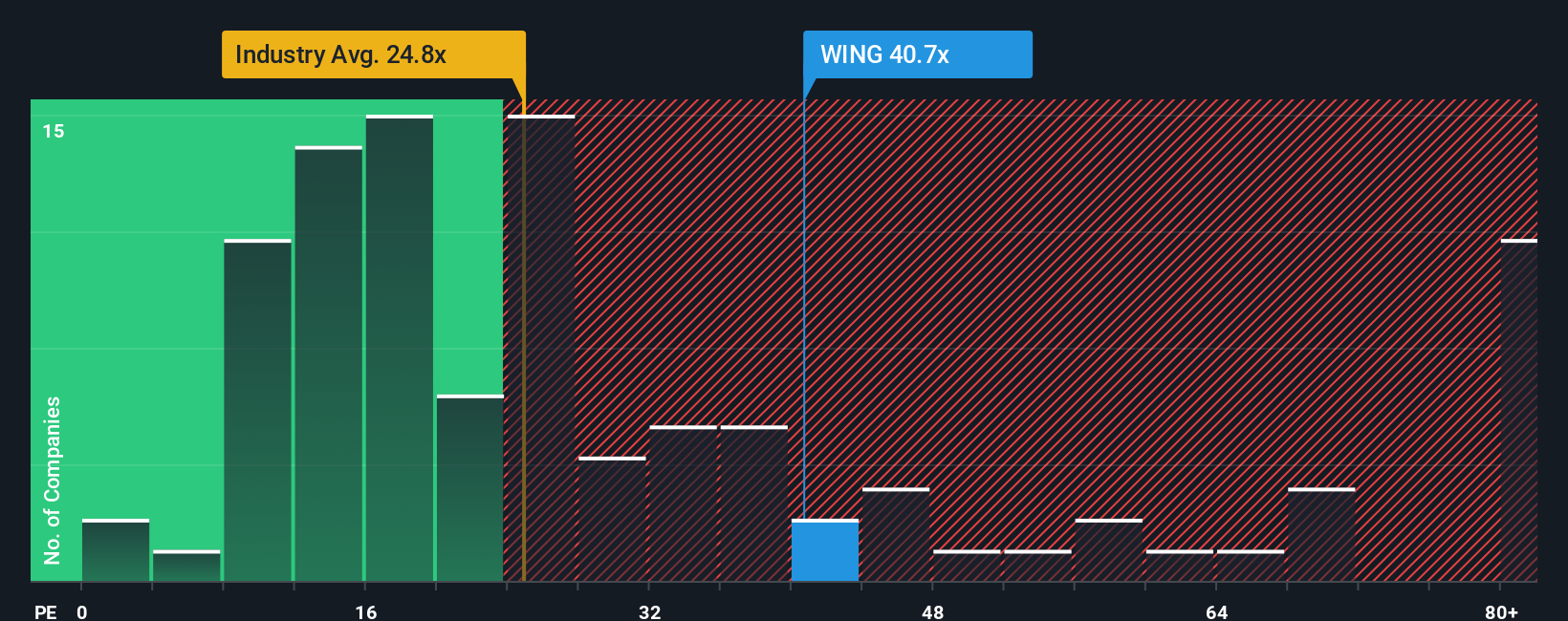

Wingstop is currently trading at a PE ratio of 41.3x. This stands well above the hospitality industry average of 21.4x and also above the peer group average of 65.0x. However, these benchmarks can be misleading if we do not account for specific company traits.

This is where the Simply Wall St “Fair Ratio” comes in handy. The Fair Ratio goes beyond simple averages, incorporating company-specific factors including earnings growth, risk profile, profit margins, industry positioning, and market capitalization. For Wingstop, the Fair Ratio is calculated to be 18.7x, which is a measure of the PE multiple the company could reasonably sustain given its financial and strategic profile.

Comparing Wingstop’s actual 41.3x to its Fair Ratio of 18.7x shows that the current stock price bakes in much higher expectations than what these fundamentals suggest.

Result: OVERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1440 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Wingstop Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let’s introduce you to Narratives. A Narrative is your personalized view of a company, the story behind the numbers, where you lay out what you expect for Wingstop’s future revenue, earnings, and profit margins, then connect that story to a financial forecast and a fair value estimate.

Unlike generic financial ratios, Narratives allow you to combine what you know (or believe) about the company with the actual data, giving context to valuation. It is a dynamic, easy-to-use tool on the Simply Wall St Community page, trusted by millions of investors. By creating or following Narratives, you can quickly compare the fair value calculated from your assumptions to the current stock price, helping you decide when to buy, hold, or sell.

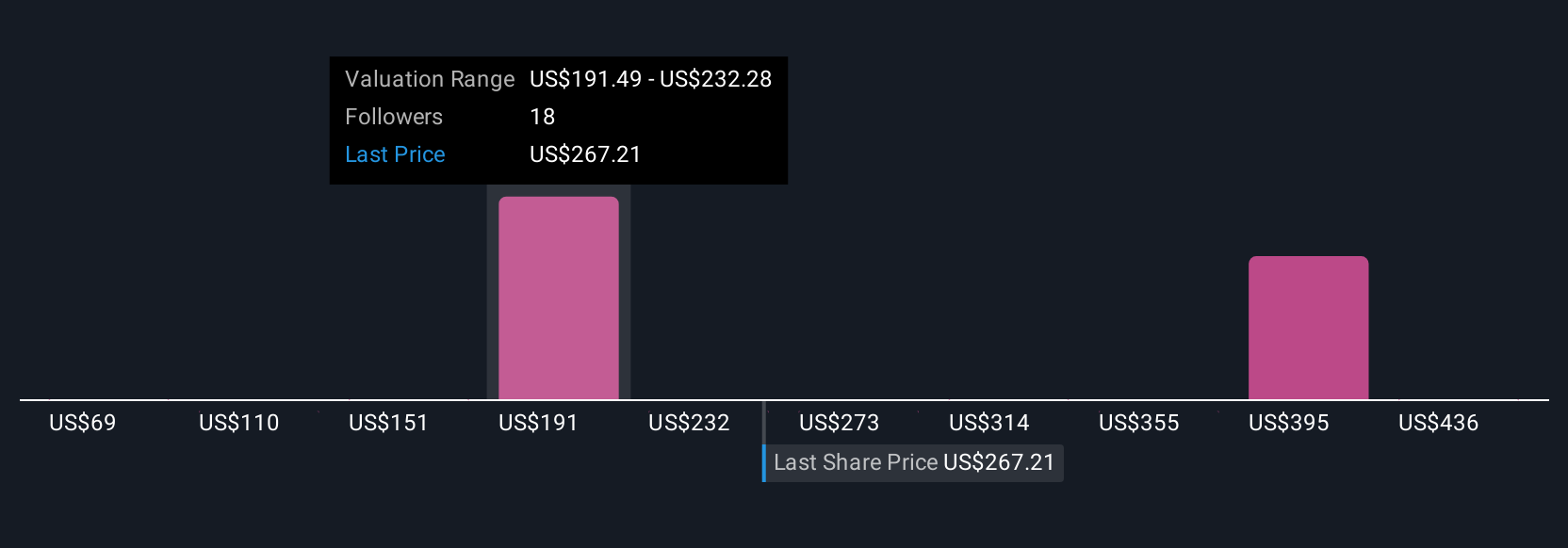

The real power is that Narratives update automatically whenever key news or earnings are released, keeping your view fresh. For example, some investors see Wingstop’s robust franchise expansion and digital innovation justifying price targets as high as $477. Others, worried about consumer demand and menu fatigue, set targets closer to $185. Narratives let you define and adjust your perspective, giving you total control over your investment story.

Do you think there's more to the story for Wingstop? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com