Examining Honda Stock Value After Recent Electric Vehicle Technology Collaboration

- Curious about whether Honda Motor stock is really a bargain right now? You are not alone. Let's break down what savvy investors are seeing and what it means for potential returns.

- After climbing 25.2% over the past year and gaining an impressive 2.7% in just the past week, the stock has caught the attention of both growth-seekers and value hunters.

- Recent headlines highlight Honda’s increased collaboration in electric vehicle technology and expanded investment in sustainable mobility, which has encouraged optimism and some renewed buying. These moves help explain the latest momentum and reveal shifting sentiment about Honda’s long-term prospects.

- When it comes to valuation checks, Honda Motor scores a solid 4 out of 6, suggesting the company may be undervalued in several key areas. We will dig into the different ways to assess Honda’s value in this article. Stick around, as there’s a smarter approach to valuation analysis you will not want to miss at the end.

Find out why Honda Motor's 25.2% return over the last year is lagging behind its peers.

Approach 1: Honda Motor Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow (DCF) model projects a company’s estimated future cash flows and then discounts them back to today’s value to find an intrinsic estimate of the stock’s worth. For Honda Motor, this means looking at both its expected growth and its future potential to generate cash.

Based on recent data, Honda Motor’s latest twelve months (LTM) Free Cash Flow stands at a loss of ¥154.3 billion. Despite the currently negative cash flow, projections are optimistic. Analysts expect the company to shift gears, with free cash flow forecasted to reach ¥889.1 billion by the fiscal year ending March 2030. Financial analysts provide cash flow estimates for the next five years, after which Simply Wall St extrapolates growth for the subsequent period.

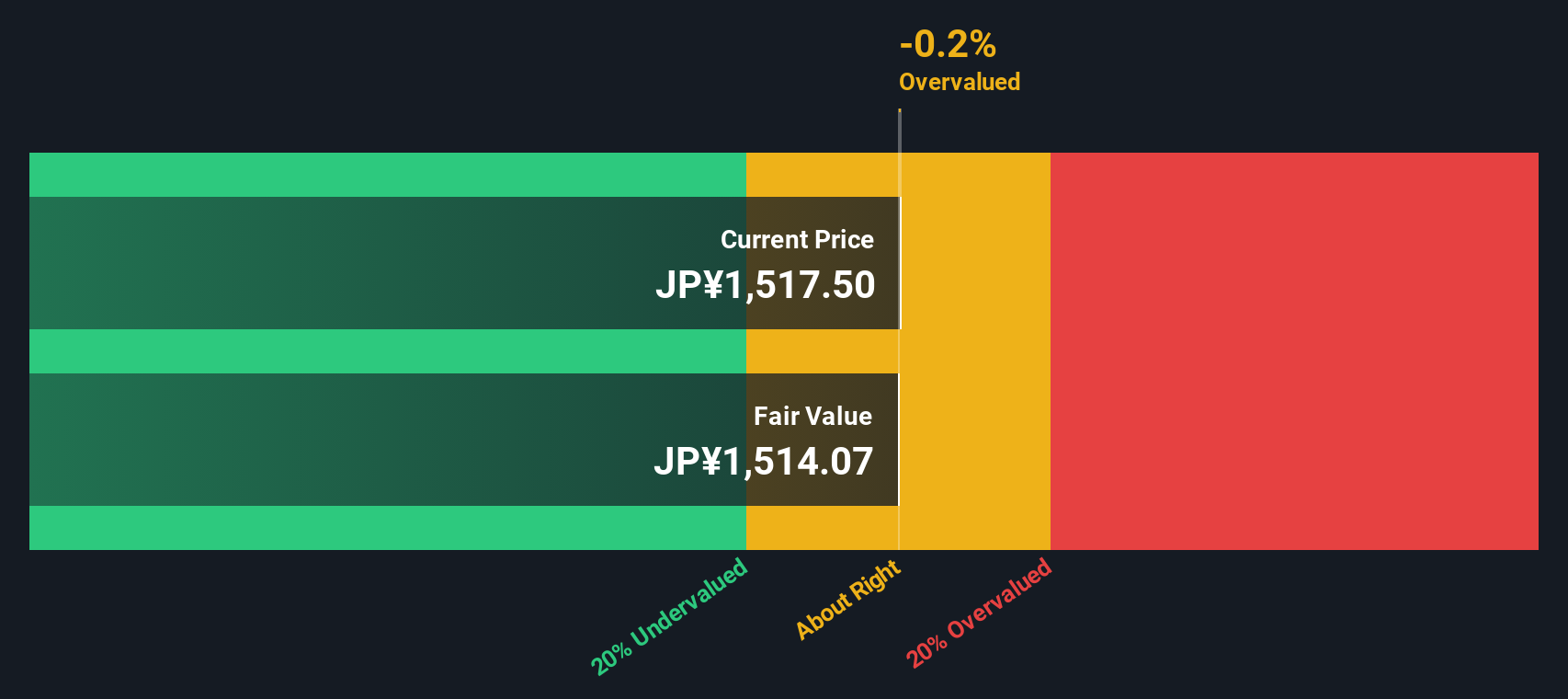

After tallying up these future cash flows and discounting them to present value, Honda Motor’s estimated intrinsic value is ¥1,845 per share. Compared to the current share price, this DCF analysis suggests the stock is trading at a 15.7% discount, which may indicate that the shares are undervalued at today’s levels.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Honda Motor is undervalued by 15.7%. Track this in your watchlist or portfolio, or discover 926 more undervalued stocks based on cash flows.

Approach 2: Honda Motor Price vs Earnings

The Price-to-Earnings (PE) ratio is a widely used valuation metric, especially for profitable companies like Honda Motor. It helps investors determine how much they are paying for each yen of earnings. PE is particularly useful for established firms where earnings are a key driver of value.

What makes a “normal” or “fair” PE ratio varies depending on growth expectations and the risks associated with a business. Fast-growing, stable companies often command higher PE ratios, while those with less certainty or lower prospects tend to trade at lower multiples.

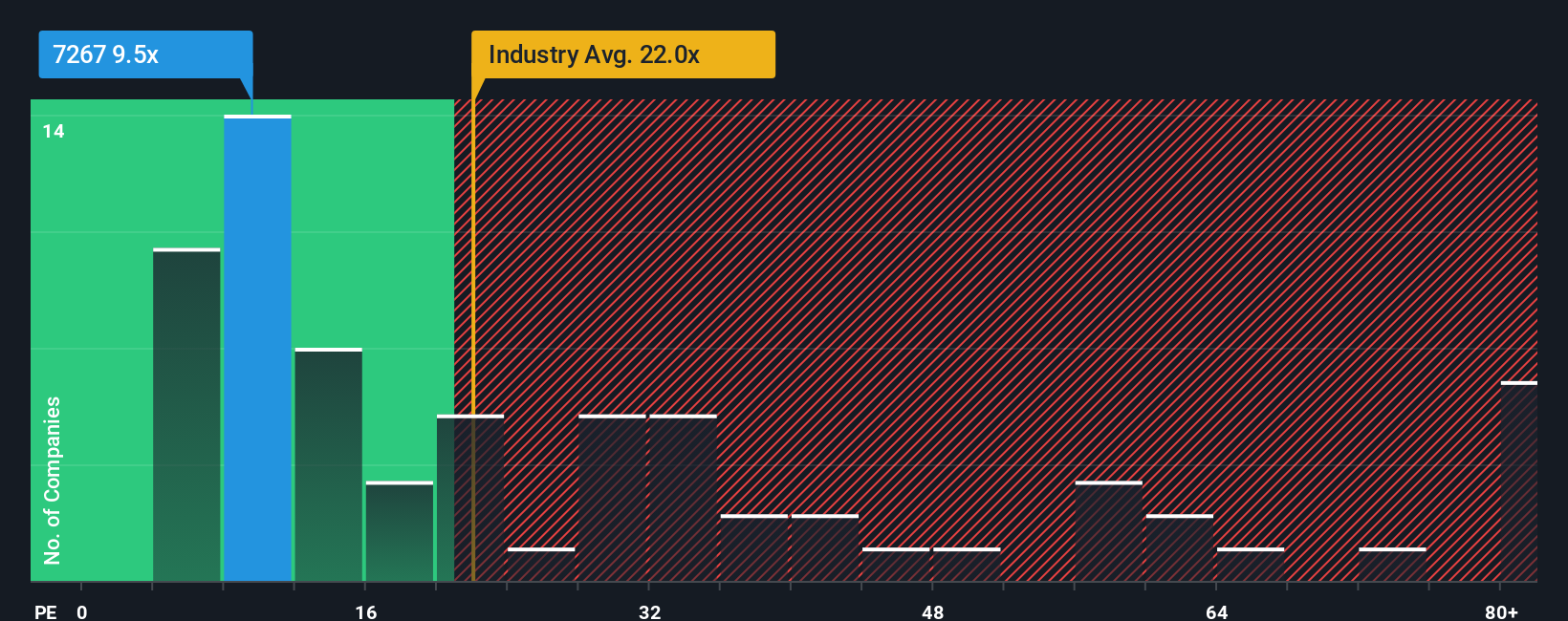

Honda Motor’s current PE ratio is 9.3x, which is notably lower than both its peer average of 10.5x and the auto industry average of 18.7x. This initially suggests Honda may be undervalued relative to its peers and industry. However, comparing PE ratios without considering a company's unique growth profile, risks, and profitability can be misleading.

Simply Wall St’s proprietary “Fair Ratio” metric addresses this gap. The Fair Ratio for Honda Motor is calculated at 17.9x, taking into account factors like future earnings growth, industry characteristics, profit margins, company size, and risk profile. This offers a more holistic benchmark than the simple peer or industry averages because it is tailored to Honda’s actual fundamentals and outlook.

With Honda’s actual PE of 9.3x sitting well below its Fair Ratio of 17.9x, this analysis points to the shares being undervalued at current prices.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1433 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Honda Motor Narrative

Earlier we mentioned that there is an even better way to understand valuation. Let us introduce you to Narratives. A Narrative is a powerful investment tool that allows you to connect your perspective on Honda Motor’s future with the financial numbers you expect, building a story that links real-world business changes to projected revenue, profit margins, and ultimately a fair value for the stock.

On Simply Wall St’s Community page, Narratives are easy to use and update. This helps millions of investors turn their outlook, whether optimistic or cautious, into a transparent, trackable valuation. Narratives make buying or selling decisions clearer by showing how your estimated Fair Value compares to the current share price, so you can act confidently when the numbers favor your strategy.

Because Narratives update automatically when major news or earnings are released, your outlook on Honda Motor is always grounded in the latest information, which reduces guesswork. For example, recent perspectives from investors range from bullish Narratives driven by strong motorcycle growth and technology partnerships (targeting ¥1,900 per share) to more cautious takes concerned about EV challenges and intense competition (targets as low as ¥1,400). This shows how flexible and personal your valuation journey can be.

Do you think there's more to the story for Honda Motor? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com