BlackRock (BLK): Evaluating Valuation After Recent Share Price Movement

BlackRock (BLK) recently saw mild movement in its stock price, gaining nearly 1% in the latest trading session. Investors are watching to gauge how the company’s valuation might compare to peers in the financial sector this month.

See our latest analysis for BlackRock.

Looking at the bigger picture, BlackRock’s share price has lost some momentum in recent months, with a 30-day return of -8.07 percent, but is still up 2.23 percent year-to-date. Despite this recent pullback, long-term holders have seen a 4.12 percent total shareholder return over the past year. The three-year and five-year total shareholder returns are 56.5 percent and 63.3 percent respectively. Overall, the short-term choppiness contrasts with its long-term record, suggesting that sentiment shifts could present fresh opportunities for investors as the market reassesses valuation and growth expectations.

If you’re curious to see which other financial names are showing growth potential and insider conviction, now’s a great time to explore fast growing stocks with high insider ownership

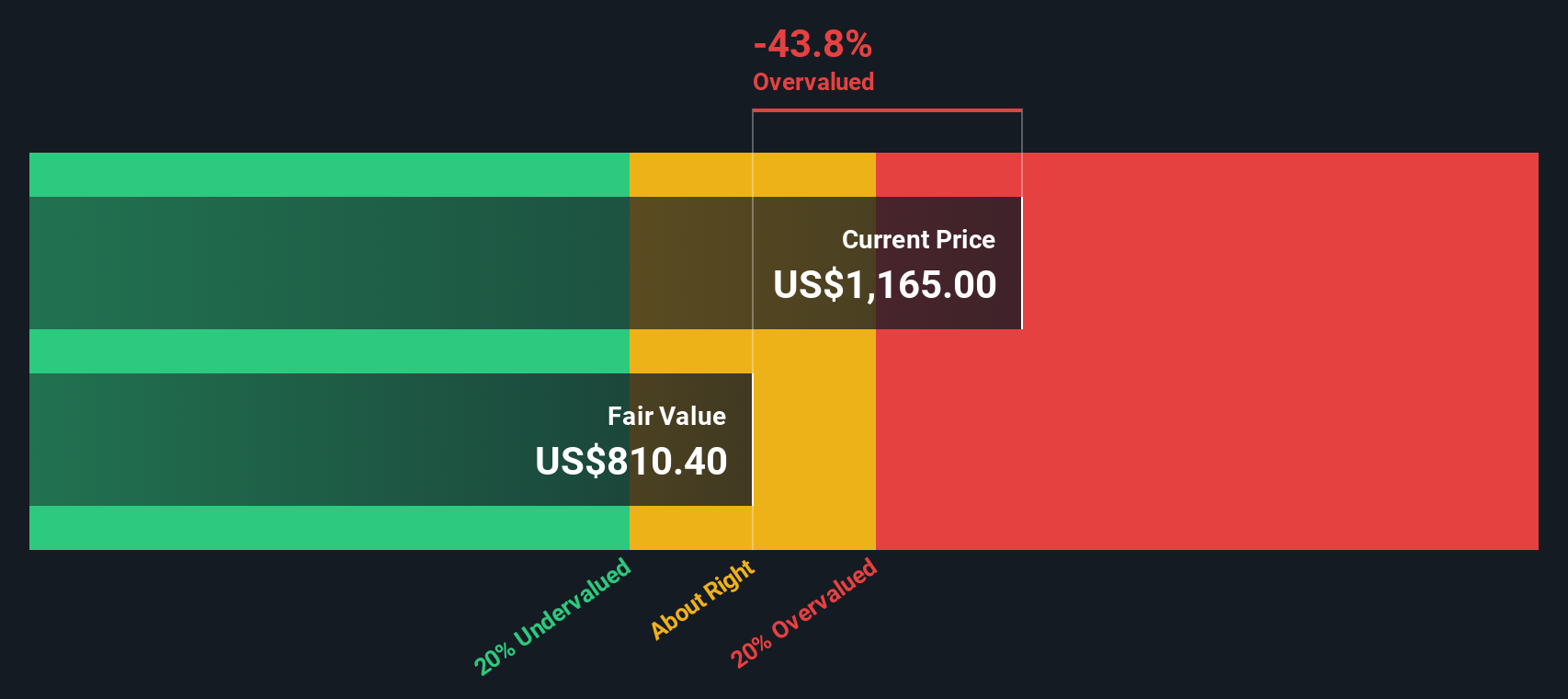

With BlackRock still trading well below analyst price targets despite solid revenue and net income growth, the question lingers: is this a buying opportunity for long-term investors, or has the market already priced in future gains?

Most Popular Narrative: 22.1% Undervalued

BlackRock’s widely followed narrative sets fair value at $1,334 per share, which is significantly higher than the last close of $1,040.06. This highlights a debate over market expectations versus narrative-driven targets.

BlackRock's expansion into private markets through acquisitions like HPS Investment Partners, GIP, and ElmTree positions the company to capitalize on the secular shift of institutional assets into alternatives and infrastructure, driving higher-fee revenue streams and long-term earnings growth.

Want to unlock the full story behind this ambitious narrative? It is based on aggressive top-line growth, ambitious margin improvements, and a profit outlook that rivals the industry’s leading companies. Learn what drives these projections. The architects of this narrative believe BlackRock could exceed expectations. Take a closer look before the market reacts.

Result: Fair Value of $1,334 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, ongoing integration risks and potential fee compression in both active and passive investing could challenge BlackRock’s ability to sustain its projected growth.

Find out about the key risks to this BlackRock narrative.

Another View: SWS DCF Model’s Take

Looking at BlackRock from the perspective of our SWS DCF model, the valuation picture shifts. The DCF suggests BlackRock is trading above its estimated fair value of $788.10. This may indicate that the market is assigning too much optimism to future cash flows. Does this highlight hidden risks for today’s investors, or is the market rightly favoring BlackRock’s growth story?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out BlackRock for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 926 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own BlackRock Narrative

If you see the story differently or want to follow your own analysis, you can craft a personal narrative in just a few minutes with Do it your way

A great starting point for your BlackRock research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

Looking for More Investment Ideas?

Take charge of your financial future and spot tomorrow’s top performers. There are exciting opportunities waiting that most investors still overlook. Don’t miss out on unique trends and sectors gaining strength now.

- Uncover market movers focused on AI and innovation by checking out these 25 AI penny stocks for stocks at the forefront of artificial intelligence advancements.

- Maximize stable income potential and secure attractive yields by reviewing these 15 dividend stocks with yields > 3%, a selection of companies prioritizing generous payouts.

- Get ahead of the mainstream and tap into the potential of blockchain technology and digital assets through these 81 cryptocurrency and blockchain stocks, featuring businesses with exposure to the future of finance.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com