Kuraray (TSE:3405): Assessing Valuation After Earnings Forecast Cut and Slowing Sales Outlook

Kuraray (TSE:3405) recently revised its full-year earnings forecast for 2025, citing lower than expected sales volumes in most divisions. The company attributes this adjustment to the impacts of US tariff policy and ongoing economic uncertainty.

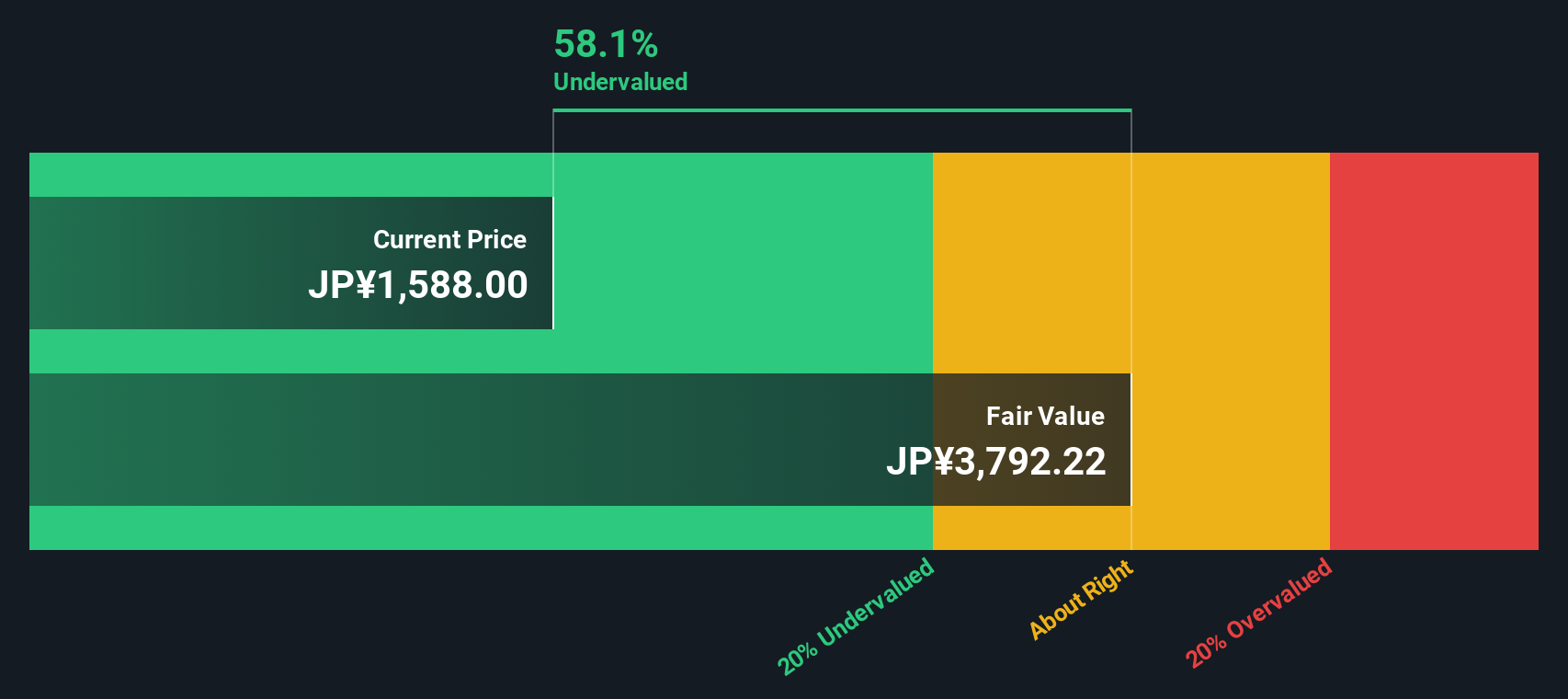

See our latest analysis for Kuraray.

After a sharp announcement lowering its earnings outlook, Kuraray’s share price has continued to slide, down 11.4% over the past month and now showing a year-to-date decline of more than 32%. While the recent buyback could offer some support, lackluster business momentum and economic uncertainty have clearly dented investor confidence. Even so, Kuraray’s longer-term total shareholder returns paint a more resilient picture, with 54% gains over the past three years and nearly 70% over five years, suggesting that patient investors have still come out ahead despite the recent volatility.

If today’s market swings have you thinking more broadly, this could be a timely moment to discover fast growing stocks with high insider ownership.

With shares now trading at a substantial discount to both analyst price targets and intrinsic value, the key question becomes whether Kuraray is fundamentally undervalued or if the market is accurately factoring in further headwinds and muted growth ahead.

Price-to-Earnings of 60.1x: Is it justified?

Kuraray’s shares are currently trading at a price-to-earnings ratio of 60.1x, which is sharply above both peer and industry averages. Despite a significant discount to fair value by other metrics, this high multiple suggests the market demands a premium for future profits, or that current profits are exceptionally depressed.

The price-to-earnings ratio compares the company’s share price to its per-share earnings, offering a sense of how much investors are willing to pay for each unit of bottom-line profit. In Kuraray’s case, a 60.1x ratio is typically seen when extraordinary growth is expected or near-term earnings have been hit by one-off items.

Compared to the JP Chemicals industry’s average price-to-earnings of just 12.1x and a “fair” ratio estimate of 25.4x, Kuraray’s current valuation looks highly stretched. If profitability recovers rapidly, this gap could narrow, but investors should be wary of overpaying if that rebound does not materialize.

Explore the SWS fair ratio for Kuraray

Result: Price-to-Earnings of 60.1x (OVERVALUED)

However, persistent economic uncertainty and slowing revenue growth could undermine any rapid recovery in Kuraray’s profitability or share price momentum in the near term.

Find out about the key risks to this Kuraray narrative.

Another View: Discounted Cash Flow Says Undervalued

While Kuraray’s sky-high price-to-earnings ratio paints a picture of overvaluation, our DCF model draws a strikingly different conclusion. According to this approach, shares are trading well below intrinsic fair value, which suggests a possible undervalued opportunity the market may be missing. Which story makes more sense for investors?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Kuraray for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 924 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Kuraray Narrative

If you’d rather rely on your own research or reach a different conclusion, you can quickly craft your own perspective from the available data in just a few minutes. Do it your way.

A great starting point for your Kuraray research is our analysis highlighting 2 key rewards and 3 important warning signs that could impact your investment decision.

Looking for More Smart Investment Moves?

Make your next portfolio decision count by checking fresh stock opportunities you might not have considered. Acting now could help you catch the next big outperformer while others are still watching from the sidelines.

- Benefit from stable passive income streams by reviewing these 14 dividend stocks with yields > 3% with yields above 3%.

- Seize the potential of revolutionary technology shifts with these 27 quantum computing stocks leading the way in computing innovation.

- Spot attractive bargains with these 924 undervalued stocks based on cash flows that the market may be underestimating based on strong cash flow analysis.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com