MasterBrand (MBC): Evaluating Valuation After Recent Share Price Volatility

See our latest analysis for MasterBrand.

Zooming out, MasterBrand’s share price has been on quite a ride lately, with a steep pullback over the past month followed by a quick bounce. The 1-week share price return sits at 16.5%, signifying a burst of momentum despite a disappointing 1-year total return of -36%. Investors are clearly re-evaluating the company's prospects as market sentiment shifts.

If the volatility around MasterBrand has you thinking bigger, now’s a smart time to broaden your search and discover fast growing stocks with high insider ownership

With shares trading well below their analyst price target, the big question is whether MasterBrand is genuinely undervalued right now or if the current price already reflects the company’s future outlook and growth prospects.

Price-to-Earnings of 16.9x: Is it justified?

MasterBrand's stock trades at a price-to-earnings (P/E) ratio of 16.9x, just below the US Building industry average of 17.3x. This means the market currently assigns almost the same value to MasterBrand's earnings as its closest industry peers.

The P/E ratio tells investors how much they are paying for each dollar of earnings. For a cyclical, mature business like MasterBrand, this measure offers context on pricing versus sector norms and anticipated growth. A ratio close to the industry average suggests the market is neither discounting nor excessively rewarding MasterBrand's profit potential.

Although MasterBrand appears attractively valued relative to the wider industry, it's worth noting that compared to a select group of peers, its P/E is elevated. This may signal the market is expecting stronger performance or improved sentiment going forward. In the absence of a distinctive “fair ratio” calculated from regression analysis, investors should stay alert in case market perceptions change suddenly.

See what the numbers say about this price — find out in our valuation breakdown.

Result: Price-to-Earnings of 16.9x (ABOUT RIGHT)

However, lingering revenue declines and a sizable discount to analyst targets remain. This suggests that ongoing uncertainty could still weigh on MasterBrand's valuation story.

Find out about the key risks to this MasterBrand narrative.

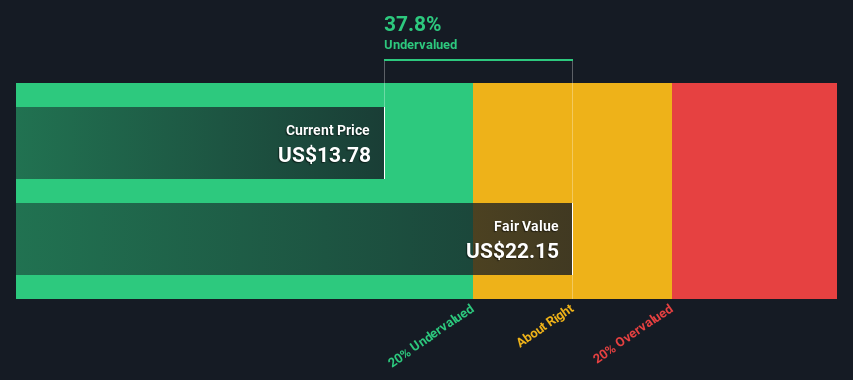

Another View: Discounted Cash Flow Signals Opportunity

While the market currently values MasterBrand similarly to its industry peers based on earnings, our DCF model takes a different approach. It suggests MasterBrand is trading around 13% below its estimated fair value, indicating potential undervaluation. Could the SWS DCF model be highlighting something that the market is overlooking?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out MasterBrand for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 924 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own MasterBrand Narrative

If you prefer to dig into the numbers yourself or think your perspective would reveal a different story, it’s quick and easy to build your own take. Do it your way

A great starting point for your MasterBrand research is our analysis highlighting 1 key reward and 4 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Now’s your chance to get ahead. Don’t settle for just one stock when there are other exciting opportunities waiting to accelerate your portfolio’s growth.

- Unlock potential with high-yield options and start earning from these 14 dividend stocks with yields > 3% offering yields above 3%.

- Catch the wave of technological innovation by checking out these 26 AI penny stocks making headlines in the AI sector.

- Spot bargains before the crowd does by targeting these 924 undervalued stocks based on cash flows that may be flying under Wall Street’s radar.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com