A Fresh Look at Ondas Holdings’s Valuation After Record Q3 Revenue, Major Acquisitions, and Growth Initiatives

Ondas Holdings, a US-based company, has filed a $219 million shelf registration after a record third quarter of revenue and major investments in the counter-UAS and defense robotics spaces. Investors are watching closely as the company broadens its financial and strategic toolkit for future growth.

See our latest analysis for Ondas Holdings.

Momentum around Ondas Holdings has accelerated as a result of its strategic moves and record-setting quarter, with the stock’s 1-day share price return of nearly 30% capturing surging investor confidence. Over the past year, total shareholder return has soared above 900%, reflecting both short-term excitement and a longer-term recovery despite a challenging five-year stretch.

If you’re interested in what’s driving similar breakthroughs across aerospace and defense, consider exploring See the full list for free.

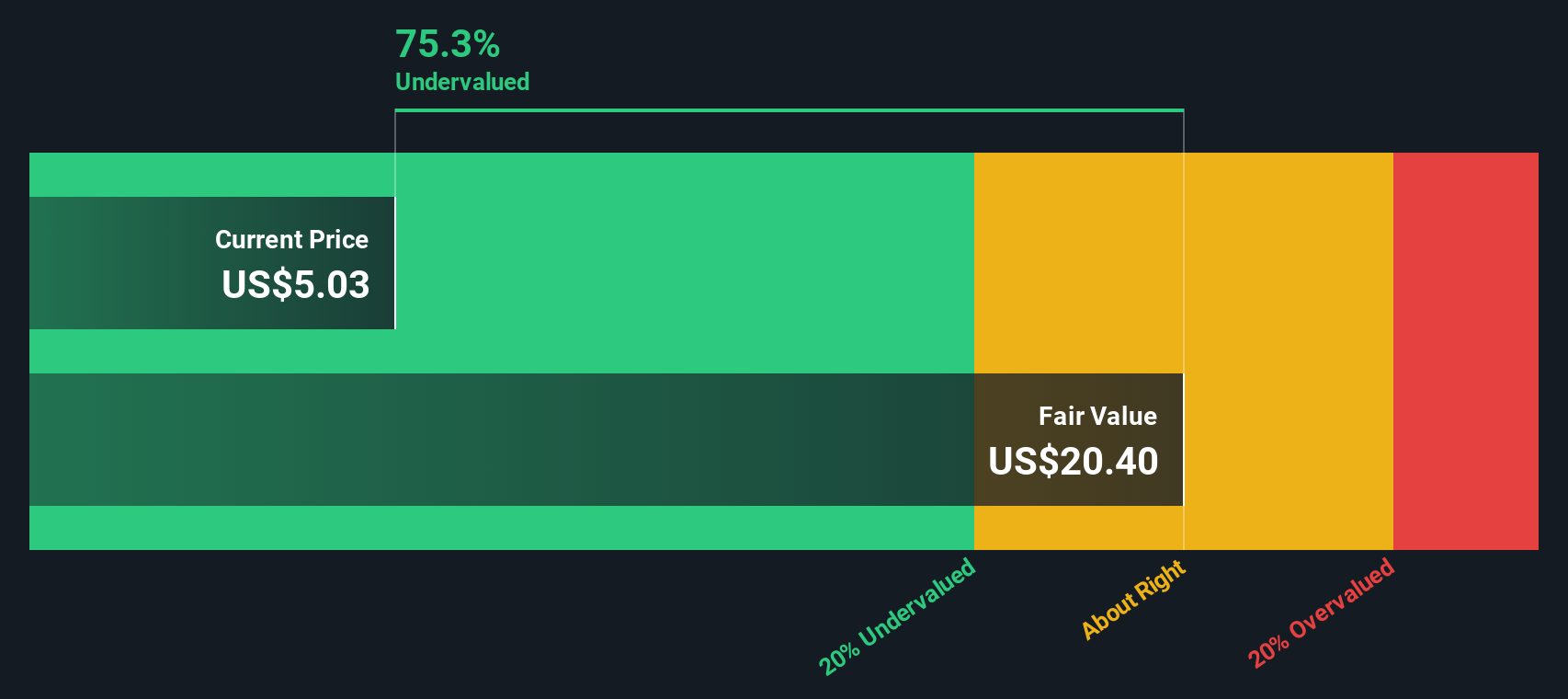

With shares already posting triple-digit annual returns and bullish revenue forecasts on the table, the key question for investors is clear: Is Ondas Holdings still undervalued at current levels, or has the market already priced in its future growth?

Most Popular Narrative: 19.7% Undervalued

Ondas Holdings’s most popular valuation narrative puts its fair value at $10.86 per share, which is notably higher than the last close price of $8.72. This perspective sets expectations for significant further upside if the projections come to pass.

"Gross margin, while currently at 26%, is projected to approach 70% over the next several years. This supports stronger profitability and unlocks higher long-term value."

Curious what’s fueling this market optimism? The formula behind the headline fair value rests on rapid sales growth, big margin expansion and a bold profit trajectory. Which number is the real linchpin for this bullish calculation? Click to reveal the full narrative’s key leap of faith.

Result: Fair Value of $10.86 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, continued delays at Ondas Networks or unforeseen disruptions in key markets could quickly challenge even the most optimistic projections for future growth.

Find out about the key risks to this Ondas Holdings narrative.

Another View: What Does the SWS DCF Model Say?

Looking at Ondas Holdings from the perspective of the SWS DCF model, the story grows even more intriguing. The DCF approach estimates a fair value of $18.28 per share, which is well above both the current market price and other analyst targets. Could this suggest hidden upside the market has yet to realize?

Look into how the SWS DCF model arrives at its fair value.

Build Your Own Ondas Holdings Narrative

If these valuations leave you unconvinced, you can dive into Ondas Holdings’s data yourself and build a personalized investment story in just minutes with Do it your way.

A great starting point for your Ondas Holdings research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

Looking for More Investment Ideas?

Smart investors never settle for just one opportunity. Make your next move count by targeting stocks with strong growth signals and unique market advantages right now.

- Supercharge your portfolio with high-yield picks by checking out these 15 dividend stocks with yields > 3%, featuring companies that consistently offer attractive dividend payouts above market averages.

- Jump ahead of market trends by exploring these 26 AI penny stocks, where breakthrough artificial intelligence innovations are creating potential for outsized returns.

- Capture unrealized value with these 924 undervalued stocks based on cash flows and get an early look at companies trading below their intrinsic worth based on hard fundamentals.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com