Exploring Centene Shares After 12% Rally and Medicaid Policy Headlines in 2025

- Curious if Centene stock could be a hidden opportunity or if it's simply out of favor? You're not alone. Smart investors are asking similar questions about whether now is the time to buy in.

- Centene's shares have bounced 2.9% over the past week and 12.0% in the last month, even though they've taken a big hit year-to-date, down 36.9%.

- Recent headlines have centered on healthcare reforms and shifting government contracts, which add both uncertainty and potential upside for the company. Industry-wide debates over Medicaid managed care policies have also pushed healthcare stocks, including Centene, into the spotlight.

- Right now, Centene scores a solid 5 out of 6 in our valuation health check. This suggests the stock passes most undervaluation tests. Let's break down how we arrive at that score across different valuation methods and keep an eye out for the approach that may best capture Centene's real value at the end of this article.

Find out why Centene's -37.9% return over the last year is lagging behind its peers.

Approach 1: Centene Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow (DCF) model estimates a company's intrinsic value by projecting its future cash flows and discounting them back to today's value. This approach aims to capture the worth of Centene based on its ability to generate cash over time.

Centene's most recent reported Free Cash Flow stands at $3.24 Billion. Analyst consensus provides projections through 2029, where Free Cash Flow is anticipated to reach $3.45 Billion. Notably, Simply Wall St extends these forecasts further out and extrapolates Centene's yearly cash flows up to 2035 with a blend of analyst estimates and in-house growth assumptions. This model relies on a 2-Stage Free Cash Flow to Equity methodology to capture both nearer-term forecasts and longer-range potential.

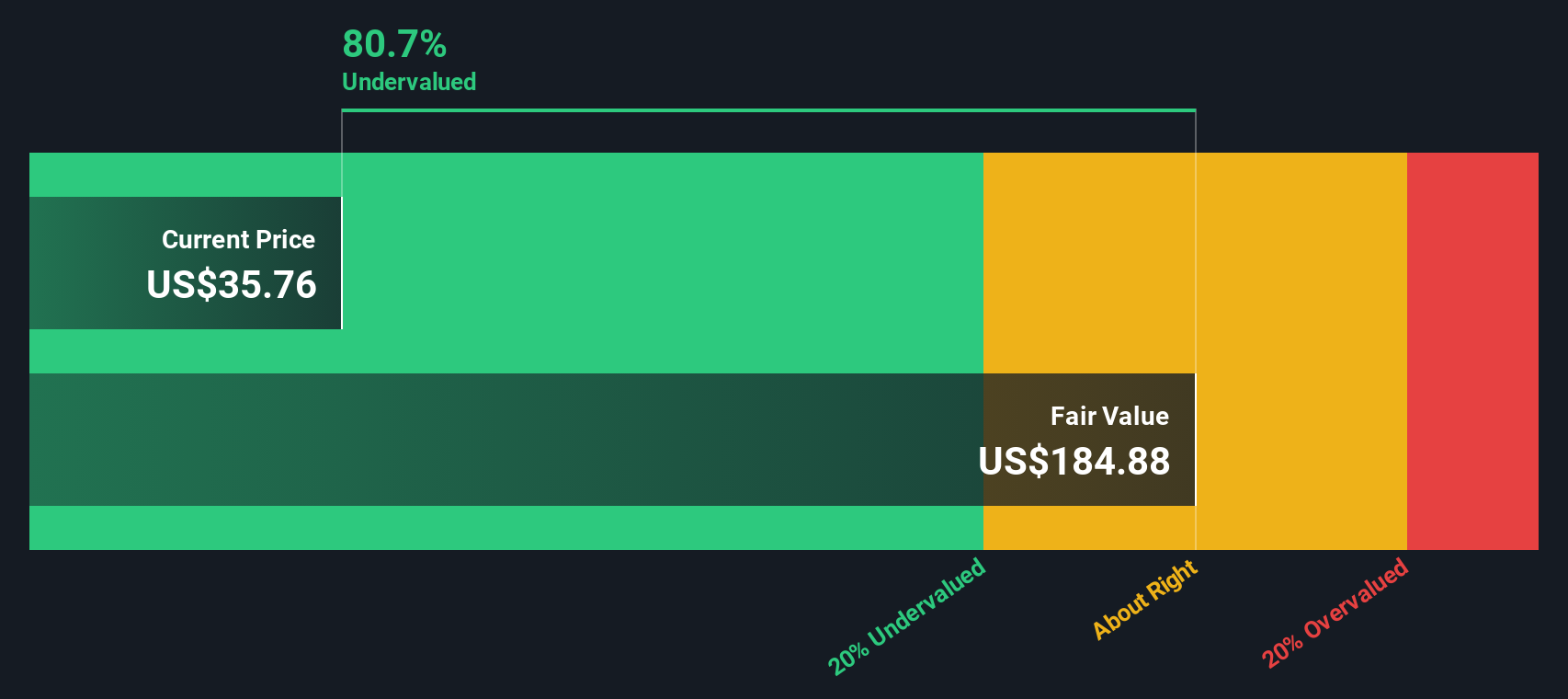

According to this DCF approach, Centene's estimated intrinsic value comes to $188.73 per share. Based on the current share price, the stock is trading at a 79.8% discount to this calculated fair value. This means DCF analysis sees Centene as significantly undervalued at present.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Centene is undervalued by 79.8%. Track this in your watchlist or portfolio, or discover 926 more undervalued stocks based on cash flows.

Approach 2: Centene Price vs Sales (P/S) Multiple

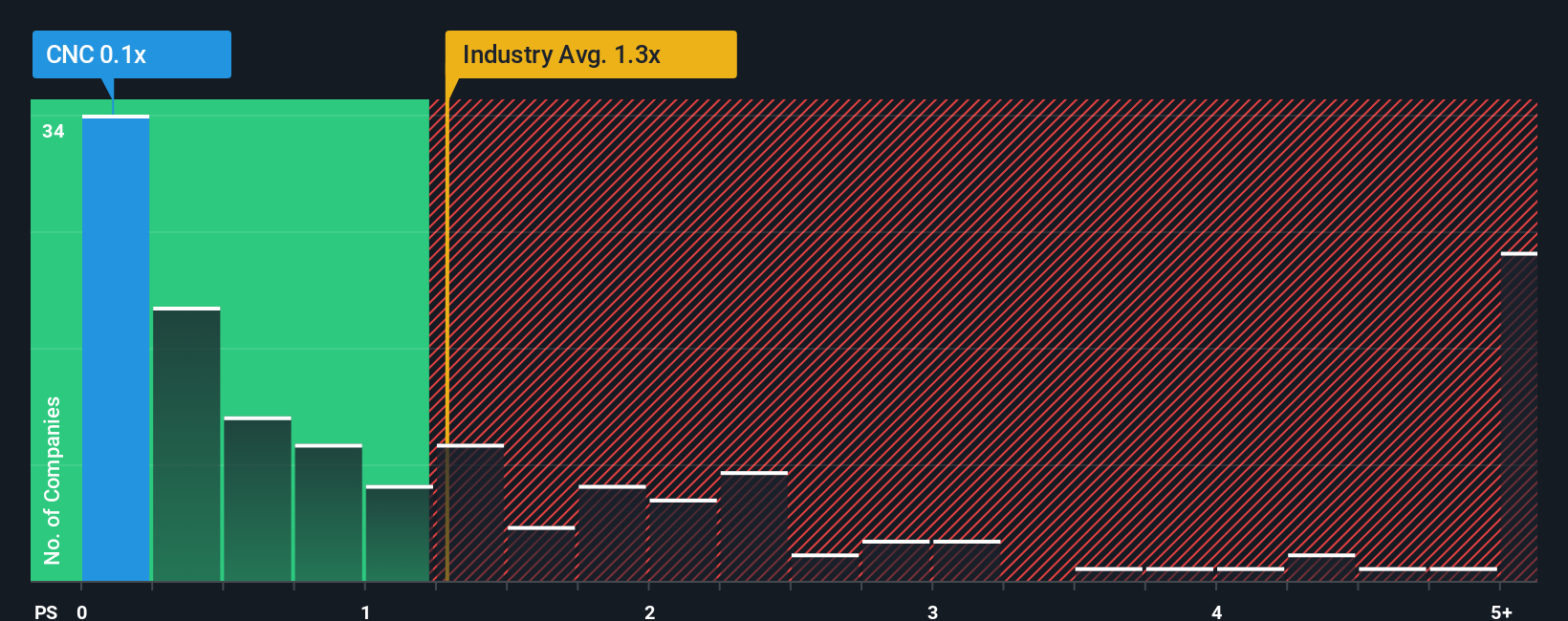

For profitable companies like Centene, the Price-to-Sales (P/S) multiple is often a solid way to gauge valuation, especially in sectors where revenue reliability is high and profit margins may fluctuate due to regulatory or macroeconomic factors. The P/S ratio shows how much investors are willing to pay for each dollar of Centene’s sales, which is particularly useful for comparing companies with different earnings structures.

Growth expectations and perceived risk play key roles in setting a “normal” or “fair” P/S ratio. Companies with higher growth prospects or greater stability often command higher multiples. In contrast, if there are risks or slower growth, the fair multiple tends to be lower.

Currently, Centene trades at a P/S ratio of just 0.11x, which is noticeably below both the healthcare industry average of 1.29x and the peer group average of 1.95x. This suggests Centene is valued at a significant discount to its sector. Simply Wall St’s “Fair Ratio” provides a more nuanced, tailored view by taking into account Centene’s specific growth forecasts, profit margins, industry dynamics, and market cap. Their proprietary metric estimates a fair P/S multiple of 0.79x. Unlike simple peer or industry comparisons, this Fair Ratio reflects the company’s unique risk profile and future outlook, making it more relevant to today’s investors.

With Centene’s actual P/S ratio sitting well below this fair benchmark, the stock appears substantially undervalued by this method.

Result: UNDERVALUED

PS ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1441 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose Your Centene Narrative

Earlier we mentioned that there's an even better way to understand valuation, so let's introduce you to Narratives. A Narrative is essentially your story—your perspective on Centene's future, bringing together your own expectations for revenue, profit margins, and fair value to clearly link the company’s business potential with a financial outcome.

Unlike traditional valuation models that rely strictly on numbers, Narratives empower you to embed your outlook on the business, management, and industry landscape right into your forecasts. This approach allows investors to make buy or sell decisions by seeing how their estimated fair value compares to the current price. Because Narratives are available on the Simply Wall St Community page, they are accessible to millions of everyday investors.

What sets Narratives apart is their dynamic nature, automatically updating when new information or news is released. This means your investment thesis remains relevant and actionable. For example, one investor might build a bullish Narrative for Centene, forecasting strong Medicaid margin recovery and estimating a fair value near $70 per share, while another may take a cautious view, factoring in policy risks and projecting fair value as low as $24. With Narratives, you can easily see both perspectives and quickly test your own assumptions.

Do you think there's more to the story for Centene? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com