Why Agios Pharmaceuticals (AGIO) May See Shifting Fortunes After Strong Phase 3 Sickle Cell Data

- On November 19, 2025, Agios Pharmaceuticals announced positive topline results from the 52-week double-blind period of its global Phase 3 RISE UP trial of mitapivat, a novel oral PK activator for patients aged 16 years or older with sickle cell disease, showing a statistically significant improvement in hemoglobin response versus placebo.

- Nearly all patients completing the double-blind study period chose to enter the ongoing open-label extension, highlighting continued interest and confidence in mitapivat's efficacy and safety profile.

- We'll consider how the strong Phase 3 results for mitapivat in sickle cell disease may alter Agios Pharmaceuticals' investment outlook.

These 11 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

Agios Pharmaceuticals Investment Narrative Recap

To be an Agios Pharmaceuticals shareholder, you need conviction in the company’s potential to turn its lead drug, mitapivat, into a commercial success across multiple rare blood disorders. The recent RISE UP Phase 3 trial results are a crucial near-term catalyst, as they provide strong clinical validation for mitapivat in sickle cell disease, but persistent operating losses and ongoing high trial costs remain the biggest risks, and these challenges are likely to persist in the near term despite the positive data.

Among recent announcements, the upcoming FDA decision for mitapivat in thalassemia is particularly relevant, as it directly ties to Agios’ efforts to expand its commercial reach and diversify revenue beyond sickle cell disease. The timing of these regulatory milestones could significantly influence market confidence, especially as the company seeks to move past its current period of financial strain.

However, against this clinical progress, investors should be aware that high ongoing R&D and SG&A expenses could…

Read the full narrative on Agios Pharmaceuticals (it's free!)

Agios Pharmaceuticals’ outlook projects $416.9 million in revenue and $67.0 million in earnings by 2028. This calls for a 116.9% annual revenue growth rate but an earnings decrease of $583.1 million from current earnings of $650.1 million.

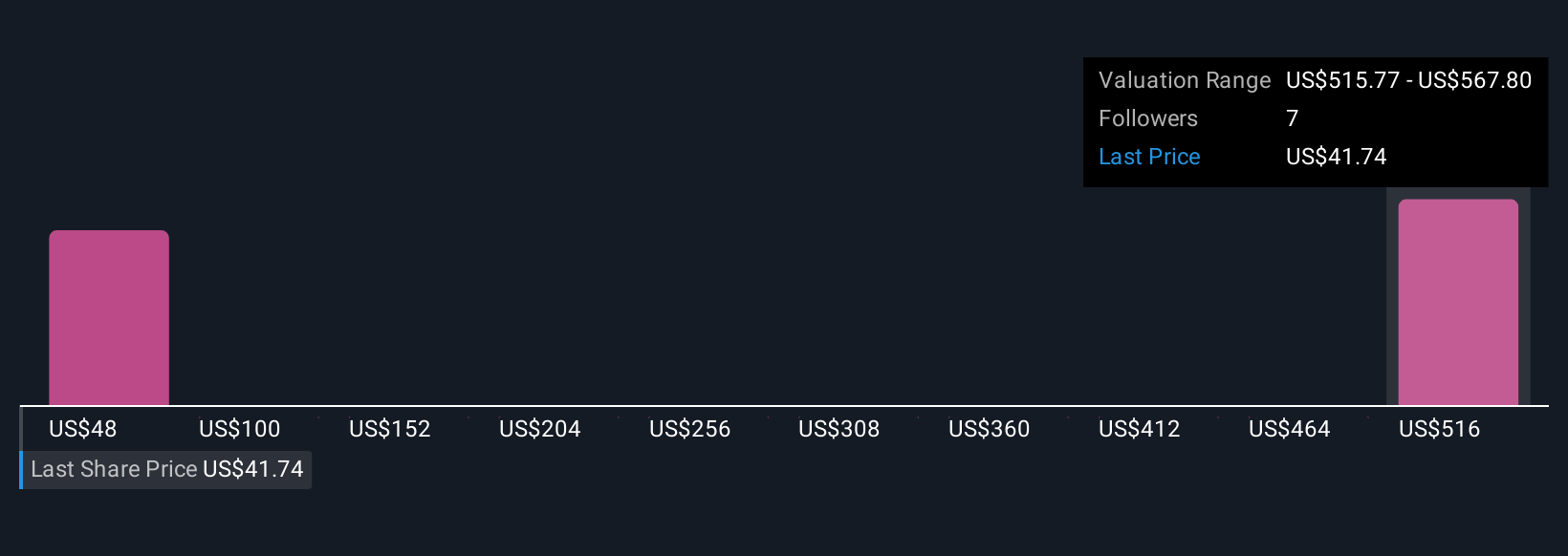

Uncover how Agios Pharmaceuticals' forecasts yield a $42.33 fair value, a 68% upside to its current price.

Exploring Other Perspectives

Simply Wall St Community members set fair value estimates for Agios Pharmaceuticals ranging from US$42 to US$692, across two perspectives. While optimism surrounds new clinical data, elevated costs and ongoing losses raise questions about the path to profitability.

Explore 2 other fair value estimates on Agios Pharmaceuticals - why the stock might be a potential multi-bagger!

Build Your Own Agios Pharmaceuticals Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Agios Pharmaceuticals research is our analysis highlighting 2 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Agios Pharmaceuticals research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Agios Pharmaceuticals' overall financial health at a glance.

Ready For A Different Approach?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

- Outshine the giants: these 26 early-stage AI stocks could fund your retirement.

- Trump's oil boom is here - pipelines are primed to profit. Discover the 22 US stocks riding the wave.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com