How Morgan Stanley’s Upgrade May Shape Apollo Global Management’s (APO) Earnings Growth Narrative

- Earlier this week, Morgan Stanley upgraded Apollo Global Management to Overweight, citing confidence in the firm's accelerated fee-related and spread-related earnings growth over the next two years.

- This renewed analyst optimism comes amid a series of high-profile conference presentations and special calls, placing Apollo's leadership and outlook under greater investor attention.

- We'll look at how Morgan Stanley's improved outlook on Apollo's earnings growth trajectory could influence its investment narrative.

Explore 26 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

Apollo Global Management Investment Narrative Recap

To be a shareholder in Apollo Global Management, an investor must believe in the firm’s ability to deliver consistent fee and spread-related earnings growth while competing effectively in alternative asset management. The recent Morgan Stanley upgrade reflects analyst confidence in Apollo’s growth acceleration, though the most important short-term catalyst remains execution against these higher expectations; internal execution risks still pose the biggest challenge and this upgrade does not materially change that risk profile.

One announcement tying directly to growth catalysts is Apollo’s ongoing share repurchase program, which saw over 2.5 million shares bought back last quarter. This continued capital return underscores management’s commitment to boosting shareholder value and may reinforce the bullish sentiment sparked by improved analyst earnings forecasts, while focusing attention on whether operational execution can keep pace with market optimism.

By contrast, investors also need to be aware of internal execution risks that could...

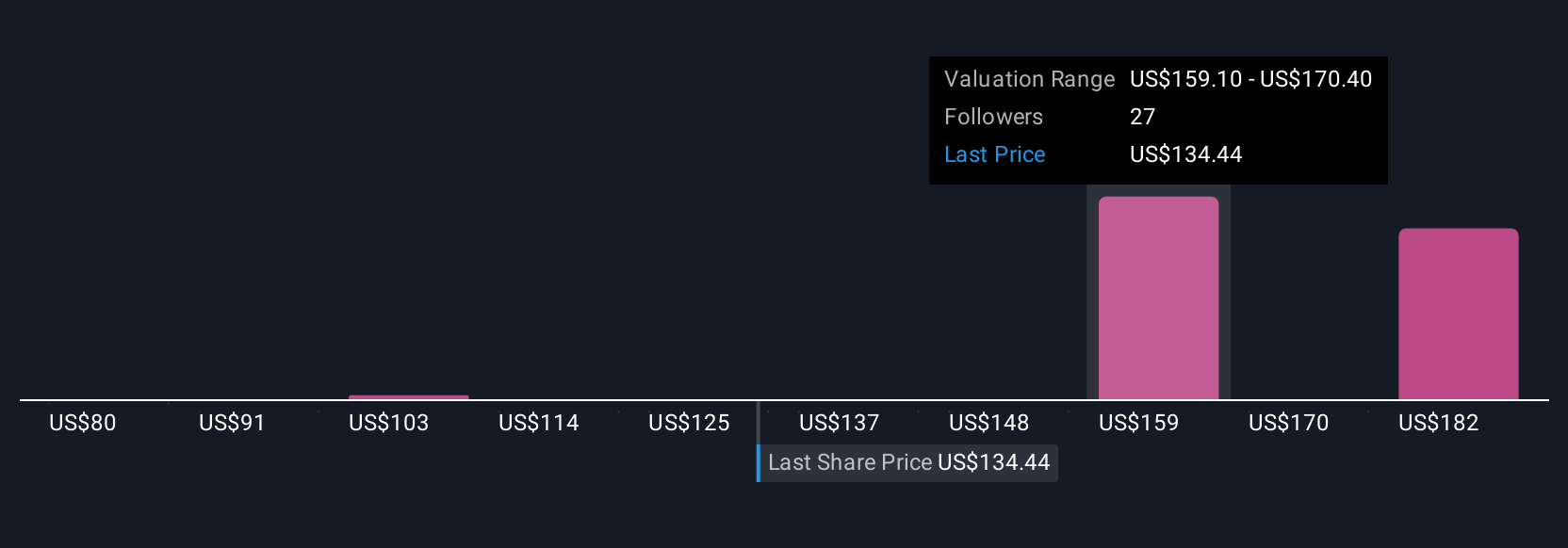

Read the full narrative on Apollo Global Management (it's free!)

Apollo Global Management's narrative projects $1.1 billion in revenue and $6.6 billion in earnings by 2028. This requires a 64.6% yearly revenue decline and an earnings increase of $3.5 billion from $3.1 billion today.

Uncover how Apollo Global Management's forecasts yield a $158.22 fair value, a 22% upside to its current price.

Exploring Other Perspectives

Six private investors in the Simply Wall St Community offer fair value estimates for Apollo ranging from US$110 to US$236,698, sharply above current trading levels. With execution risk still top of mind, a diverse mix of opinions highlights several factors shaping the debate about Apollo’s future growth and pricing, take a closer look at why your outlook might differ.

Explore 6 other fair value estimates on Apollo Global Management - why the stock might be worth 15% less than the current price!

Build Your Own Apollo Global Management Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Apollo Global Management research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Apollo Global Management research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Apollo Global Management's overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 36 best rare earth metal stocks of the very few that mine this essential strategic resource.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com