Three Undiscovered Gems in Asia Backed By Strong Fundamentals

As global markets grapple with AI-related concerns and fluctuating economic indicators, the Asian market presents unique opportunities for investors seeking growth. In this environment, identifying stocks with strong fundamentals becomes crucial, as they are more likely to withstand broader market volatility and capitalize on regional economic strengths.

Top 10 Undiscovered Gems With Strong Fundamentals In Asia

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Shandong Sinoglory Health Food | NA | 4.47% | 5.27% | ★★★★★★ |

| Central Forest Group | NA | 5.20% | 24.71% | ★★★★★★ |

| SEC Electric Machinery | NA | -5.40% | -44.23% | ★★★★★★ |

| Shenyang Yuanda Intellectual Industry GroupLtd | NA | 9.86% | 33.52% | ★★★★★★ |

| Nanjing Well Pharmaceutical GroupLtd | 33.54% | 10.14% | 9.90% | ★★★★★☆ |

| Daewon Cable | 21.76% | 7.48% | 44.88% | ★★★★★☆ |

| YFY | 69.02% | -0.89% | -30.70% | ★★★★☆☆ |

| Nippon Sharyo | 48.57% | -0.32% | -3.31% | ★★★★☆☆ |

| Qijing Machinery | 38.27% | 3.10% | -2.56% | ★★★★☆☆ |

| Aurora OptoelectronicsLtd | 4.19% | -12.12% | 20.63% | ★★★★☆☆ |

Underneath we present a selection of stocks filtered out by our screen.

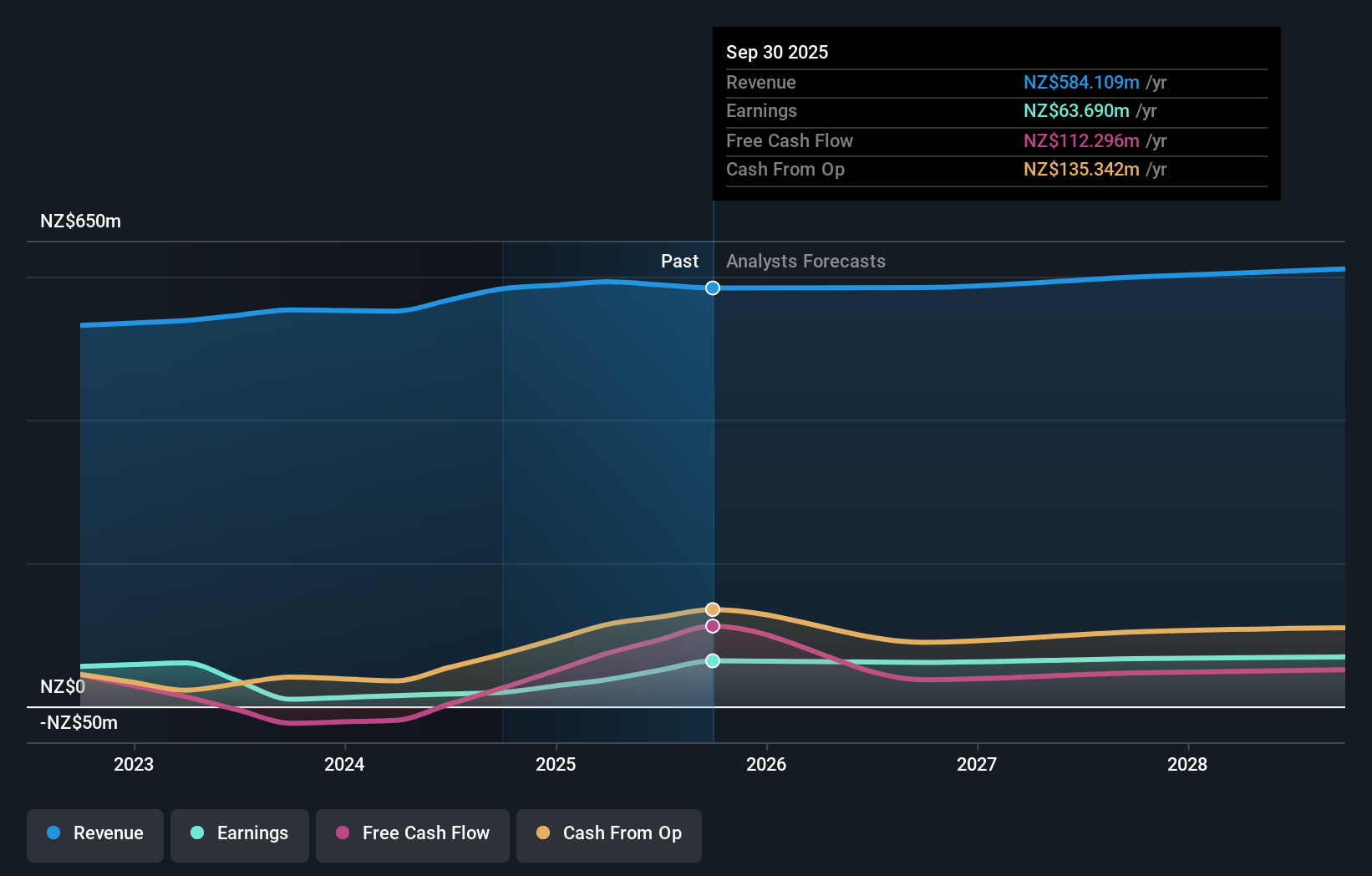

Sanford (NZSE:SAN)

Simply Wall St Value Rating: ★★★★★★

Overview: Sanford Limited is involved in the farming, harvesting, processing, storage, and marketing of seafood products with a market cap of NZ$682.59 million.

Operations: Sanford Limited generates revenue primarily from the farming, harvesting, processing, and selling of seafood products amounting to NZ$584.11 million.

Sanford's recent performance highlights its potential as a compelling investment opportunity. With earnings skyrocketing by 223% over the past year, it outpaces the broader food industry growth of 73%. This financial leap is supported by a solid net debt to equity ratio of 12.6%, reflecting prudent financial management as it decreased from 30.8% over five years. Sanford’s interest payments are comfortably covered with an EBIT coverage of 8.3 times, indicating strong operational efficiency. Trading at about 26% below its estimated fair value, Sanford appears well-positioned against peers and industry standards for relative value.

- Click here to discover the nuances of Sanford with our detailed analytical health report.

Assess Sanford's past performance with our detailed historical performance reports.

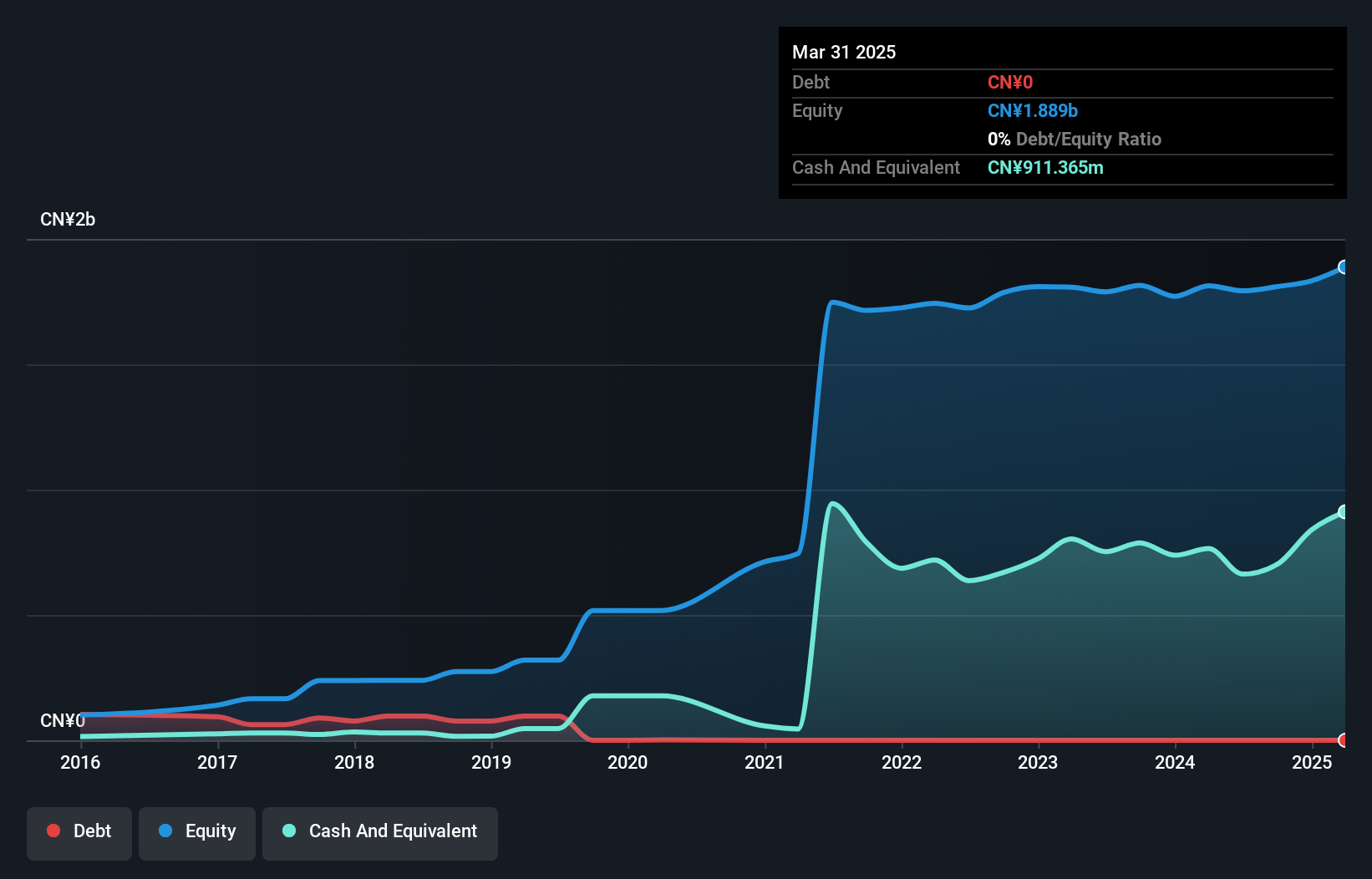

Tianjin Yiyi Hygiene ProductsLtd (SZSE:001206)

Simply Wall St Value Rating: ★★★★★★

Overview: Tianjin Yiyi Hygiene Products Co., Ltd specializes in the R&D, design, production, and sale of disposable pet and personal hygiene care products both domestically and internationally, with a market capitalization of CN¥6.11 billion.

Operations: Tianjin Yiyi generates revenue through the sale of disposable pet and personal hygiene products. The company's cost structure includes expenses related to research, design, production, and sales activities. It has a market capitalization of CN¥6.11 billion.

Tianjin Yiyi, a player in the hygiene products sector, is catching attention with its high-quality earnings and impressive growth. Over the past year, earnings surged by 32.4%, outpacing the industry average of 21.4%. The company is debt-free and trades at a significant discount of 51.5% to its estimated fair value, hinting at potential upside for investors. For the first nine months of 2025, net income rose to CNY 156.7 million from CNY 150.93 million last year, while basic EPS increased to CNY 0.85 from CNY 0.82. Additionally, it repurchased shares worth CNY 11.34 million recently.

Create SD Holdings (TSE:3148)

Simply Wall St Value Rating: ★★★★★★

Overview: Create SD Holdings Co., Ltd. operates in Japan through its subsidiaries, focusing on drug stores, dispensing pharmacies, and nursing care services, with a market cap of ¥217.06 billion.

Operations: Create SD Holdings generates revenue primarily from its drug store business, which accounts for ¥464.78 billion.

Create SD Holdings stands out in the Asian market with a solid track record, boasting earnings growth of 17.6% over the past year, which surpasses the Consumer Retailing industry's 10.8%. The company operates debt-free and has maintained this status for five years, eliminating concerns over interest payments. With a Price-To-Earnings ratio of 13.4x, it offers good value compared to Japan's market average of 13.9x. The firm is also free cash flow positive, generating ¥5,972 million recently despite significant capital expenditures around ¥17 billion annually. These factors suggest a robust financial footing and potential for future growth amidst industry challenges.

- Delve into the full analysis health report here for a deeper understanding of Create SD Holdings.

Understand Create SD Holdings' track record by examining our Past report.

Turning Ideas Into Actions

- Click through to start exploring the rest of the 2485 Asian Undiscovered Gems With Strong Fundamentals now.

- Already own these companies? Link your portfolio to Simply Wall St and get alerts on any new warning signs to your stocks.

- Elevate your portfolio with Simply Wall St, the ultimate app for investors seeking global market coverage.

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com