A Look at Intesa Sanpaolo (BIT:ISP) Valuation Following CEO Change in Albanian Operations

Intesa Sanpaolo (BIT:ISP) has named Giuseppe Giampietro as the new chief executive for its operations in Albania, succeeding Alessandro D'Oria after his four-year tenure. Giampietro’s appointment follows 25 years with the group and includes several leadership roles, sparking fresh interest in the bank’s regional strategy.

See our latest analysis for Intesa Sanpaolo.

Recent momentum for Intesa Sanpaolo is building, with its share price up nearly 46% so far this year and total shareholder return topping 60% for the past 12 months. Strategic shifts, such as the new leadership in Albania, are catching investors’ attention and fueling optimism about growth potential for the group over the longer term.

If you’re curious what else seasoned insiders are backing, now’s a smart time to discover fast growing stocks with high insider ownership

With shares rallying nearly 60% in a year and trading just shy of analyst targets, investors are left to wonder if Intesa Sanpaolo is still trading at a discount, or if the market is already pricing in the next phase of growth.

Most Popular Narrative: 8.8% Undervalued

With Intesa Sanpaolo’s estimated fair value at €6.16, which is about 9% above the last close of €5.62, the narrative suggests the market is not fully recognizing the bank’s earnings and growth potential. This sets the backdrop for the strategic view that follows.

Continued investment in digital transformation, including cloud migration, AI, and technology platforms, should lead to further operational cost reductions and improved customer reach. These efforts are expected to support higher net margins and long-term bottom-line growth.

Curious why analysts believe efficiency moves alone could power Intesa’s valuation? The real surprise might be how their future profit forecasts and margin assumptions shape the fair value calculation. Want to see which bold estimations underpin the narrative’s optimistic case? Unpack the hidden details driving this target.

Result: Fair Value of €6.16 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, significant dependence on Italy’s economy and intensifying competition from fintechs could quickly challenge Intesa Sanpaolo’s valuation story.

Find out about the key risks to this Intesa Sanpaolo narrative.

Another View: What Do Market Ratios Suggest?

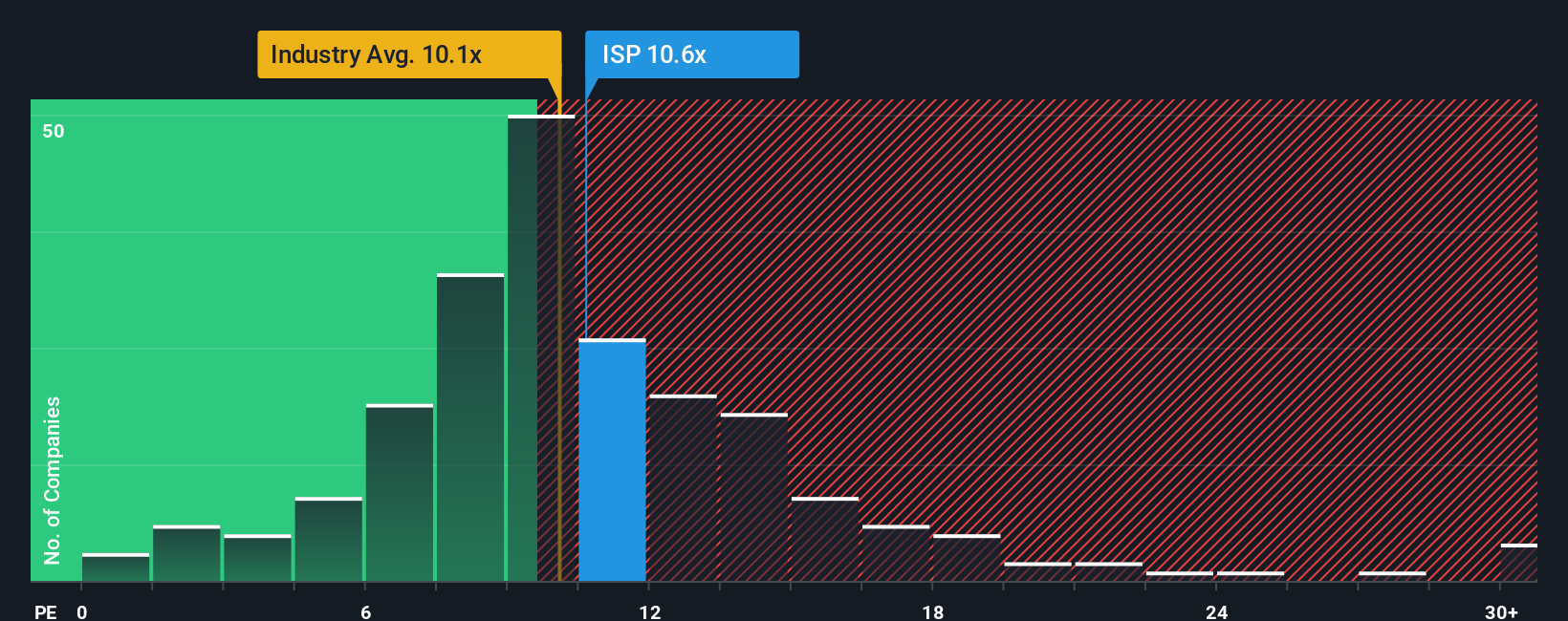

While the fair value estimate points to Intesa Sanpaolo trading at a discount, its current price-to-earnings ratio of 10.7x is actually higher than the industry average of 9.8x. This suggests a possible premium, which could potentially limit further upside unless future growth exceeds expectations. So, could investor optimism already be priced in?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Intesa Sanpaolo Narrative

If you have a different take or want to investigate the numbers for yourself, you can craft your own perspective in just a few minutes with Do it your way

A great starting point for your Intesa Sanpaolo research is our analysis highlighting 3 key rewards and 4 important warning signs that could impact your investment decision.

Looking for More Investment Ideas?

Smart investors always keep their options open, and Simply Wall Street’s screeners can point you toward new opportunities most people will overlook. Don’t settle for the obvious; your next winning stock pick could be waiting in one of these standout categories:

- Fuel your portfolio’s income with these 17 dividend stocks with yields > 3% boasting yields above 3%, so you can get paid while you wait for growth.

- Stay ahead of tech trends and capture early movers in artificial intelligence by checking out these 25 AI penny stocks right now.

- Catch undervalued companies before the market does by scanning these 919 undervalued stocks based on cash flows that may offer more upside than you expect.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com