Will Eversource Energy's (ES) Blocked Aquarion Sale Reshape Its Balance Sheet Strategy?

- Earlier this week, Connecticut's Public Utilities Regulatory Authority denied Eversource Energy's proposed US$2.4 billion sale of its Aquarion Water subsidiary to a newly created quasi-public entity.

- This regulatory decision, based primarily on concerns over the buyer’s governance structure, disrupts Eversource’s efforts to streamline operations and reduce debt.

- We'll consider how Connecticut's rejection of the Aquarion sale may affect Eversource's balance sheet improvement plans within its investment narrative.

We've found 17 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

Eversource Energy Investment Narrative Recap

At the heart of the Eversource Energy investment story is the belief in steady, regulated utility returns supported by regional electrification and infrastructure upgrades. The recent denial by Connecticut regulators of the US$2.4 billion Aquarion Water sale disrupts management’s core balance sheet improvement plans, putting short-term focus squarely on debt reduction and cost recovery as the main catalysts and risks to watch; the direct impact is material given management’s clear reliance on this divestiture.

Among recent announcements, the company’s reaffirmation of its 2025 earnings guidance (US$4.72 to US$4.80 per share, with a 5–7% compound annual growth target) stands out. This guidance now faces greater scrutiny, as the failed Aquarion sale removes one lever for enhancing financial flexibility and credit metrics just as rate case outcomes and storm cost approvals grow more critical.

In sharp contrast, those following Eversource’s story should not overlook the risk that continued regulatory challenges in Connecticut may further...

Read the full narrative on Eversource Energy (it's free!)

Eversource Energy's outlook anticipates $14.8 billion in revenue and $2.1 billion in earnings by 2028. This scenario involves a 4.4% annual revenue growth rate and a $1.24 billion increase in earnings from the current $858.0 million.

Uncover how Eversource Energy's forecasts yield a $75.60 fair value, a 17% upside to its current price.

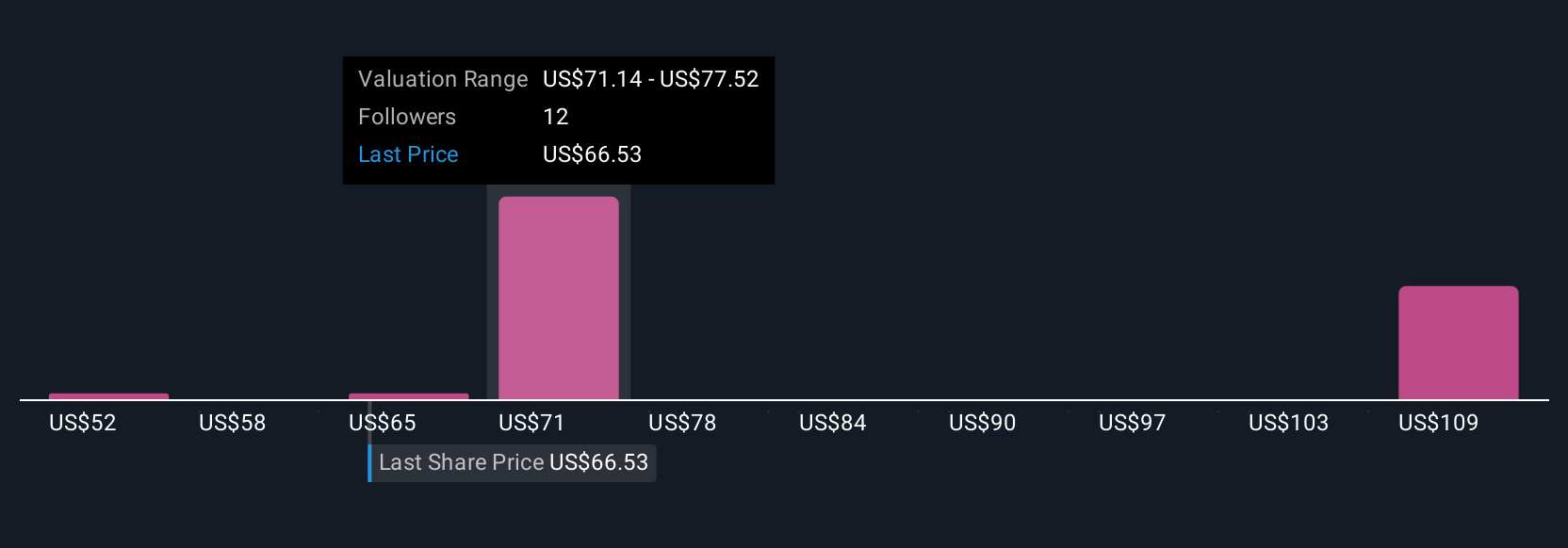

Exploring Other Perspectives

Simply Wall St Community members estimate Eversource’s fair value across a wide range, from US$52 to US$218.96 based on four unique forecasts. Regulatory uncertainty remains front and center, so explore these different perspectives to fully understand the potential impacts on future financial performance.

Explore 4 other fair value estimates on Eversource Energy - why the stock might be worth over 3x more than the current price!

Build Your Own Eversource Energy Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Eversource Energy research is our analysis highlighting 4 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Eversource Energy research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Eversource Energy's overall financial health at a glance.

Searching For A Fresh Perspective?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

- These 11 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 25 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com