W.W. Grainger (GWW): Evaluating Valuation After Months-Long Share Price Decline

W.W. Grainger (GWW) shares have seen some movement recently, catching investors’ attention as the stock continues a months-long decline. As Grainger’s revenue and profit trends show steady growth, there is curiosity around what might come next.

See our latest analysis for W.W. Grainger.

After a remarkable multiyear run, shares of W.W. Grainger have pulled back with a 1-year total shareholder return of -20.27%. Long-term holders are still sitting on a powerful 135.9% gain over five years. Recent drops could signal shifting expectations. Even with fundamentals like revenue and net income trending higher, momentum is clearly fading in the short term.

If this reversal has you wondering where else opportunities might be emerging, consider broadening your search and discovering fast growing stocks with high insider ownership

With the stock now trading below analyst price targets and core business metrics still climbing, the key question emerges: Is W.W. Grainger undervalued, or is the market already factoring in future growth potential?

Most Popular Narrative: 12.2% Undervalued

Based on the most widely followed narrative, W.W. Grainger’s fair value sits notably above the recent closing price. This suggests meaningful upside if the underlying financial story plays out. The narrative’s fair value target is grounded in analysts’ modeling of Grainger’s future growth, margins, and sector position. This sets the stage for a deeper look at the drivers behind this view.

The acceleration of digital transformation in B2B/industrial commerce is expanding the addressable market for Grainger's online platforms (especially Zoro and MonotaRO), driving faster-than-industry top-line gains, operating leverage, and margin expansion as e-commerce penetration rises. Growing complexity in global supply chains, combined with heightened regulatory and safety compliance needs, is causing customers to seek out one-stop, resilient distribution partners. This favors Grainger's breadth, product expertise, and robust distribution network for sustained market share gains and stable earnings.

Want to know what’s behind this valuation gap? This narrative leans on a digital transformation story and projections of faster top-line gains. See the detailed financial roadmap and bold assumptions analysts are using to justify a premium for Grainger’s shares. Are these estimates too ambitious or just the start?

Result: Fair Value of $1,054.60 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, persistent inflation or a prolonged slowdown in key end-markets could quickly challenge even the most optimistic growth expectations for Grainger.

Find out about the key risks to this W.W. Grainger narrative.

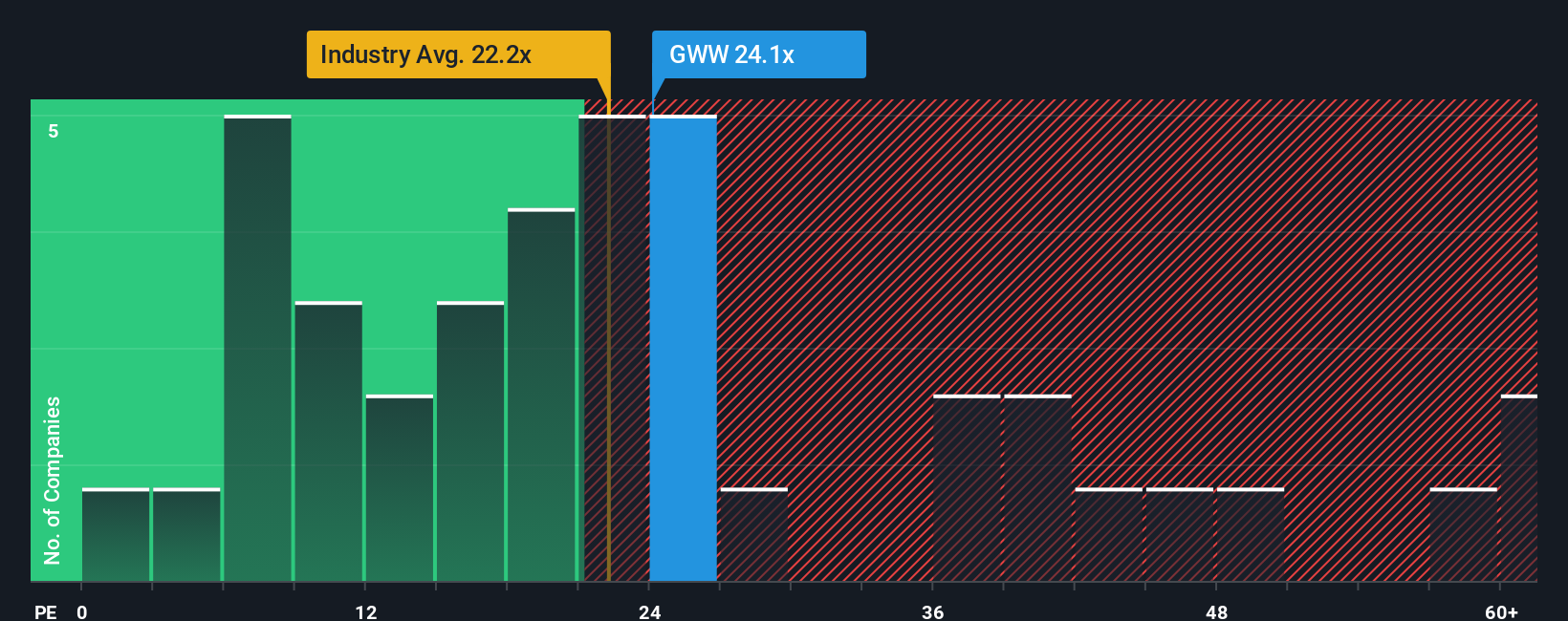

Another View: Industry Multiples Paint a Different Picture

Looking from a different angle, Grainger’s share price is higher than both the industry and peer group averages when you compare their price-to-earnings numbers. While the company's figure stands at 25.5x, rivals in the US Trade Distributors space average just 19.8x, and its peers average 22.9x. The current ratio is a touch below its calculated fair ratio of 26.7x. This suggests the market might now be closer to fair value. This premium signals confidence, but could it leave less room for upside if growth slows?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own W.W. Grainger Narrative

Curious to see how your analysis stacks up? Dive into the data and craft a narrative of your own in just a few minutes, Do it your way

A great starting point for your W.W. Grainger research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Looking for More Investment Ideas?

Maximize your exposure to top-performing stocks and fresh opportunities by branching beyond a single company. The market never waits. Seize new ideas now or risk missing the next big winner.

- Capture the momentum of artificial intelligence by targeting these 26 AI penny stocks at the forefront of tech-driven growth and innovation.

- Boost your income potential with these 16 dividend stocks with yields > 3% that consistently deliver strong yields and stable returns in any market environment.

- Stay ahead of market shifts and spot hidden gems through these 905 undervalued stocks based on cash flows currently trading below what their fundamentals suggest they're worth.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com