Is AT&T Still a Bargain After Recent 5G Expansion Momentum?

- Curious if AT&T is still a good deal, or if you've missed the boat? Let's dig in and find out whether the stock's price reflects its true value right now.

- AT&T's shares have climbed 16.3% over the past year and are up 12.1% year-to-date. However, the last month showed a slight pullback of -2.8%.

- Much of this momentum has centered around renewed investor optimism on telecom sector stability. Recent industry news about expanded 5G rollouts and infrastructure investments continues to set the backdrop for AT&T’s share price action.

- AT&T currently clocks in with a value score of 5 out of 6 on our valuation checks. There is more beneath the surface; next, we’ll break down the different ways to analyze value, and finish up with the most powerful valuation perspective savvy investors are using today.

Approach 1: AT&T Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow (DCF) model estimates a company's intrinsic value by projecting its future cash flows and discounting them back to today's value. This approach is especially useful for companies with steady and predictable cash generation, such as AT&T.

For AT&T, the current Free Cash Flow stands at $21.80 billion. Analyst estimates provide detailed projections for the next five years, after which future cash flows are extrapolated based on growth trends. By 2029, AT&T's Free Cash Flow is expected to reach $20.31 billion, reflecting stable long-term growth according to forecasts on Simply Wall St.

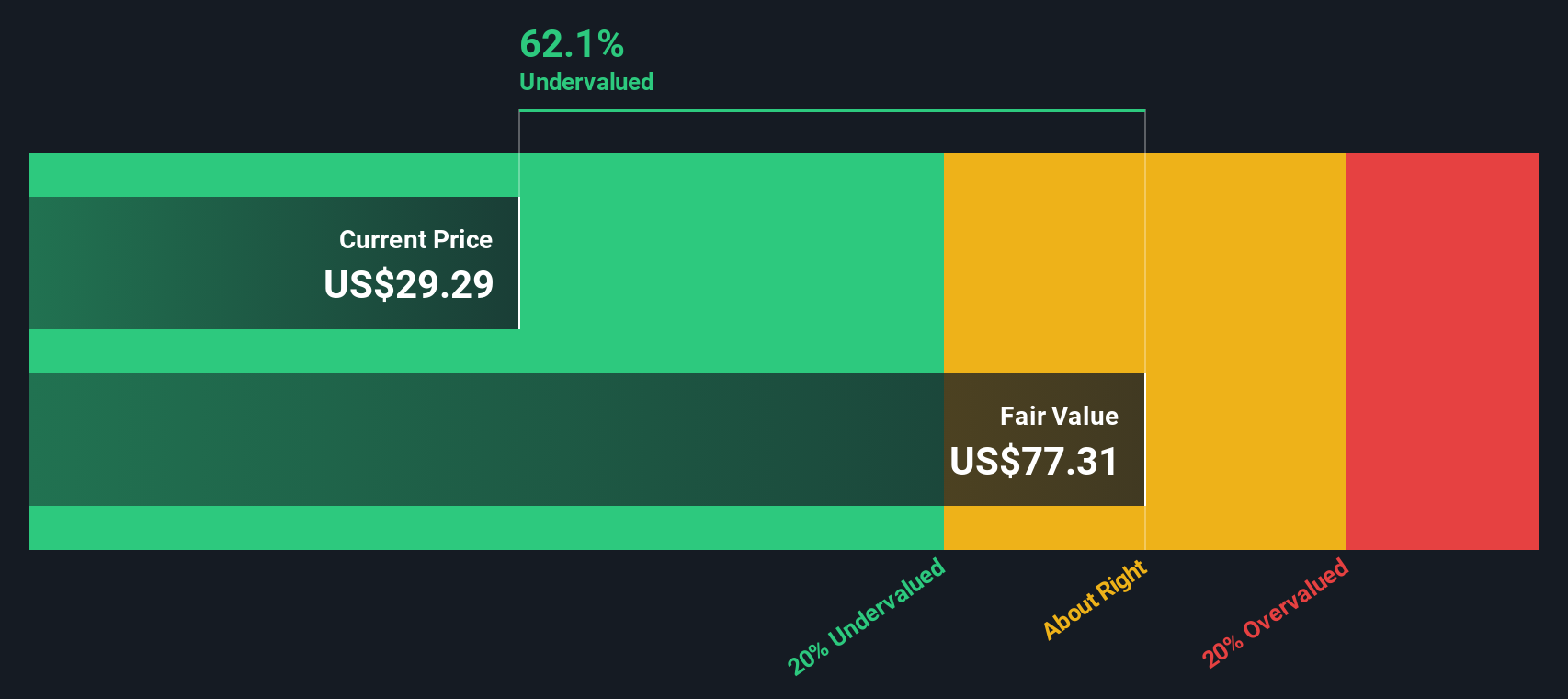

Based on these projections, the DCF model calculates an intrinsic value of $57.80 per share. Given the current market price, this implies that AT&T is trading at a 55.7% discount relative to its intrinsic value. In practical terms, the stock appears significantly undervalued when compared to its expected cash generation over the next decade.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests AT&T is undervalued by 55.7%. Track this in your watchlist or portfolio, or discover 905 more undervalued stocks based on cash flows.

Approach 2: AT&T Price vs Earnings (PE)

The Price-to-Earnings (PE) ratio is the most widely used metric to value profitable companies like AT&T, since it directly relates what investors are willing to pay for each dollar of current earnings. For businesses with a consistent profit track record, the PE gives a practical, apples-to-apples basis for comparing value across the sector.

Growth expectations and perceived risk play a big role in setting what counts as a "normal" or "fair" PE multiple. Companies with faster earnings growth, lower debt, and more resilient business models often command above-average PE ratios, while slower growers or those with more risk generally trade for less.

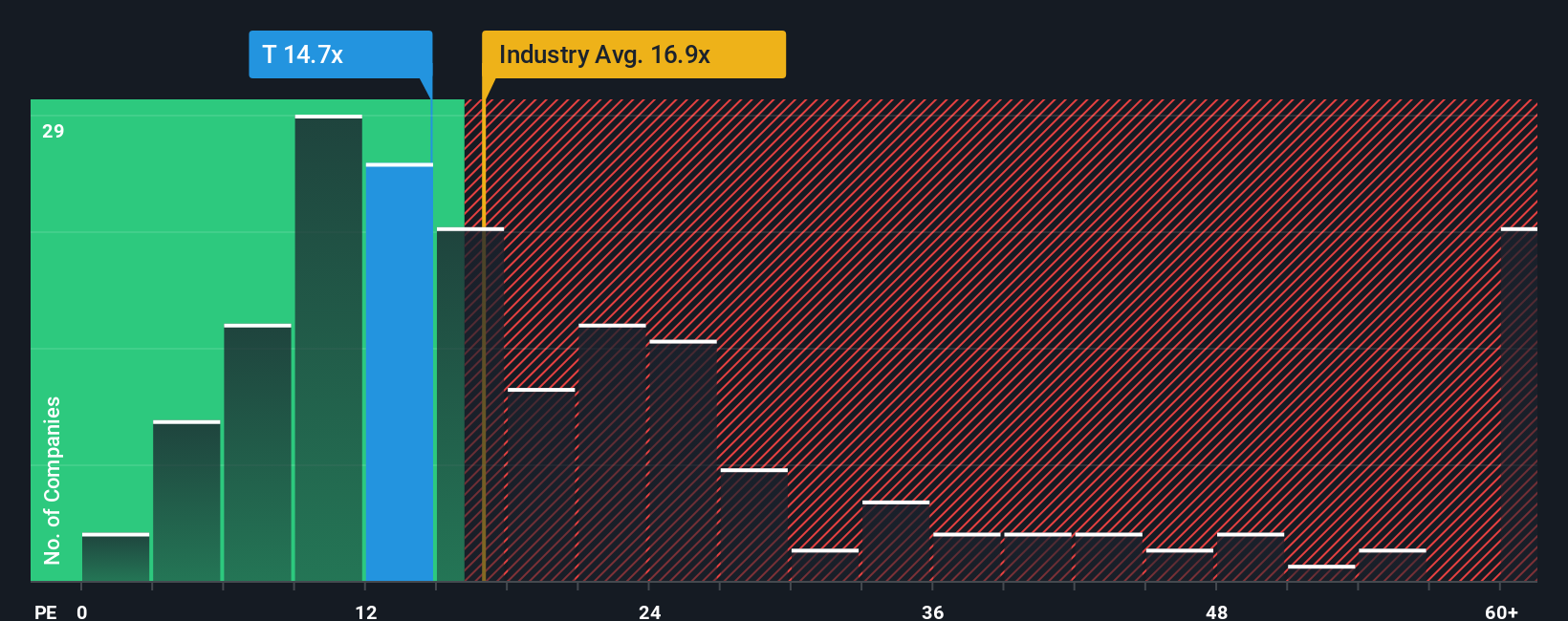

Currently, AT&T trades at an 8.18x PE, which is below both the broader telecom industry average of 16.24x and the peer average of 8.63x. However, benchmarks do not tell the full story. Simply Wall St’s proprietary "Fair Ratio" for AT&T comes in at 12.26x, reflecting the company’s unique blend of earnings growth, risk profile, profitability, size, and its place within the telecommunications sector.

The Fair Ratio is a more comprehensive benchmark than looking only at peers or the industry because it is tailored to AT&T’s own strengths and weaknesses. This means it adjusts expectations based on the company’s specific growth trajectory, margins, sector trends, and even market capitalization. The result is a more precise view of fair value.

Comparing AT&T’s actual PE of 8.18x with its Fair Ratio of 12.26x suggests the stock is currently undervalued based on earnings power, even after factoring in its risk and growth outlook.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1416 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your AT&T Narrative

Earlier we mentioned that there's an even better way to understand valuation, so let's introduce you to Narratives. A Narrative lets you create and share your own "story" about a company, your personal perspective that ties together what you believe about its future revenue, earnings, and margins with a fair value estimate.

Instead of relying only on formulas, Narratives allow you to explain the reasoning behind your forecasts and see how your outlook fits within the wider investment community. On Simply Wall St’s Community page, Narratives make it easy for anyone to connect the company's story (why things might change) to a financial forecast and through to a calculated fair value, linking real business drivers with numbers in an accessible, visual tool trusted by millions of investors.

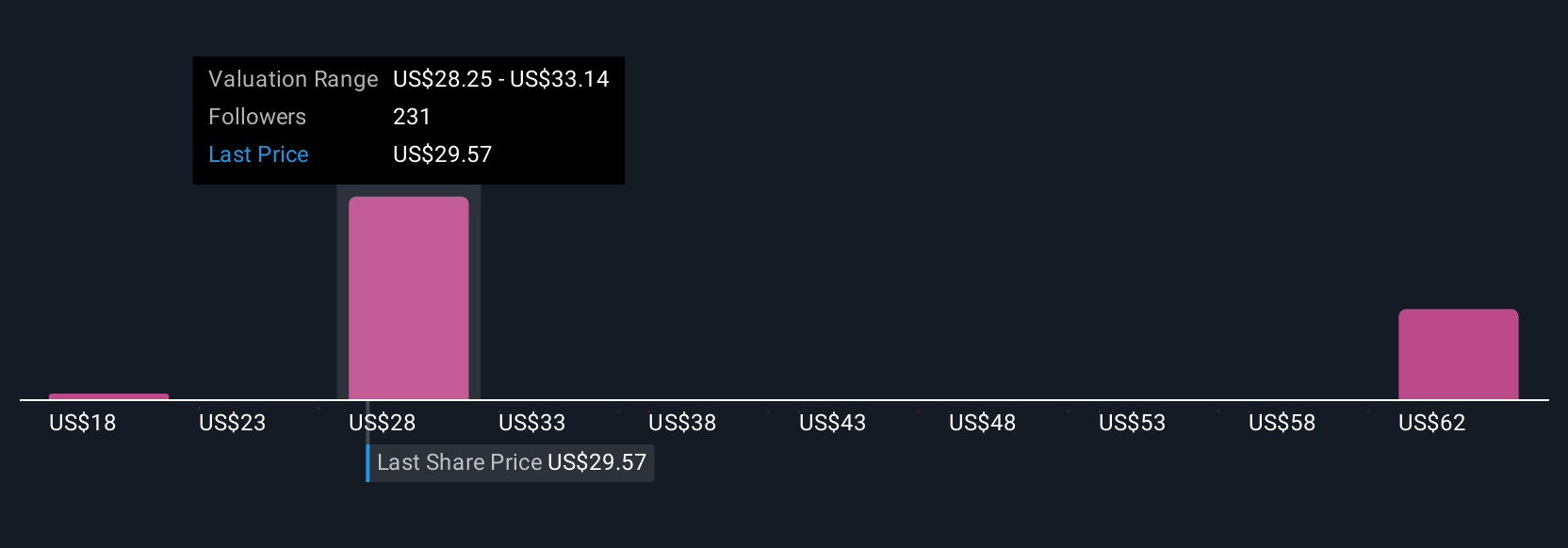

Because Narratives update automatically when fresh news or earnings are released, they are powerful for deciding when to buy or sell, as you can see at a glance how your own Fair Value compares to the current share price. For example, some see major upside for AT&T with a price target as high as $34.00, while others are more cautious, setting their target at $15.49. This showcases just how different perspectives can be when you build your own Narrative.

Do you think there's more to the story for AT&T? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com