Is Chipotle Still a Good Value After 47% Decline in 2025?

- Wondering whether Chipotle Mexican Grill is worth your attention right now? Let’s dig into the numbers and the story behind them so you can decide if this high-flyer is still a good value.

- After a wild ride, Chipotle shares are up 3.6% in the last week, but down 24.6% over the past month and a steep 47.3% year-to-date. This suggests changing perceptions of growth and risk.

- Recent headlines have focused on shifts in consumer spending habits and broader concerns about inflation that might squeeze restaurant margins. Ongoing news about Chipotle’s expansion plans and the fast-casual industry’s resilience continue to drive investor conversations.

- Right now, Chipotle scores a 3 out of 6 on our valuation checks. This means the stock appears undervalued in half of the areas we review. We will explore how different valuation methods paint the picture and hint at an even better way to gauge value by the end of this article.

Find out why Chipotle Mexican Grill's -46.3% return over the last year is lagging behind its peers.

Approach 1: Chipotle Mexican Grill Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow (DCF) model takes projected future cash flows a business is expected to generate and discounts them back to their value today, accounting for the time value of money. This approach aims to estimate what the company is intrinsically worth based on its fundamentals, instead of market sentiment.

For Chipotle Mexican Grill, the most recent reported Free Cash Flow is $1.57 Billion. Analysts estimate annual Free Cash Flow will grow, reaching $2.48 Billion by 2029. Although analysts provide estimates for the next five years, additional years are extrapolated to build a complete picture. These projections help assess the company’s ability to grow and generate returns over the long term.

Based on these calculations and using a 2 Stage Free Cash Flow to Equity model, Chipotle’s estimated intrinsic value per share is $35.62. When compared to the current share price, this analysis suggests the stock is 11.4% undervalued.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Chipotle Mexican Grill is undervalued by 11.4%. Track this in your watchlist or portfolio, or discover 906 more undervalued stocks based on cash flows.

Approach 2: Chipotle Mexican Grill Price vs Earnings

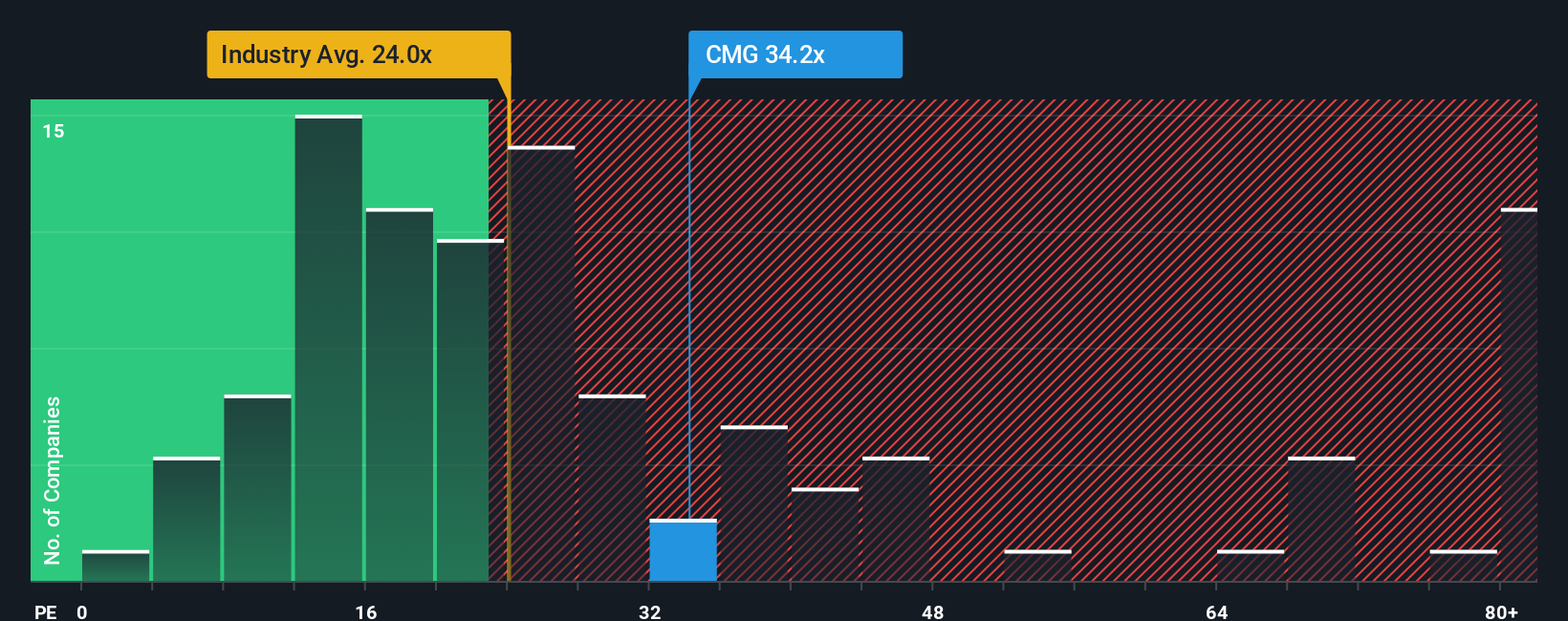

For profitable companies like Chipotle Mexican Grill, the Price-to-Earnings (PE) ratio is a popular tool for valuation. This metric provides a quick way to see how much investors are paying for each dollar of earnings, making it especially useful when a business has a solid earnings track record.

The "normal" or fair PE ratio for a company is heavily influenced by factors like expected earnings growth and the risks the company faces. Faster-growing, lower-risk firms usually command higher PE ratios, while slower growth and greater uncertainty push the ratio down.

As of now, Chipotle trades at a PE ratio of 27.17x. Compared to the Hospitality industry average of 20.83x and a peer average of 43.64x, Chipotle sits above its industry but well below leading comparables. Simply Wall St’s “Fair Ratio” for Chipotle is calculated as 26.04x. This proprietary benchmark accounts for not only industry trends and profit margins but also factors like company-specific growth expectations, risk profile, and market capitalization.

The Fair Ratio offers a more tailored benchmark than a simple comparison to peers or industry averages. Because it integrates Chipotle’s actual earnings growth prospects, relative risk, and other fundamentals, it provides a more precise gauge of the company's underlying value.

Chipotle’s current PE ratio of 27.17x is very close to its Fair Ratio of 26.04x. This signals that the stock's price is well-aligned with its underlying earnings power.

Result: ABOUT RIGHT

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1413 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Chipotle Mexican Grill Narrative

Earlier we mentioned there is an even better way to understand valuation, so let’s introduce you to Narratives. Narratives are the stories investors tell themselves about a company, linking their expectations about its future (such as revenue growth, earnings, margins, and fair value) to both the numbers and a clear rationale behind them. Instead of focusing only on static metrics, Narratives connect Chipotle’s business trajectory with specific financial forecasts, producing a fair value estimate that evolves as your view does.

On Simply Wall St’s Community page, millions of investors use Narratives as an easy, accessible tool to share and debate their perspectives, test assumptions, and see the story behind every valuation. Narratives help you decide when to buy or sell by comparing your calculated fair value to the actual market price. Whenever news breaks or earnings come out, the models automatically update to reflect the latest information.

For example, some investors forecast significant global expansion and margin improvement, leading them to a bullish fair value of $65 per share. Others highlight economic headwinds and industry risks, resulting in a more conservative estimate closer to $46. Narratives let you align your investment decision with your own outlook, not just the crowd’s.

Do you think there's more to the story for Chipotle Mexican Grill? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com