Ubisoft (ENXTPA:UBI): Assessing Valuation Following Earnings Delay and Trading Halt

Ubisoft Entertainment (ENXTPA:UBI) has announced a delay in releasing its first-half 2025-26 results and requested a halt in trading of its shares and bonds on Euronext. This move is drawing plenty of investor attention.

See our latest analysis for Ubisoft Entertainment.

The trading halt and results delay follow a rough patch for Ubisoft’s shareholders, with a year-to-date share price return of -47.36% and a one-year total shareholder return of -49.91%. While this week’s 11.31% share price jump hints at renewed speculation, the stock’s longer-term momentum remains challenged.

If major event-driven swings have you curious about opportunity elsewhere, now is a great time to broaden your search and discover fast growing stocks with high insider ownership

The question now confronts investors directly: are recent declines and analyst price targets signs that Ubisoft is trading at a bargain, or is the market already reflecting the company’s expected recovery in its share price?

Most Popular Narrative: 40.2% Undervalued

With the current share price at €6.77 and the most widely followed narrative estimating fair value at €11.33, Ubisoft is viewed as significantly undervalued by analysts tracking future recovery and new projects. The following insight explains why this gap has captured attention.

The launch of Assassin's Creed Shadows demonstrated strong early sales and engagement, suggesting future revenue boosts as the game continues to perform well and receives ongoing content updates and expansions. This can positively impact revenue and net margins.

Curious about what powers this bold valuation? The real story comes down to blockbuster launches, ambitious franchise growth, and a dramatic swing in profitability. The narrative behind the numbers signals a game-changing three-year outlook and a valuation leap that demands a closer look.

Result: Fair Value of €11.33 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, continued heavy reliance on blockbuster titles and high cash flow consumption could challenge Ubisoft’s path to sustained recovery and invalidate bullish analyst forecasts.

Find out about the key risks to this Ubisoft Entertainment narrative.

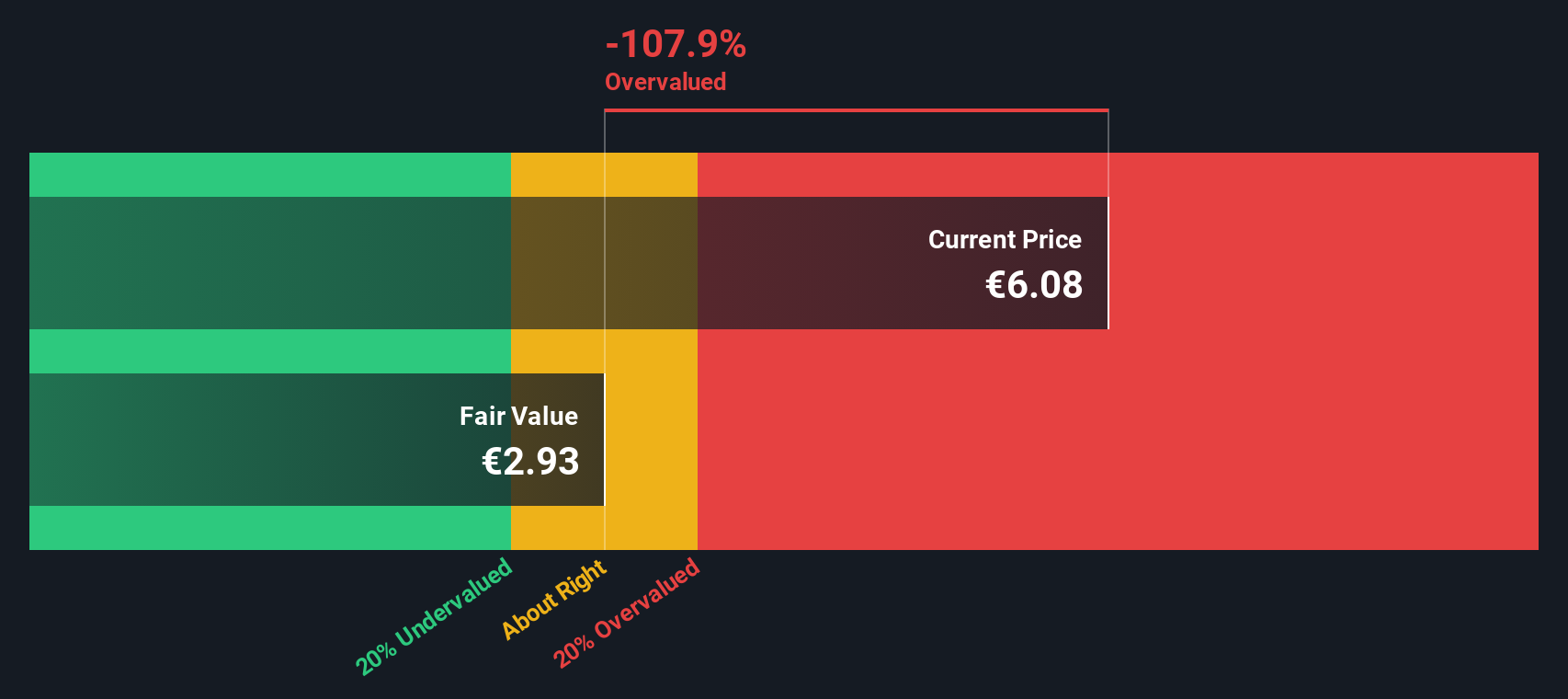

Another View: Discounted Cash Flow Tells a Different Story

While analysts see Ubisoft as good value compared to peers using price-to-sales, our SWS DCF model suggests something else entirely. The DCF estimate puts Ubisoft’s fair value far below the current share price and challenges the optimism of recovery narratives. Are analysts overlooking persistent risks?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Ubisoft Entertainment for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 886 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Ubisoft Entertainment Narrative

If you see things differently or want to dig deeper, you can quickly piece together your own view on Ubisoft in just a few minutes. Do it your way

A great starting point for your Ubisoft Entertainment research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Smart investors know it pays to think beyond the obvious. Use these proven screeners to get ahead of the crowd and unlock your next opportunity now.

- Unearth high-potential opportunities by targeting these 886 undervalued stocks based on cash flows as these may benefit from powerful cash flow trends this year.

- Capture potential passive income by targeting these 16 dividend stocks with yields > 3% offering attractive yields above 3% in the current market.

- Ride the emerging tech wave by identifying these 25 AI penny stocks as these companies are taking artificial intelligence mainstream with real revenue growth.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com