Watts Water Technologies (WTS): Evaluating Valuation as Momentum Slows After Strong Year-to-Date Gains

Watts Water Technologies (WTS) stock has slipped over the past month, shedding around 2% despite strong year-to-date gains. Investors seem to be weighing recent performance against the company's steady annual revenue and net income growth.

See our latest analysis for Watts Water Technologies.

After a stellar stretch that saw Watts Water Technologies enjoy a 34.5% year-to-date share price return, momentum has cooled a bit in recent weeks, with the stock easing back from recent highs. Still, when you look at the bigger picture, shareholders have benefited from both strong short-term gains and impressive compounding. Watts’ total return over the last five years sits at 141%, reflecting business strength even as near-term enthusiasm wavers.

If you’re in the mood to expand your watchlist beyond the obvious, this is an ideal time to discover fast growing stocks with high insider ownership.

With solid fundamentals and a share price just below analyst targets, the question stands: is Watts Water Technologies currently undervalued, offering investors a window for entry, or is future growth already reflected in the price?

Most Popular Narrative: 4.3% Undervalued

With Watts Water Technologies closing at $269.84 compared to a narrative fair value estimate of $282.00, the current price sits notably below the consensus outlook. This suggests potential opportunity if projected trends hold true. The difference between analyst expectations and present trading levels adds intrigue to the company's future trajectory.

"The accelerating rollout and success of Nexa, Watts' intelligent water management platform, positions the company to capture the growing demand for advanced, data-driven water conservation, efficiency, and regulatory compliance solutions. This is expected to drive higher-margin, recurring revenue and support long-term earnings and margin expansion."

How does the consensus arrive at this fair value? The calculation is based on transformative tech, bold compound growth, and a future profit multiple that would grab any investor’s attention. Which ambitious numbers and strategic bets power this outlook? Uncover the specifics that set the bar for Watts’ premium. There’s more beneath the surface than meets the eye.

Result: Fair Value of $282.00 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, persistent weakness in the European market or unexpected tariff pressure could quickly reverse Watts' recent gains and challenge the case for further upside.

Find out about the key risks to this Watts Water Technologies narrative.

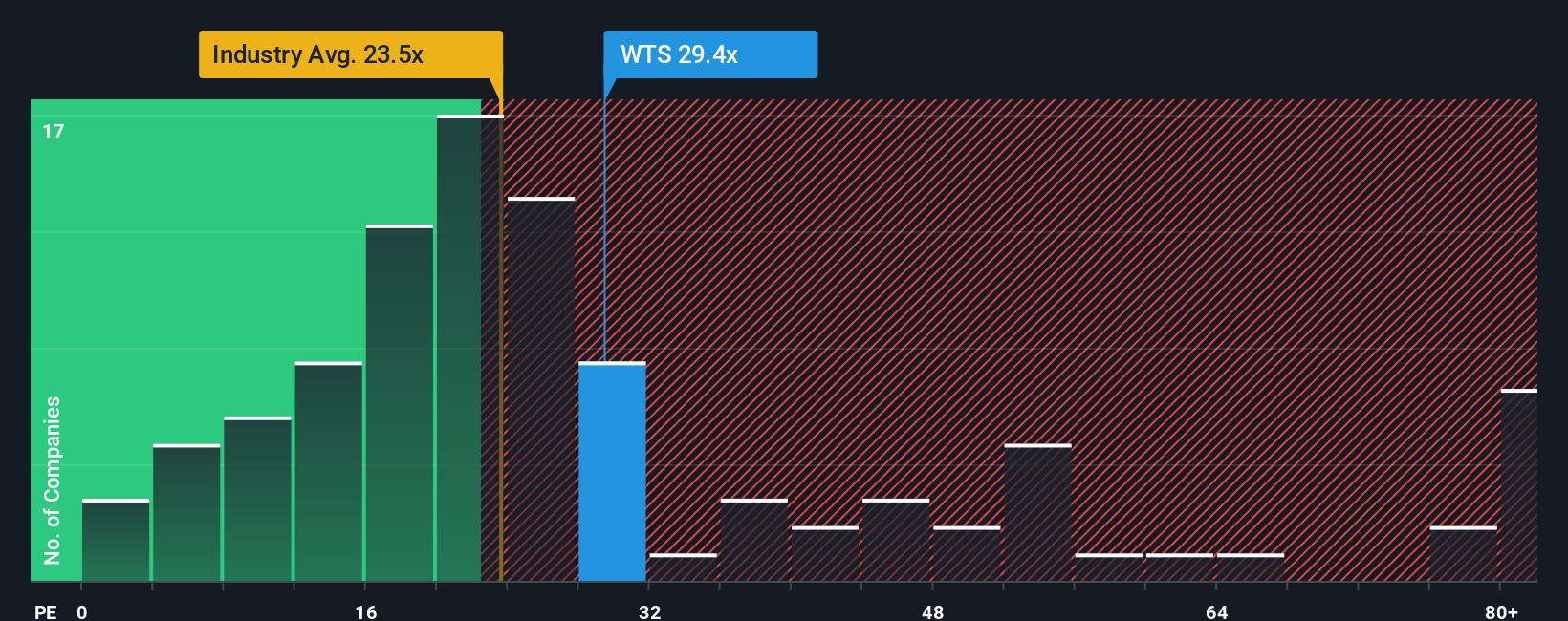

Another View: Market Multiples Tell a Cautionary Tale

Looking from a different angle, the market’s current price-to-earnings ratio for Watts Water Technologies is higher than both the US Machinery industry average and its fair ratio. WTS trades at 27.7x earnings, while the industry is at 23.9x and the fair ratio sits lower at 22.4x. This premium could mean investors are paying up for perceived growth and reliability. However, it may also raise the stakes for disappointment if expectations slip.

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Watts Water Technologies Narrative

If the numbers or outlook here don’t quite align with your perspective, you can dive into the figures yourself and form your own story in just a few minutes. Do it your way

A great starting point for your Watts Water Technologies research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Looking for More Investment Ideas?

Smart investors are those who seek out opportunity before the crowd acts. Make the most of your next move by tapping into fresh, actionable stock ideas you won’t want to overlook.

- Tap into the explosive growth of digital assets by accessing these 82 cryptocurrency and blockchain stocks that are leading the charge in tomorrow’s financial landscape.

- Unlock potential income streams by reviewing these 16 dividend stocks with yields > 3% with yields above 3% to explore reliable cash flow opportunities.

- Spot innovation early by researching these 25 AI penny stocks that are disrupting traditional sectors with ground-breaking advancements in artificial intelligence.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com